Key Stats for Walmart Stock

- 52-Week Range: $94.23–$135.16

- Current Price: $119.00

- Street Mean Target: ~$139

- TIKR Target Price (Mid): ~$147

- Market Cap: ~$947 billion

- LTM Gross Margin: 25.0%

- NTM P/E: ~40x

- Dividend Yield: 0.9%

- Fwd 2-Yr EPS CAGR: ~12%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Walmart Is Not the Retailer You Think It Is Anymore

Most investors look at Walmart Inc. (WMT) and see what it has always been: the world’s largest retailer, built on low prices, an enormous store footprint, and razor-thin margins. That description still fits the surface. But underneath it, a different business is emerging, one that is quietly becoming one of the most important advertising and membership platforms in the country.

Global advertising revenue grew 37% in Q1 fiscal 2027. Walmart Connect, the company’s U.S. retail media business, grew 44% in the same period. Membership fee revenue grew 17% globally, with Walmart+ net adds hitting a record first-quarter high.

Together, advertising and membership now account for roughly one third of Walmart’s total operating income, a stunning figure for revenue streams that barely existed five years ago.

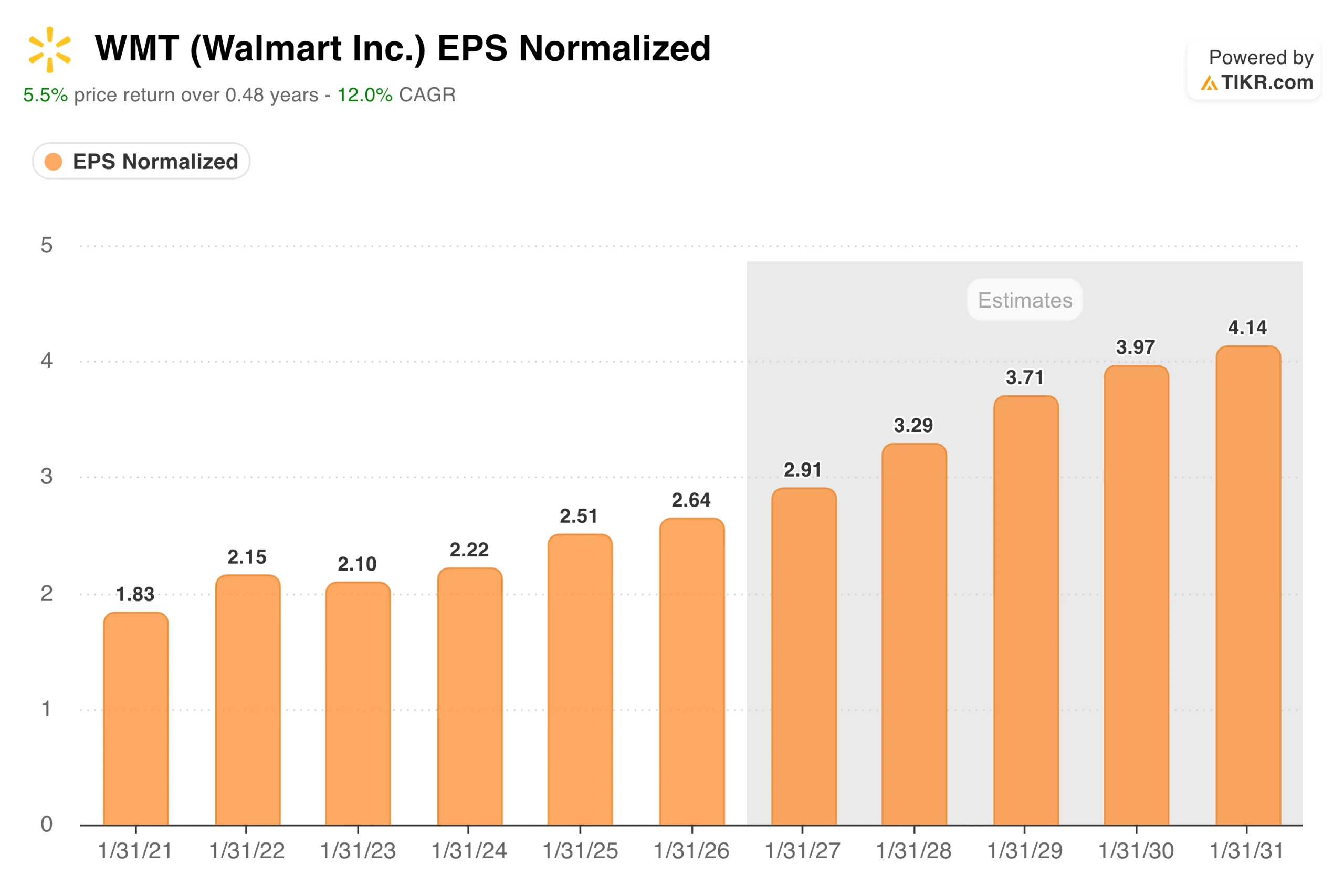

Normalized EPS grew from $1.83 in fiscal 2021 to $2.64 in fiscal 2026, a steady, unbroken climb across five years that included the pandemic recovery and a costly buildout of digital infrastructure.

Consensus estimates then accelerate noticeably: around $2.91 in fiscal 2027, building toward $4.14 by fiscal 2031. The reason estimates accelerate rather than simply persist is that advertising and membership carry margins far above the retail core, and they are growing at multiples of the company’s overall revenue growth rate.

“Our results reflect our continued focus on delivering across the enterprise,” said CEO John Furner, “growing higher-margin commerce solutions. It’s a disciplined approach that’s helping us grow the business and strengthen returns.”

eCommerce is the engine driving it all, and global eCommerce grew 26% in Q1 FY27, with marketplace GMV up a record 50%. More digital traffic creates more advertising inventory. More advertising inventory generates revenue at margins closer to software than retail. More marketplace sellers drive fulfillment volume, reinforcing the value of Walmart+ membership. The flywheel is real and accelerating.

See the exact moment Wall Street upgrades WMT stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

Why Did the Stock Fall 15% From Its Highs?

The business transformation story is not what sent WMT down. A single earnings day reaction did.

Walmart’s stock price peaked above $135 in late May before falling nearly 16% to its max drawdown on June 2, then partially recovering to around 11% below its highs today. The trigger was the Q1 FY27 earnings release: a solid headline beat that the market read as underwhelming given the valuation.

Free cash flow came in at negative $1.9 billion for the quarter, driven by $6.7 billion in capital expenditures, up 34% year over year. Inventory built 8.9%. Full-year guidance was left unchanged rather than raised.

None of those concerns is without merit, as a stock at around 40x forward earnings has little patience for a quarter that raises questions about cash generation. But the capex driving that negative free cash flow is building the automated distribution infrastructure that makes the eCommerce economics work.

Walmart expects 65% of its stores to eventually be served by automated distribution centers, and that investment has a long payback period that one quarter of free cash flow will not cover.

Walmart’s advertising and marketplace growth are reshaping the P&L. Track every earnings revision and analyst update in real time on TIKR for free →

What Does the Valuation Model Say?

TIKR’s valuation model targets around $147 per share in its mid case, representing roughly 24% total return from current levels at about 4.7% annualized over the next four and a half years. The high case reaches around $224, assuming mid-single-digit revenue growth and net income margins expanding toward 4%.

The honest tension is multiple. At around 40x forward earnings, WMT is not cheap by any traditional retail measure. The bull case requires believing that advertising and membership will continue to lift the consolidated margin profile. That those businesses have already grown to one-third of their operating income is evidence that the shift is working, but sustaining that trajectory at scale is a different challenge.

Tariff costs remain a wildcard given the company’s extensive sourcing in Asia. Competition from Amazon in both retail and advertising is structural. And a sustained period of negative free cash flow, while strategically defensible, is a risk conservative investors will weigh.

Should You Invest in Walmart?

Walmart is a business that has been consistently underestimated because the transformation is happening inside a company that still looks, from the outside, like a grocery store.

Advertising revenue, the membership flywheel, and automation investment do not fit the traditional mental model of Walmart.

The post-earnings pullback has brought the stock to a more attractive level than it was in late May. Whether the multiple is justified depends on how much you believe in the sustainability of the margin shift underway.

See the full TIKR model for WMT, including scenario assumptions and historical valuation multiples. Build your own valuation for Walmart stock on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!