Key Takeaways:

- AI Infrastructure Boom: Data center revenue surged 50% in fiscal 2025, driven by power management and optical connectivity demand.

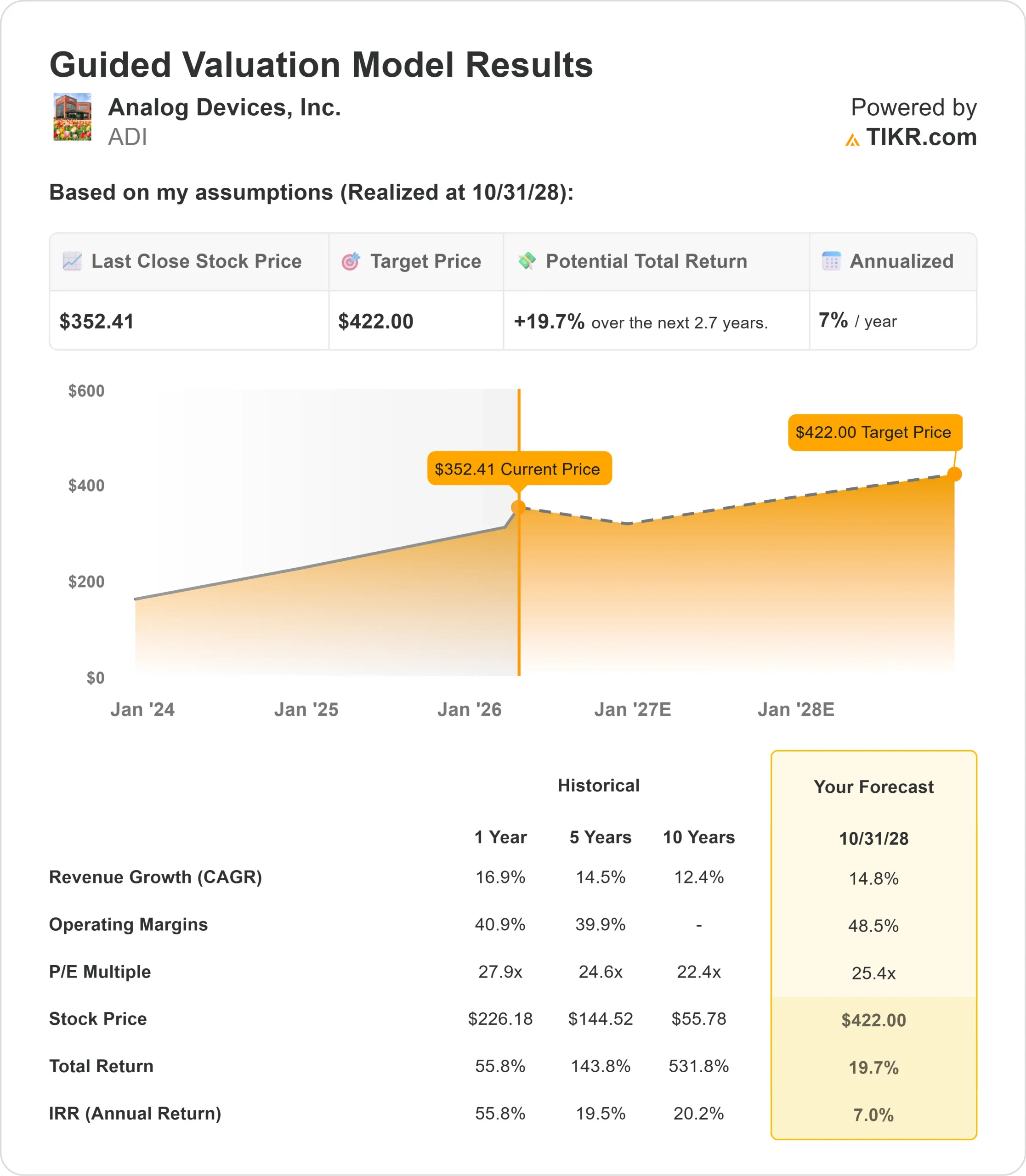

- Price Projection: Based on current execution, ADI stock could reach $422 by October 2028.

- Potential Gains: This target implies a total return of 20% from the current price of $352.

- Annual Return: Investors could see roughly 7% growth over the next 2.7 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Analog Devices (ADI) delivered an impressive Q1 2026, beating guidance across revenue, profitability, and earnings per share while raising its dividend by 11%.

CEO Vincent Roche highlighted the company’s strategic positioning in high-growth megatrends, particularly AI-driven computing and connectivity.

This segment, encompassing automated test equipment (ATE) and data centers, now accounts for nearly 20% of ADI’s revenue, running at a $2 billion-plus run rate.

- The data center business grew by 50% in fiscal 2025, fueled by AI infrastructure buildouts.

- ADI’s power management solutions address critical challenges as hyperscalers deploy higher-voltage architectures and denser GPU clusters.

- The company’s protection circuits, power delivery systems, and digital control technologies enable data centers to scale AI workloads while managing thermal and efficiency constraints.

- ATE revenue accelerated by 40% in fiscal 2025 and continued to grow in Q1 2026.

- ADI supplies integrated pin electronics and measurement systems for testing advanced semiconductors, with content reaching tens of thousands of dollars per tester.

- Rising chip complexity and AI-related device proliferation create durable demand tailwinds.

- Beyond AI, Industrial markets showed broad-based recovery.

- The segment grew 38% year-over-year in Q1, with strength across automation, aerospace, defense, and instrumentation.

- Management noted normalized ordering patterns typical of an up-cycle, with book-to-bill ratios well above 1.0.

Despite strong fundamentals and record investment in innovation, questions remain about sustainability as the company navigates automotive headwinds and pricing dynamics.

See analysts’ full growth forecasts and estimates for ADI stock (It’s free) >>>

What the Model Says for Analog Devices Stock

We analyzed Analog Devices as it transformed into a diversified analog leader with commanding positions in AI infrastructure, industrial automation, and automotive electronics.

- The company benefits from structural shifts in demand. Data centers require increasingly sophisticated power management as AI accelerators push thermal and efficiency limits.

- ADI’s mixed-signal expertise enables precise voltage regulation, fault protection, and thermal management—capabilities that become more valuable as compute density increases.

- In industrial markets, ADI holds leadership in ATE, aerospace, and instrumentation. These applications demand long product lifecycles, exceptional reliability, and system-level integration—all ADI strengths that support pricing power and margin expansion.

- Management demonstrated pricing discipline in Q1, implementing increases that reflect both innovation premiums and responses to persistent cost inflation.

- Gross margins expanded 240 basis points year-over-year to 71.2%, driven by favorable mix, higher utilization, and pricing actions.

Using a forecast of 14.8% annual revenue growth and 48.5% operating margins, our model projects the stock will rise to $422 within 2.7 years. This assumes a 25.4x price-to-earnings multiple.

That represents compression from ADI’s historical P/E averages of 27.9x (one year) and 24.6x (five years). The lower multiple acknowledges near-term automotive softness and potential margin pressure as pricing benefits moderate.

The real value lies in capturing AI infrastructure growth while maintaining momentum in Industrial and Communications across a diversified portfolio.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ADI stock:

1. Revenue Growth: 14.8%

ADI’s growth reflects strong execution across multiple drivers.

- Industrial revenue grew 50% year-over-year in Q2 guidance, led by ATE and aerospace strength.

- Communications accelerated 63% year-over-year in Q1, with data center and wireless both showing double-digit sequential growth.

Management expects fiscal 2026 to be a banner year.

- Q2 guidance of $3.5 billion implies 11% sequential growth, well above the typical 4-5% seasonality.

- Book-to-bill remains healthy across Industrial segments, and the company isn’t shipping below consumption anymore.

2. Operating margins: 48.5%

Q1 operating margin was at 45.5%, above the high end of the guidance, up 200 basis points sequentially and 500 basis points year-over-year.

Q2 guidance targets 47.5% operating margins, reflecting gross margin expansion from favorable mix and pricing, partially offset by strategic R&D investments and higher variable compensation.

Management expects OpEx growth to trail revenue growth by roughly half for the full year, creating significant operating leverage.

3. Exit P/E Multiple: 25.4x

The market values ADI at 29.5x current earnings. We assume modest compression to 25.4x over our forecast period.

Near-term automotive headwinds create some uncertainty. The segment declined 8% sequentially in Q1 despite 8% year-over-year growth, as Chinese tariff-related pre-buying unwound.

Management expects automotive to remain below seasonal in Q2 before recovering in the second half.

As AI infrastructure deployment continues and Industrial markets strengthen, ADI should command a premium multiple.

The company’s technical leadership, pricing power, and margin-expansion trajectory support long-term above-market valuations.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

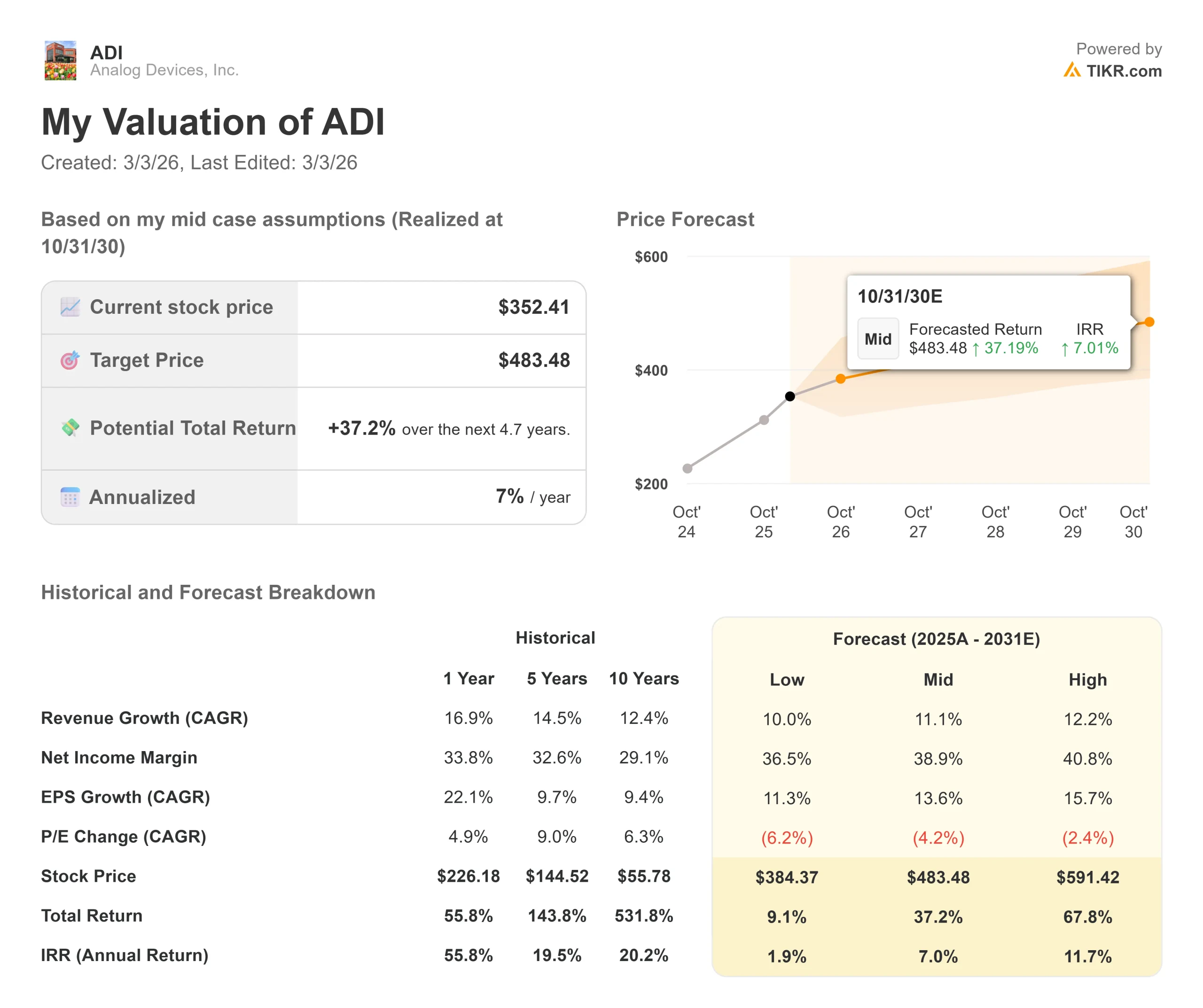

ADI’s performance depends on AI infrastructure spending, industrial recovery pace, and automotive market stabilization. Here’s how the stock might perform under different scenarios through October 2030:

- Low Case: If revenue growth moderates to 10.0% and net income margins compress to 36.5%, investors still see a 9.1% total return (1.9% annually).

- Mid Case: With 11.1% growth and 38.9% margins, we expect a total return of 37.2% (7.0% annually).

- High Case: If AI acceleration drives 12.2% revenue growth while ADI maintains 40.8% margins, returns could hit 67.8% total (11.7% annually).

See what analysts think about ADI stock right now (Free with TIKR) >>>

The range reflects execution on AI infrastructure wins, successful navigation of automotive challenges, and Industrial momentum sustainability.

In the low case, data center spending decelerates, or automotive weakness persists longer than expected.

In the high case, AI workloads exceed projections, Industrial recovery accelerates, and pricing power drives margin expansion beyond current expectations.

How Much Upside Does Analog Devices Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!