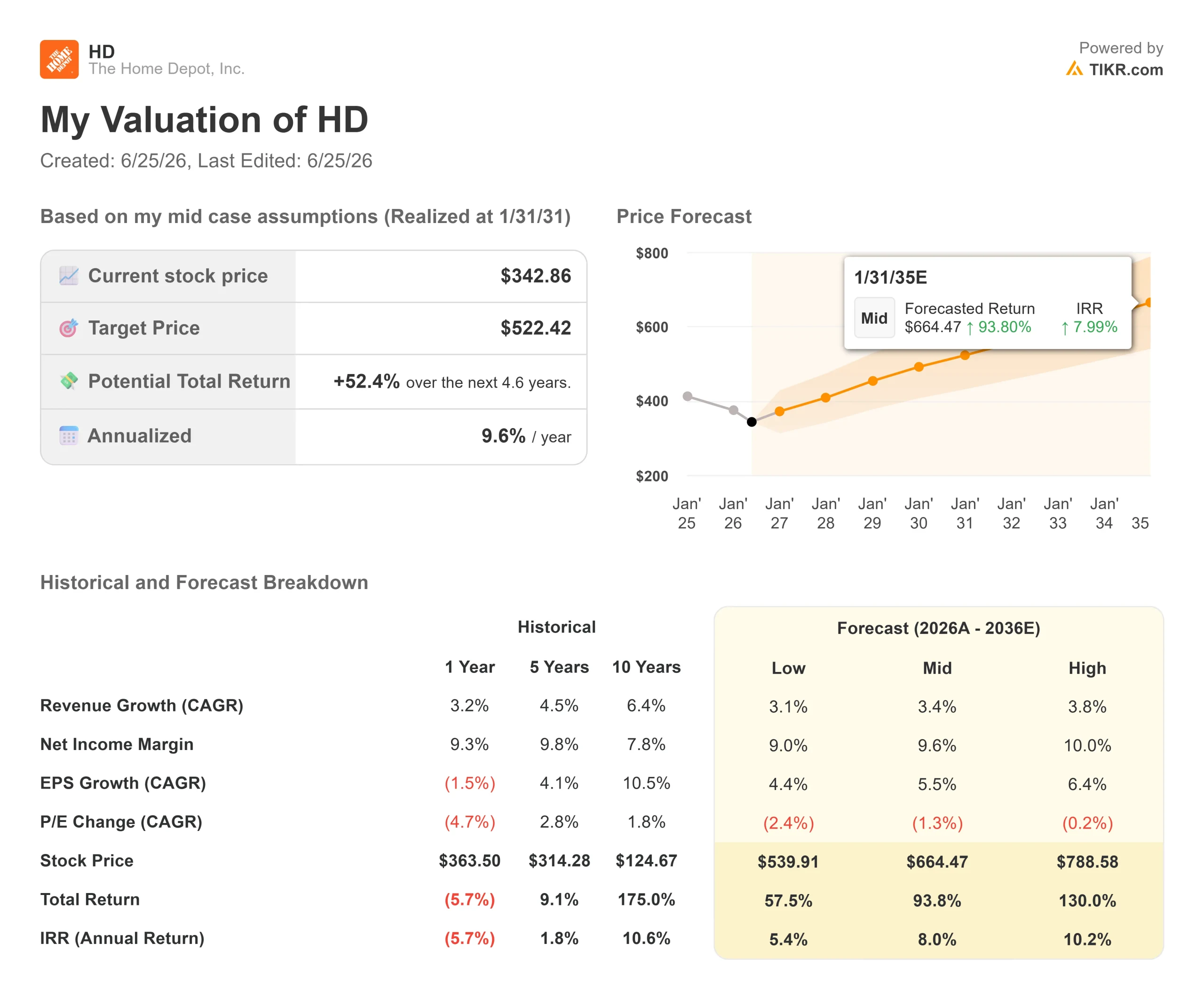

Key Stats for Home Depot Stock

- Current Price: $342.86

- Target Price (Mid): ~$520

- Street Target: ~$370

- Potential Total Return: ~52%

- Annualized IRR: ~10% / year

- Earnings Reaction: +2.69% (May 19, 2026)

- Max Drawdown: -29.74% (May 15, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The Home Depot (HD) absorbed a vote of no confidence from Wall Street on June 23, then did the opposite of what the bears expected. The morning after Wolfe Research cut its rating to Peer Perform from Outperform, the stock rose 5.67% to close at $342.86, a one-day gain of $18.41. Downgraded retailers in weak housing cycles do not usually trade like that.

That gap between the analyst call and the tape is the story. Wolfe analyst Spencer Hanus did not soften the message. He flagged the housing “lock-in” effect, meaning homeowners holding 3% mortgages who will not sell, plus return-on-capital dilution from Home Depot’s large professional-distribution acquisitions and rising rate risk. He said unlocking housing is a mid-2027 event at the earliest, and that Wolfe now prefers Lowe’s.

So why did buyers show up? Because the note contained nothing new. Every concern Hanus raised has defined the HD debate for two years, and the stock had already fallen nearly 30% from its $426.75 high, hitting a 29.74% drawdown on May 15. When caution lands on a stock that has already priced in caution, the reaction can invert. The market treated the downgrade as the last bear catching up, not the first arriving.

The real question is whether the fundamentals back the buyers or the skeptics.

What the Quarter Actually Showed

Fiscal Q1 2026, reported May 19, was not weak. Total sales were $41.8 billion, up 4.8% year over year, with comparable sales up 0.6%. Adjusted diluted earnings per share were $3.43, down from $3.56, a decline management had already guided for. The stock rose 2.69% on the print, results were in line, and full-year guidance was reaffirmed.

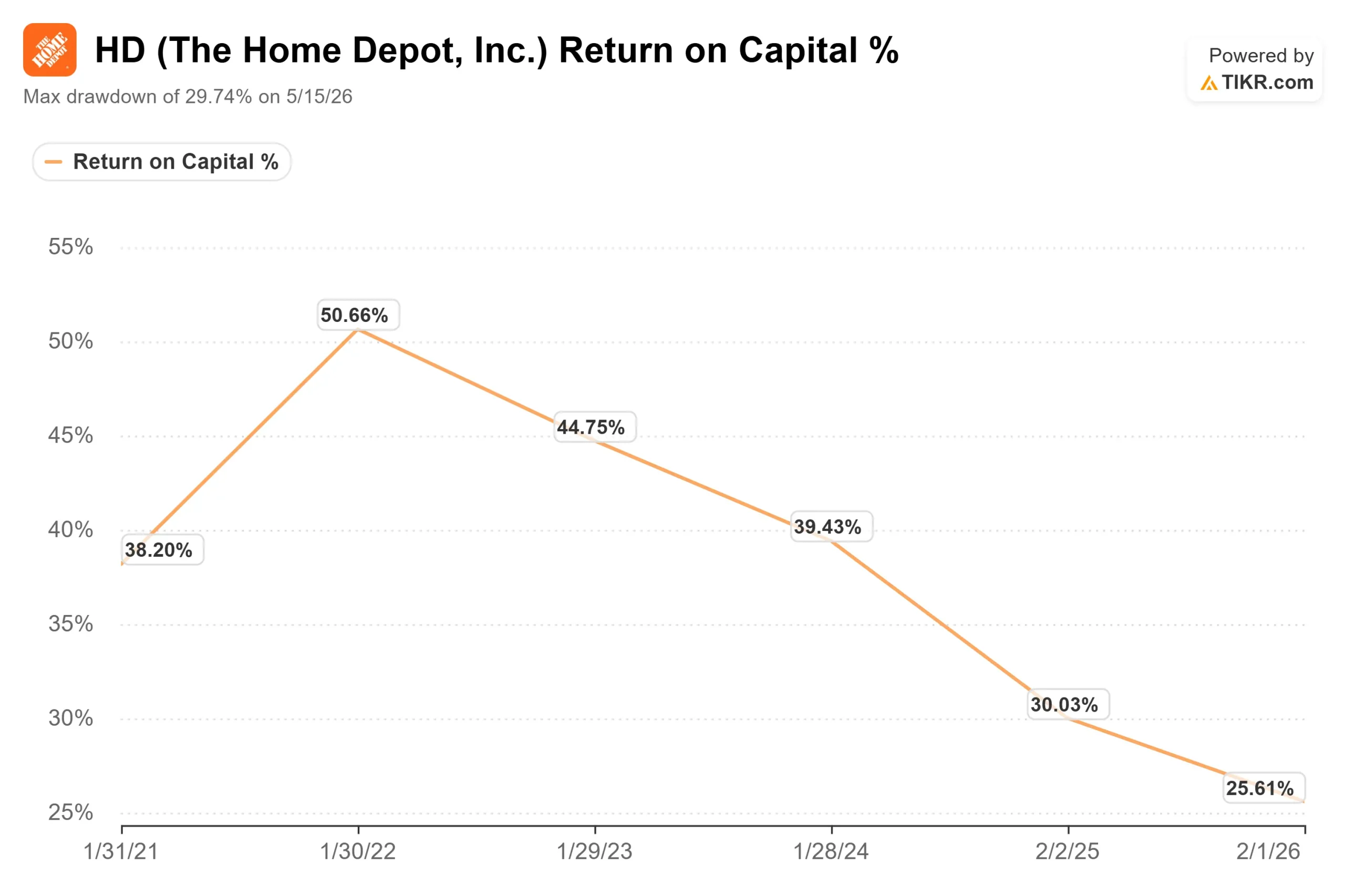

The detail Wolfe singled out is return on invested capital. On the Q1 call, management reported ROIC of 25.4%, down from 31.3% a year earlier. That decline is real, and it is exactly what large acquisitions do to a capital-efficiency ratio in the near term. The debate is whether it reflects permanent value destruction or the temporary cost of buying scale.

Management framed demand as steady, not deteriorating. CFO Richard McPhail said performance was “in line with our expectations,” with underlying demand “relatively similar to what we experienced throughout fiscal 2025.” That reframes the bear case: the problem is not falling demand, it is demand that will not accelerate while housing stays frozen.

The acquisition Wolfe worries about is also the company’s biggest bet. Last quarter, Home Depot closed its purchase of Mingledorff’s, a heating, ventilation, and air conditioning (HVAC) distributor with 42 Southeast locations. CEO Ted Decker said the deal opens a roughly $100 billion HVAC distribution market and lifts Home Depot’s total addressable market to $1.2 trillion, with the professional customer alone worth $700 billion. That is the upside Wolfe is discounting, and the bulls are buying.

See historical and forward estimates for Home Depot stock (It’s free!) >>>

The Valuation Tension

At $342.86, Home Depot trades at about 22x forward earnings and 15.6x NTM EV/EBITDA, a premium to where it sat at its spring lows. Bulls see a wide-moat compounder on sale versus its own history. The skeptic sees a mature retailer paying up for acquisitions that dilute returns, while the core waits on a housing recovery that keeps slipping.

Against peers, though, HD looks cheap. Its 15.6x NTM EV/EBITDA sits well below TJX Companies at 20.93x and Ross Stores at 19.29x, two off-price retailers with no housing exposure, per TIKR’s Competitors page. That roughly 5-turn discount reflects the housing cycle weighing on HD, not a broken business. Whether it is a gift depends on when turnover normalizes, the one variable nobody can date.

What tilts toward the buyers is the cash. Home Depot generated $10.1 billion in free cash flow over the trailing twelve months and paid about $2.3 billion in dividends last quarter alone. The 2.8% yield is funded by current cash, not a hoped-for recovery, giving holders a paid floor while the thesis plays out. The risk is timing: if rates stay high into 2027, comps stay flat, and the stock can drift longer than patient investors expect.

See how Home Depot performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $342.86

- Target Price (Mid): ~$520

- Potential Total Return: ~52%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Home Depot stock (It’s free!) >>>

The mid case points to a target near $520, implying around 52% total return, or roughly 10% per year. The two revenue drivers are Pro ecosystem expansion through SRS, GMS, and now Mingledorff’s, and a gradual recovery in big-ticket renovation demand as housing turnover normalizes. The model assumes a revenue CAGR of around 3% to 4%, below the long-run pace, so this is not a boom forecast.

The margin driver is net income margin holding near 9.6% as the GMS acquisition mix drag fades through late fiscal 2026. The primary risk is the one Wolfe named: housing turnover staying frozen, which would keep comps flat and push the recovery into 2027. The upside is that even modest normalization unlocks deferred demand in HD’s highest-share categories. The downside is a stock that drifts sideways, paying its dividend while investors wait on the Federal Reserve.

Conclusion

The cleanest test arrives with fiscal Q2 2026 results on August 18. Watch two lines. First, SRS organic growth: management guided to mid-single-digit growth for the year, so “good” looks like that line turning solidly positive and validating the acquisitions Wolfe questioned. “Bad” looks like roofing staying negative on another quiet storm season. Second, watch whether management holds the flat-to-2% full-year comp guide. A cut would confirm the downgrade; a hold would confirm the buyers. The downgrade asked a fair question, and August is when Home Depot starts to answer it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Home Depot?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Home Depot, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Home Depot alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Home Depot on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!