Key Takeaways:

- Wealth Management Growth: Net new assets hit $31 billion in Q1 2026, representing 8% annualized growth—second-best quarter ever.

- Price Projection: Based on current execution, RJF stock could reach $185 by September 2028.

- Potential Gains: This target implies a total return of 21% from the current price of $153.

- Annual Return: Investors could see roughly 8% growth over the next 2.6 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Raymond James Financial (RJF) reported record quarterly revenues of $3.7 billion in fiscal Q1 2026, up 6% year-over-year. The firm delivered adjusted earnings per share of $2.86 and maintained its 20% adjusted pretax margin target despite headwinds from lower interest rates and softer investment banking revenues.

CEO Paul Shoukry emphasized the company’s focus on “The Power of Personal”—deep client relationships that drive sustainable growth.

This approach continues to resonate with financial advisers, reflected in strong recruiting momentum and client asset growth of 15% year-over-year to a record $1.71 trillion.

The firm recruited advisers with $460 million in trailing production over the past 12 months, equivalent to a significant acquisition.

CFO Butch Oorlog highlighted that 89% of earnings were returned to shareholders through dividends and $1.45 billion in share buybacks over the year.

Mobile wealth management platforms and AI tools like Rai—Raymond James’ proprietary operations agent—are helping advisers save time and strengthen client relationships.

The firm invested nearly $1.1 billion in technology this year, creating a competitive moat that smaller firms struggle to match.

See analysts’ full growth forecasts and estimates for RJF stock (It’s free) >>>

What the Model Says for Raymond James Stock

We analyzed Raymond James through its transformation into a leading independent wealth management platform with diversified revenue streams across Private Client Group, Capital Markets, Asset Management, and Banking segments.

The company benefits from structural tailwinds in wealth management.

- Adviser recruiting remains robust, with $31 billion in quarterly net new assets representing the second-best quarter in company history.

- This growth is broad-based across independent contractor, employee, and RIA custody channels.

- Raymond James’ banking segment provides additional upside. Securities-based lending balances surged 28% year-over-year and 10% in Q1 alone, reflecting synergies with the growing private client business.

- Management expects continued strong loan growth as lower rates make floating-rate products more attractive.

Using a forecast of 7.8% annual revenue growth and 20% operating margins, our model projects the stock will rise to $185 within 2.6 years. This assumes an 11.3x price-to-earnings multiple.

That represents compression from Raymond James’ historical P/E averages of 14x (one year) and 12.9x (five years).

The lower multiple acknowledges near-term headwinds from interest rate cuts, which have reduced non-compensable revenues, and the timing-dependent nature of investment banking fees.

The real value lies in capturing long-term growth in wealth management through superior adviser retention and recruiting, while expanding fee-based assets and deploying the strong balance sheet in securities-based lending.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for RJF stock:

1. Revenue Growth: 7.8%

Raymond James’ growth centers on structural demand for high-quality wealth management services.

The company delivered 6% revenue growth prior year quarter, driven by record client assets and consistent net new asset additions.

Management expects this momentum to continue as adviser recruiting pipelines remain robust.

Fee-based assets of $1.04 trillion grew 19% year-over-year, with strong net inflows annualizing at nearly 10%.

The recently announced Clark Capital acquisition adds $46 billion in combined assets and strengthens the firm’s model portfolio and managed account capabilities.

2. Operating margins: 20%

Raymond James achieved its 20% adjusted pretax margin target in Q1 despite revenue headwinds from lower interest rates and softer capital markets activity.

This performance reflects the stability of diversified revenue streams and disciplined expense management.

Management expects non-compensation expenses to grow approximately 8% in fiscal 2026, primarily reflecting continued technology investments.

The firm’s focus on quality over quantity in adviser recruiting supports margin sustainability, as higher-net-worth client acquisition drives revenue without proportional cost increases.

3. Exit P/E Multiple: 11.3x

The market values Raymond James at 12.3x earnings. We assume the P/E will compress modestly to 11.3x over our forecast period, below historical averages of 13-14x.

Near-term uncertainty from interest rate policy and investment banking timing weighs on the multiple.

However, the firm’s differentiated culture, leading technology platform, and strong balance sheet position it well for sustained growth.

As Raymond James continues demonstrating resilient execution across market cycles, the stock should benefit from multiple expansion back toward historical norms.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Wealth management firms face market volatility and competition for adviser talent. Here’s how Raymond James stock might perform under different scenarios through September 2030:

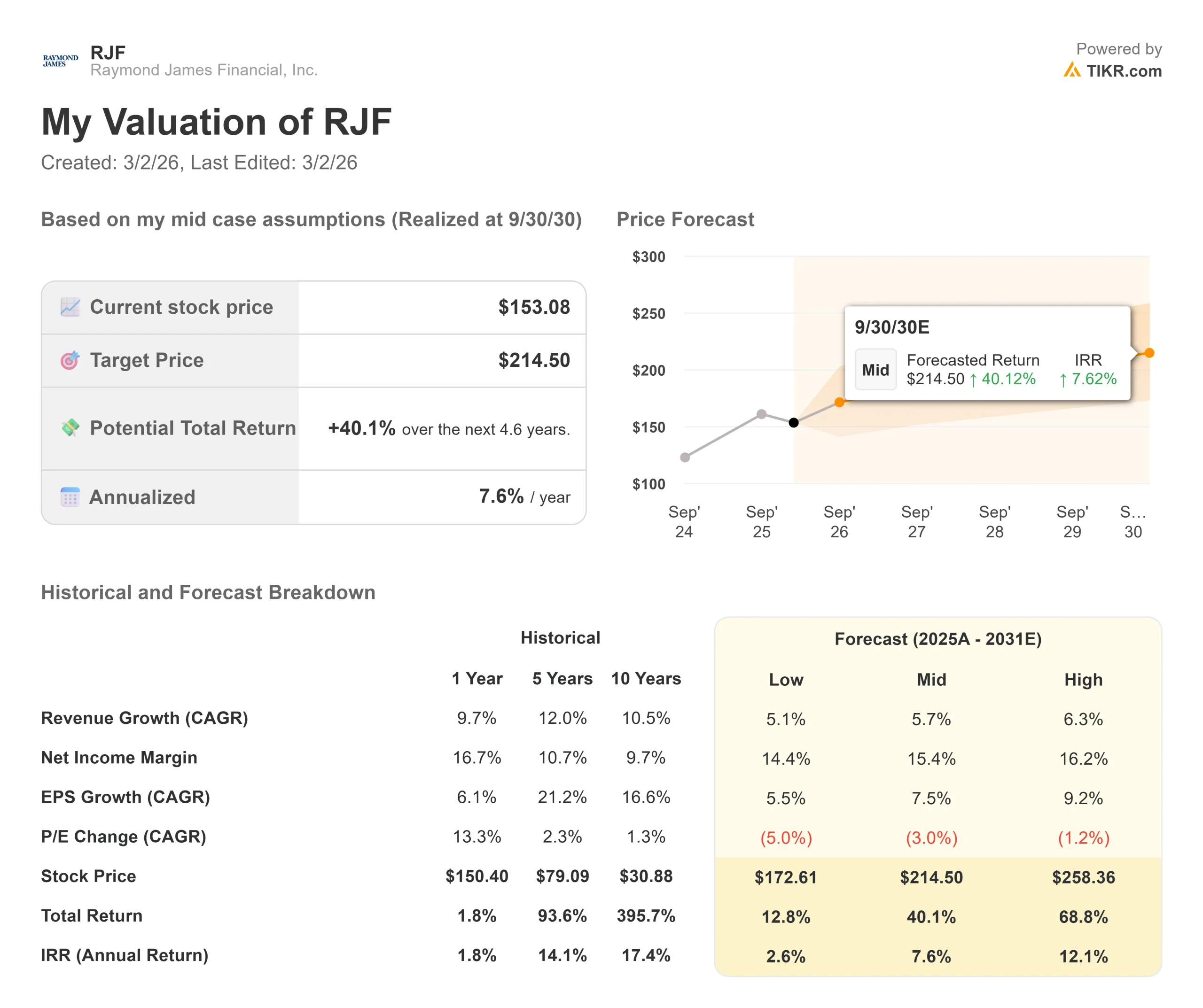

- Low Case: If revenue growth slows to 5.1% and net income margins compress to 14.4%, investors still see a 12.8% total return (2.6% annually).

- Mid Case: With 5.7% growth and 15.4% margins, we expect a total return of 40.1% (7.6% annually).

- High Case: If recruiting acceleration drives 6.3% revenue growth while Raymond James maintains 16.2% margins, returns could hit 68.8% total (12.1% annually).

See what analysts think about RJF stock right now (Free with TIKR) >>>

The range reflects execution on adviser recruiting, successful integration of acquisitions like Clark Capital, and the banking segment’s ability to grow securities-based lending while maintaining credit quality.

In the low case, competitive pressures from private equity-backed firms intensify, or sustained low interest rates compress banking profitability.

In the high case, the investment banking pipeline converts stronger than expected, technology investments drive operating leverage faster than anticipated, and adviser satisfaction translates to accelerated recruiting and retention.

How Much Upside Does Raymond James Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!