Key Stats for Coca-Cola Stock

- 52-Week Range: $65.35 to $84.04

- Current Price: $80.31

- Street Mean Target: $85.97

- TIKR Model Target (2030, Mid): ~$105

- Q1 2026 Organic Revenue Growth: 10%

- Q1 2026 EPS: $0.91 (+18% YoY)

- Q1 2026 Operating Margin: 35.0%

- FY2026 Comparable EPS Growth Guidance: 8% to 9%

- Dividend Yield: 2.7%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

10% Organic Revenue Growth, a New CEO, and a $20 Billion IRS Dispute That Refuses to Go Away

Most stocks in this series have a story built around a drawdown, a recovery, or a turnaround. Coca-Cola’s (KO) story is simpler and, depending on what you’re looking for, more compelling: the earnings just keep going up.

EPS has grown every year since 2021, from $2.32 in 2021 to $3.00 in 2025. No COVID crater, no post-cycle hangover, no missed guidance year.

The consensus expects that to continue, with estimates climbing toward $3.27 in 2026, $3.48 in 2027, and $4.19 by 2030. That kind of consistency is rare in any sector. In consumer staples, it is basically the gold standard.

The business spans more than 200 countries and territories, with a portfolio well beyond Coke. Sprite, Fanta, BODYARMOR, Fairlife, Dasani, smartwater, Costa, and Powerade all sit in the same system. Coca-Cola Zero Sugar grew 13% in Q1 2026.

Fairlife, the premium dairy brand, is scaling rapidly and represents one of the highest-margin additions to the portfolio in years.

See analysts’ growth forecasts and price targets for Coca-Cola stock (It’s free) >>>

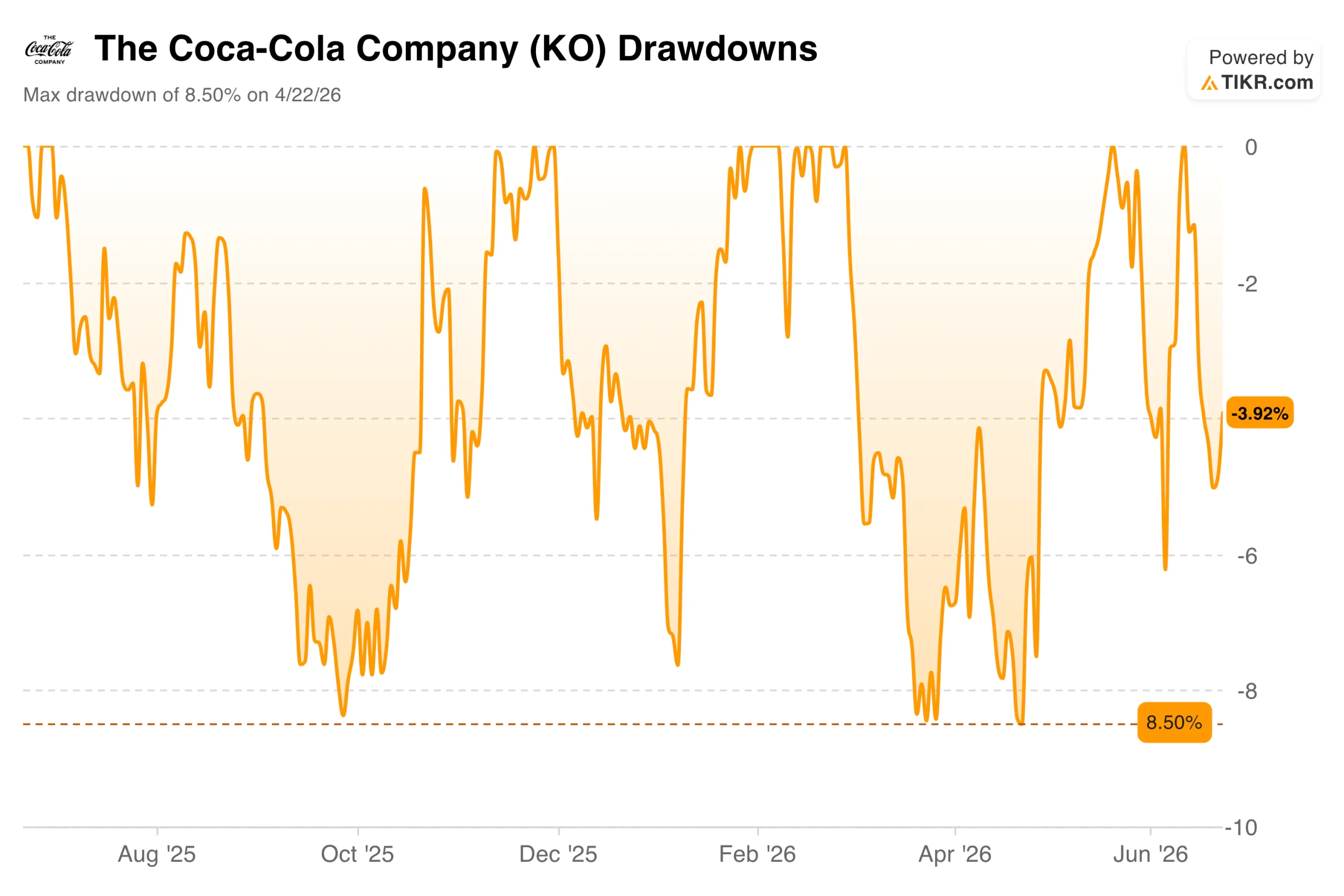

A Max Drawdown of 8.5% and a Stock Near Its All-Time High

The drawdowns chart for Coca-Cola looks nothing like most names in this series. The maximum drawdown over the entire period shown is just 8.5%, briefly hit in late 2025 and again in April 2026. The stock is currently only 4% off its recent all-time high of $84.04.

That stability is not an accident. Coca-Cola’s 0.36 beta reflects a business whose revenues are tied to global beverage consumption rather than economic cycles. People drink Coke during recessions, under tariff regimes, and when the S&P is down 20%.

The Q1 2026 results reinforced the narrative: organic revenues grew 10%, operating margin expanded to 35.0%, and EPS grew 18% to $0.91. Management raised full-year comparable EPS growth guidance to 8%-9%, up from 7%-8%. CEO Henrique Braun called it a strong start.

Estimate a company’s fair value instantly (Free with TIKR) >>>

From $2.32 to $3.00 in Four Years, With Estimates Pointing to $4.19 by 2030

The EPS chart is the cleanest in the series. From $2.32 in 2021 to $3.00 in 2025, every bar is higher than the one before it. No disruption, no step-down. Just consistent execution across a business that moves its concentration to bottlers in virtually every market on earth.

The consensus projects an acceleration from here. The jump from $3.00 in 2025 to an estimated $3.27 in 2026 reflects raised guidance, the Fairlife ramp, and the FIFA World Cup tailwind. Coca-Cola is the official sponsor of the 2026 tournament, which will run across the US, Mexico, and Canada, and has already activated partnerships across markets. These events historically move volume.

The one genuine overhang is a $20 billion tax dispute with the IRS now heading to the federal appeals court in Miami. Coca-Cola has been fighting this case for years, continues to exclude it from guidance, and the outcome remains genuinely uncertain.

A ~$105 Mid-Case Target, About 6% Annualized, and a 2.7% Dividend Along the Way

The TIKR valuation model targets around $105 per share for Coca-Cola by year-end 2030, implying roughly 31% total return from the current price of $80.31, or about 6% annualized. The mid-case assumes around 3% annual revenue growth and net income margins near 30%, consistent with the historical trajectory.

The high case implies a target near $155 and total returns above 90%. The Street mean of $85.97 suggests analysts broadly view the stock as fairly priced rather than a deep-value opportunity.

The bull case is that Coca-Cola compounds reliably across every macro environment, Fairlife adds a high-margin growth driver, and a 2.7% dividend provides a floor of return while waiting.

The bear case is that the stock trades at roughly 24 times forward earnings, a full price for mid-to-high single-digit EPS growth, and the IRS dispute is a real tail risk with no certain resolution date.

Coca-Cola is not the kind of stock that doubles. It is the kind of stock that, over long enough periods, rarely disappoints.

See the full TIKR model for KO, including scenario assumptions and historical valuation multiples. Build your own valuation for Coca-Cola stock on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!