Key Stats for ACN Stock

- Past week’s performance: -3.7%

- 52-week range: $187 to $326

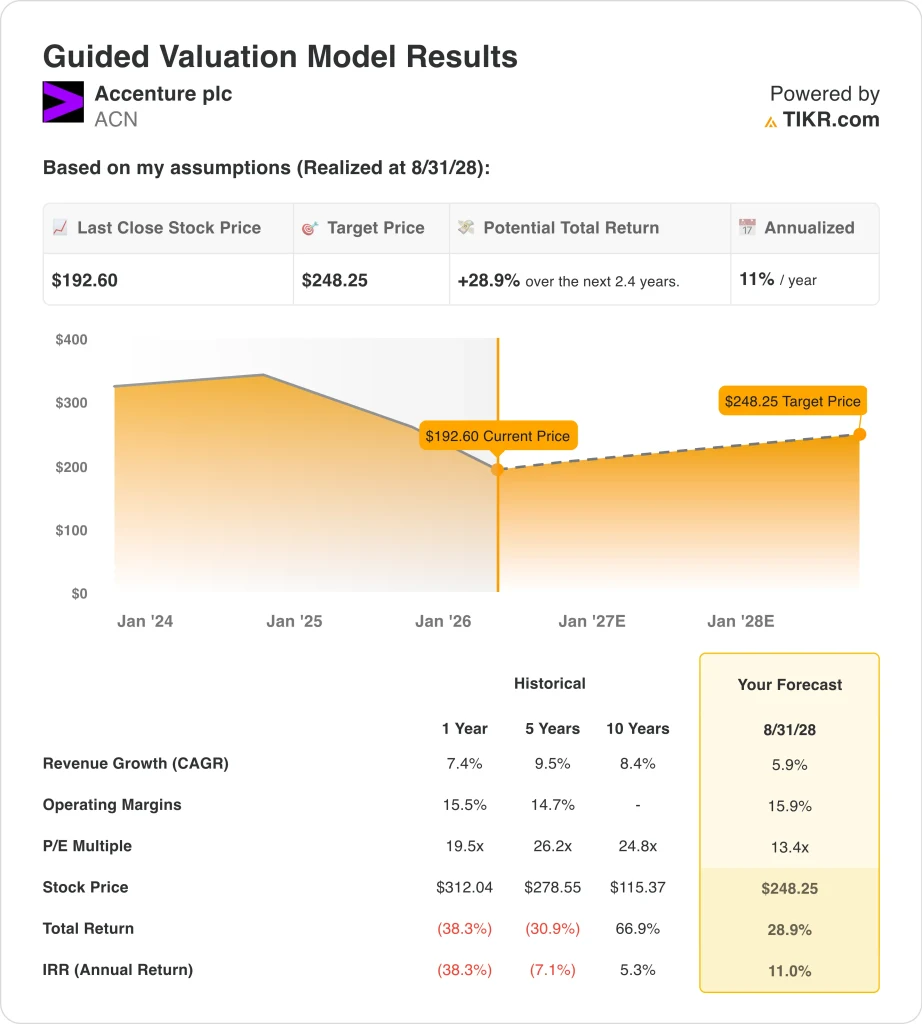

- Valuation model target price: $248

- Implied upside: 28.9% over 2.4 years

Value your favorite stocks like ACN with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Accenture (ACN)’s stock weakness this week was really an earnings story. The company reported fiscal Q2 revenue of $18.04 billion, ahead of estimates, and it posted record quarterly bookings of $22.1 billion. But the market focused more on its Q3 revenue outlook of $18.35 billion to $19.0 billion, which came in below analysts’ expectations.

That split reaction explains the stock move. Investors liked the strong AI demand, higher bookings, and the company’s decision to raise the low end of its full-year local-currency revenue growth outlook to 3% from 2%. But they were less comfortable with near-term guidance and with management’s comment that federal business would create about a 1% drag on fiscal 2026 growth.

Management made clear that AI demand is still strong. In Accenture’s Q1 fiscal 2026 conference call, CEO Julie Sweet said, “The demand for AI is both real and rapidly maturing.” The company also said it is on track in fiscal 2026 to more than double bookings from key emerging AI and data ecosystem partners versus fiscal 2025, which helps explain why AI remains central to the bullish case even as the stock falls.

The company kept adding to that narrative after earnings. Accenture launched Cyber.AI with Anthropic’s Claude for security operations on March 25, expanded its Microsoft security collaboration, and announced a NOAA modernization contract through Accenture Federal Services. So the market is not questioning whether demand exists. It is questioning how quickly that demand turns into faster growth at a time when federal spending is a headwind and consulting budgets remain selective.

See analysts’ growth forecasts and price targets for ACN (It’s free) >>>

Is ACN Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.9%

- Operating Margins: 15.9%

- Exit P/E Multiple: 13.4x

Based on these inputs, the model estimates a target price of $248.25, implying 28.9% total upside from the current share price and a 11.0% annualized return over the next 2.4 years.

The valuation case is not built on aggressive assumptions. Accenture’s model uses 5.9% annual revenue growth, which is below its 7.4% one-year historical growth rate and well below the 9.5% five-year pace shown in the valuation image. That matters because the stock is already pricing in a slower, more mature business, not an AI hyper-growth story.

Margins also look grounded. The model assumes 15.9% operating margins, only modestly above the 15.7% LTM level and close to management’s fiscal 2026 adjusted operating margin outlook of 15.7% to 15.9%. In other words, the valuation depends more on steady execution than on a dramatic profitability jump.

The business still has solid fundamentals. LTM revenue is $72.1 billion, LTM free cash flow is about $12.5 billion, and the company has net cash of roughly $1.1 billion. Accenture also trades at about 13.5x NTM earnings and 8.1x NTM EBITDA, which is much lower than the 19.5x P/E shown in the model’s one-year historical context.

This means investors are paying for a resilient services franchise with strong cash generation, but they are no longer willing to pay a premium multiple unless growth reaccelerates. That is why record bookings and rising AI work matter so much now, because they are the clearest evidence that Accenture can keep taking share even in a slower spending environment.

What’s Driving the ACN Stock Going Forward?

The next catalyst is execution against the updated fiscal 2026 outlook. Management now expects full-year revenue growth of 3% to 5% in local currency, or about 4% to 6% excluding the federal drag, and adjusted EPS of $13.65 to $13.90. That means investors will be watching whether commercial demand stays strong enough to offset pressure in federal work.

Bookings are especially important because they show future revenue potential. Accenture delivered $22.1 billion in Q2 bookings and $43.0 billion in the first half, with a 1.2 book-to-bill ratio in both periods. Management also said 41 clients generated more than $100 million in quarterly bookings, which suggests the company is still winning large transformation projects despite tighter budgets.

AI remains the most important growth driver. Accenture said more than 60% of Q2 revenue was tied to its top 10 ecosystem partners, and that growth from those partners outpaced the company’s average. It also now has more than 85,000 AI and data professionals and more than 1,400 advanced AI clients, which shows the scale it has built around enterprise AI adoption.

Acquisitions are another swing factor. Julie Sweet said Accenture expects to deploy $5 billion more in acquisitions this year, and management said completed deals are meant to expand the firm into higher-growth areas with attractive margins. That could support growth, but investors will want proof that acquisition spending converts into faster organic revenue and more non-labor-based revenue over time.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Accenture?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACN, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ACN alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Accenture stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!