Key Takeaways:

- Strong Q4 Performance: Capital One reported adjusted earnings of $3.86 per share, driven by synergies from the Discover integration.

- Price Projection: Based on current execution, COF stock could reach $253 by December 2028.

- Potential Gains: This target implies a total return of 30% from the current price of $194.

- Annual Return: Investors could see roughly 10% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Capital One Financial (COF) wrapped up 2025 with strong Q4 results, earning $3.26 per diluted share and completing the strategic sale of its $8.8 billion Discover Home Loans portfolio.

For the full year, the company generated adjusted earnings of $19.61 per share while integrating Discover’s operations and announcing a transformative $5.15 billion acquisition of Brex, the business payments pioneer.

CEO Richard Fairbank highlighted the company’s position at a pivotal moment.

- Capital One has built the nation’s third-largest small-business credit card franchise, while the Discover acquisition creates the opportunity to scale a proprietary payments network.

- The Brex deal accelerates Capital One’s expansion into corporate liability cards and integrated business payment solutions, creating new revenue streams across small business banking and corporate travel.

- Purchase volume growth reached 6.2% year-over-year in the domestic card business, excluding Discover.

- Growth was strongest among heavy spenders at the top of the market, where Capital One continues investing aggressively in premium benefits.

- The combined domestic card portfolio now generates a revenue margin of 17.3%, with credit metrics stabilizing after nearly a year of improvement.

Despite intense competition from major banks and fintechs, Capital One sees disciplined behavior across the industry.

Fairbank noted that while investment requirements are higher, competitors aren’t engaging in reckless credit practices that characterized past cycles.

See analysts’ full growth forecasts and estimates for COF stock (It’s free) >>>

What the Model Says for Capital One Stock

We analyzed Capital One as it transformed into an integrated banking and payments company with leading positions in credit cards, consumer banking, and commercial lending.

The company benefits from multiple structural tailwinds.

- In business cards, continued migration from cash to digital payments drives industry growth of roughly 9% annually.

- Capital One’s heavy spender franchise captures a disproportionate share at the premium end of the market, where customers generate higher purchase volumes and engagement.

- The Discover network integration creates vertical integration benefits.

- Capital One has nearly completed migrating debit cards to Discover’s network, capturing immediate synergies.

- Credit card migration will begin through testing this year, with the ability to originate new Capital One cards on Discover’s network by mid-2026.

- Brex adds a comprehensive business payments platform to accelerate growth in corporate liability cards, where Capital One’s presence is currently smaller than in personal liability.

- The acquisition brings modern technology infrastructure built from the ground up, enabling Capital One to expand its small business bank nationally and enhance its travel portal with corporate travel capabilities.

Using a forecast of 9.3% annual revenue growth and 50% operating margins, our model projects the stock will rise to $253 within 2.8 years. This assumes an 8.4x price-to-earnings multiple.

That represents compression from Capital One’s historical P/E averages of 11.7x (one year) and 9.1x (five years).

The lower multiple reflects near-term investments in network acceptance, Brex integration, and premium card benefits that will pressure efficiency ratios before driving long-term revenue growth.

The real value lies in Capital One’s unique position, combining a scaled consumer franchise, a proprietary payments network, and a modern technology stack well-positioned for AI-driven solutions.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for COF stock:

1. Revenue Growth: 9.3%

Capital One’s growth centers on three engines.

- The domestic card business delivered 6.2% organic growth with stronger performance in premium segments. Management expects this momentum to continue as the company invests in acquiring heavy spenders and deepens customer relationships.

- The Discover integration adds growth through network synergies as debit and eventually credit volume migrates to the proprietary network. International acceptance expansion and brand building will unlock additional opportunities to capture payment flows.

- Brex accelerates growth in business payments with corporate liability cards and small-business banking. Management expects these investments to generate significant revenue growth on the other side of the integration, consistent with their original expectations for the Discover deal.

2. Operating margins: 50%

Capital One’s operating margins reflect disciplined expense management alongside strategic investments.

The company is investing heavily in technology, marketing, and integration costs.

Management acknowledged that investments in Brex, network acceptance, premium benefits, and AI will create near-term pressure on efficiency ratios.

However, these investments directly target revenue growth opportunities with attractive long-term economics.

3. Exit P/E Multiple: 8.4x

The market values Capital One at 9.6x earnings. We assume the P/E will compress modestly to 8.4x over our forecast period.

Near-term investment spending and pressure on the efficiency ratio weigh on the multiple.

However, as revenue growth accelerates from Discover synergies and Brex capabilities, Capital One should command a premium valuation given its differentiated position, combining banking scale with ownership of payments networks.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

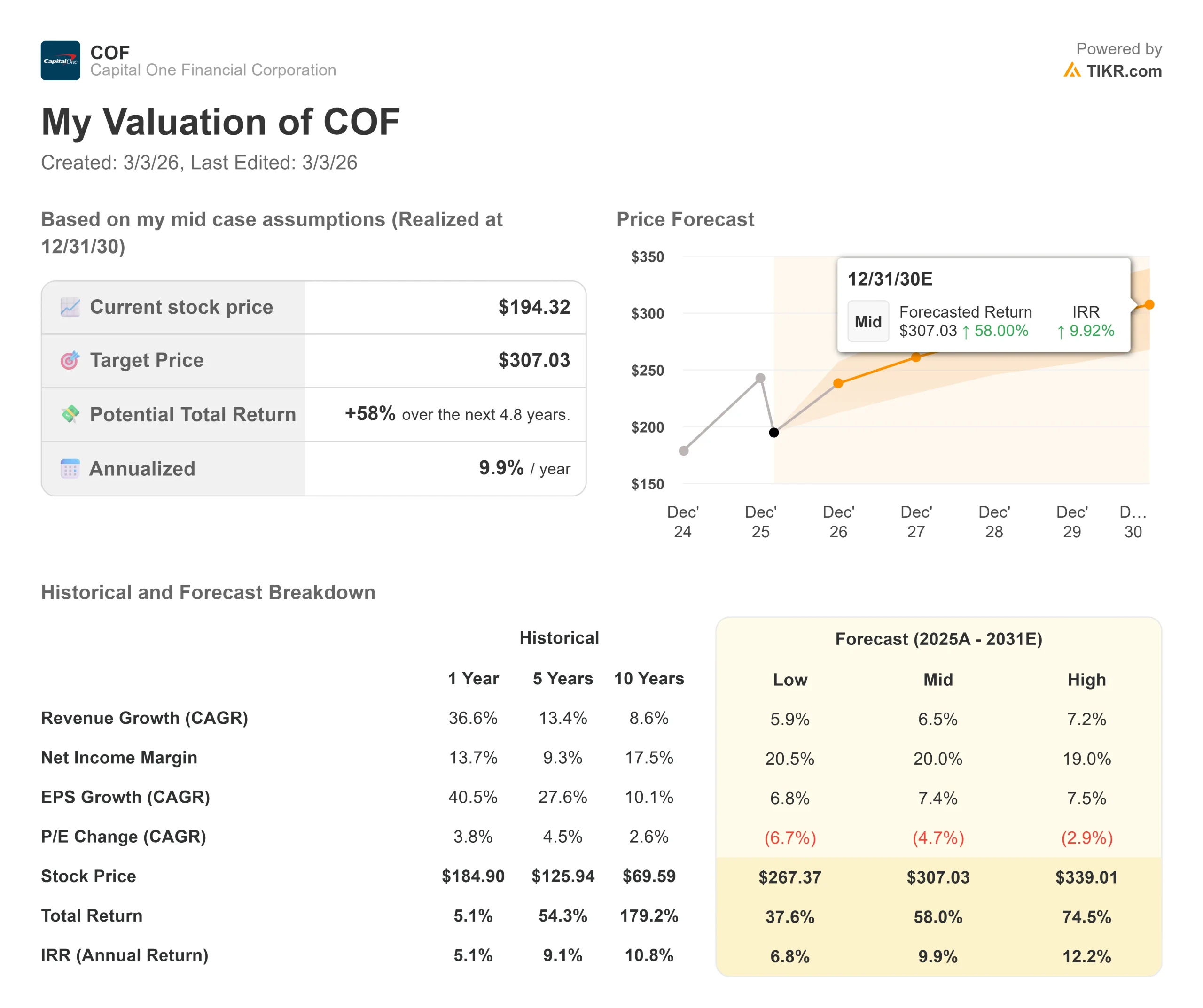

Banking companies face credit cycles and competitive intensity. Here’s how Capital One stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth moderates to 5.9% and net income margins compress to 20.5%, investors still see a 37.6% total return (6.8% annually).

- Mid Case: With 6.5% growth and 20.0% margins, we expect a total return of 58.0% (9.9% annually).

- High Case: If Brex integration and network growth drive 7.2% revenue growth while Capital One maintains 19.0% margins, returns could hit 74.5% total (12.2% annually).

See what analysts think about COF stock right now (Free with TIKR) >>>

The range reflects execution on the Discover integration, the successful scaling of the payments network, and Brex’s ability to capture market share in the business payments market.

In the low case, competitive intensity or credit deterioration constrains growth.

In the high case, network effects and Brex’s modern platform drive faster-than-expected revenue acceleration with improved efficiency ratios.

How Much Upside Does Capital One Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!