Key Takeaways

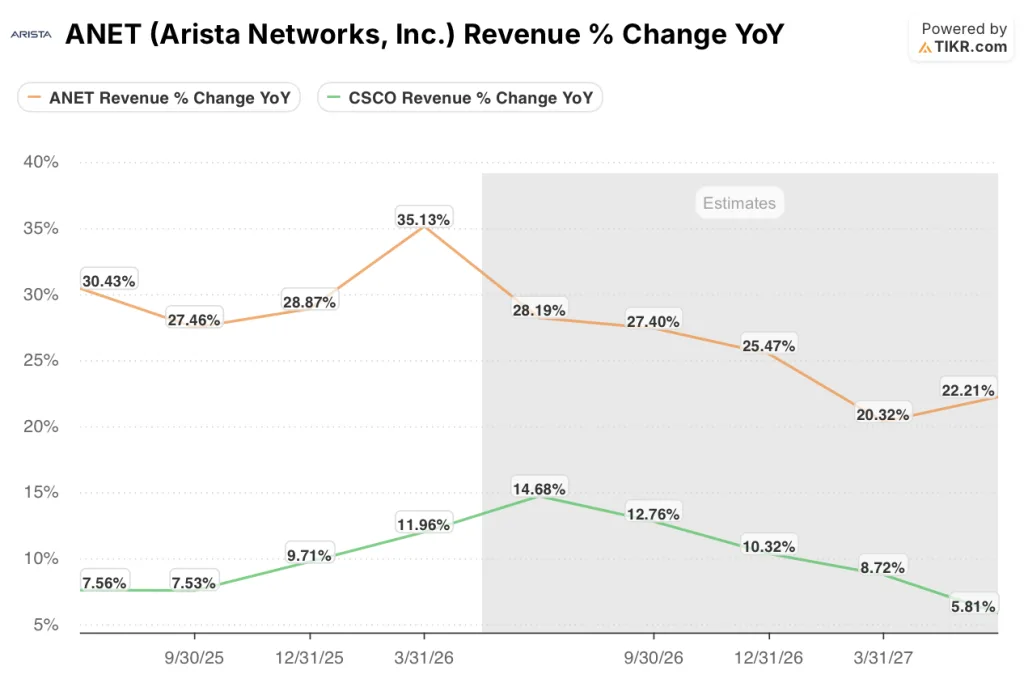

- Arista Networks stock is growing quarterly revenue at 35% versus Cisco Systems stock at 12%, a gap driven by Arista’s dominance in Ethernet-based AI fabric deployments at Microsoft, Meta, and emerging hyperscalers.

- TIKR’s valuation model targets around $339 for Arista Networks stock at an annualized IRR of roughly 18%, versus around $145 for Cisco Systems stock at roughly 5%, a 13-percentage-point gap in favor of Arista.

- Arista’s 43% operating margin in Q1 2026 is nearly double Cisco’s 25% operating margin in Q3 FY2026, reflecting the structural cost advantage of a pure-play networking business over a diversified portfolio carrying Splunk integration and collaboration declines.

- Cisco’s hyperscaler AI order intake is accelerating to $9 billion in fiscal 2026, with Silicon One P200 design wins at three hyperscalers for scale-across applications confirmed in Q3 and early Q4, making Cisco the improving but still slower-growth alternative.

Why Arista Networks Is the Purer Bet and Cisco Systems Is the Safer One

AI chips only work if they are wired together efficiently. The switches and cables that connect thousands of GPUs inside a data center are not glamorous, but they determine whether a cluster runs at full speed or wastes computing time waiting on data.

Arista Networks (ANET) builds that plumbing, and the biggest cloud companies in the world, Microsoft and Meta among them, have made it their default choice for AI infrastructure.

Arista does one thing: high-speed networking. That focus is the source of its edge. Its software, called EOS, runs identically across every product it sells, which makes managing a large AI cluster significantly simpler than stitching together gear from multiple vendors. The company raised its fiscal 2026 revenue guidance to approximately $11.5 billion, representing roughly 28% growth, and lifted its AI networking revenue target to $3.5 billion, more than doubling its AI sales in a single year. Demand is outpacing what Arista can ship, not the other way around.

Cisco Systems (CSCO) on the other hand is the established giant of networking. It sells switches, routers, security software, collaboration tools, and optics to enterprises, governments, and cloud providers around the world. That breadth made Cisco dominant for decades and still generates roughly $63 billion in annual revenue. But it also means Cisco is not a pure AI play: most of what it sells serves customers who are upgrading campus networks, renewing software contracts, or replacing aging hardware, not building GPU clusters from scratch.

Cisco is catching up in AI. Its Silicon One chip and Acacia optics business are winning orders from hyperscalers at a pace the company did not expect at the start of the year, with AI infrastructure orders from cloud giants now expected to reach $9 billion for fiscal 2026. Chuck Robbins, Cisco’s Chair and CEO, described Q3 as a record quarter with product revenue up 17% and total orders up 35%.

But for every dollar of AI acceleration, there are legacy segments growing slowly or shrinking, and that drag is why Cisco Systems stock trades at a steeper discount to Arista Networks stock than either company’s AI traction alone would suggest.

The Street Gives Arista Networks 17% Implied Upside and Cisco Systems Just 5%

Of 30 analysts covering Arista Networks stock, 22 rate it a Buy and 7 rate it Outperform, with just 1 Hold and no Underperforms or Sells as of June 23, 2026. The mean price target is $190, with the high reaching $220, against a close of $162, implying 17% upside on the consensus mean.

The Street expects Arista Networks to grow quarterly revenue at roughly 28% in the next reported quarter, with EBITDA margins around 47% and normalized EPS growing roughly 21% year over year.

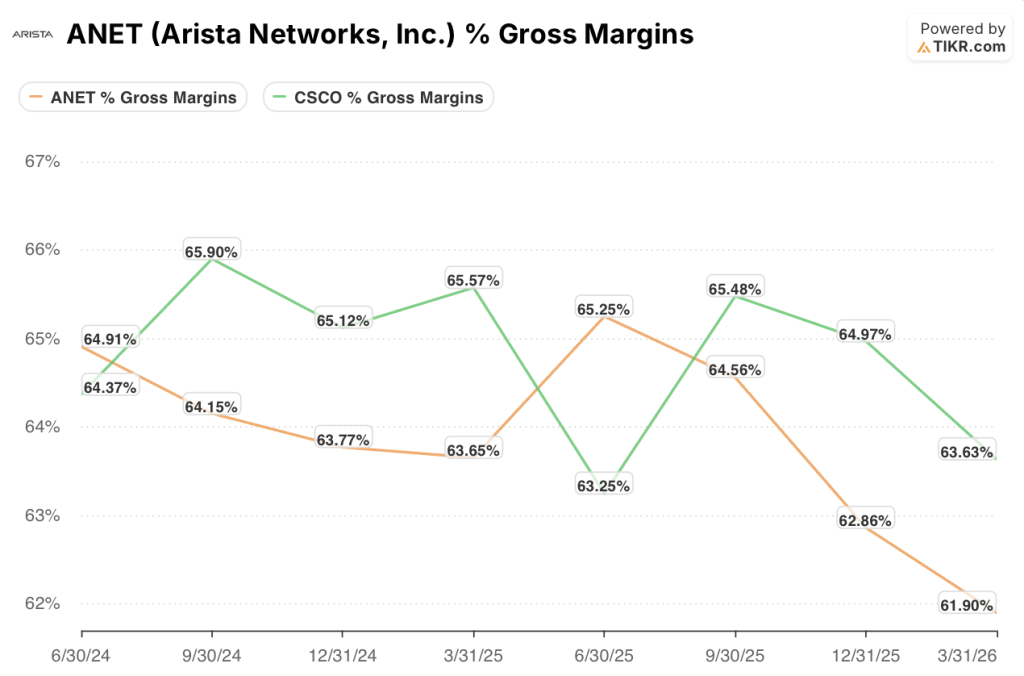

Analysts are not worried about demand. The concern is gross margin, which came in at 62% in Q1 2026, down from 65% a year earlier, as higher memory costs and a heavier mix of large cloud customers weighed on profitability.

Chantelle Breithaupt, Arista’s CFO, held the full-year gross margin guidance at 62% to 64%, with recovery dependent on a shift back toward enterprise customers in the second half.

Meawnhile, of 26 analysts covering Cisco Systems stock, 13 rate it a Buy and 4 rate it Outperform, with 8 Holds and 1 Underperform as of June 23, 2026. The mean price target is $127, with the high at $150, against a close of $121, implying 5% upside on the consensus mean.

Analysts expect Cisco Systems to post quarterly revenue of $16.83 billion in the next reported quarter, with EBITDA margins around 38% and normalized EPS growing roughly 18% year over year.

The Street’s caution is not about Cisco’s AI momentum, which is real. It is about the weight of the rest of the portfolio. The Splunk cloud transition is compressing near-term revenue recognition.

Collaboration revenue is declining. And Cisco’s stock has already run nearly 100% off its 52-week low of $66, leaving limited room for error if growth moderates.

Arista Networks Runs a 43% Operating Margin While Cisco Systems Runs 25%

The most important financial contrast between Arista Networks stock and Cisco Systems stock is not revenue size. It is what each company keeps from every dollar it earns.

Arista posted an operating margin of 43% in Q1 2026, on $2.71 billion in revenue that grew 35% year over year. Cisco posted an operating margin of 25% in Q3 FY2026, on $15.84 billion in revenue that grew 12% year over year.

Arista is the smaller company but the far more efficient one: it runs a leaner cost structure because it sells only networking gear and does not carry the overhead of a security division, a collaboration business, or a $28 billion acquisition in the middle of a transition.

Gross margin tells a more nuanced story.

Cisco’s 64% gross margin edges Arista’s 62%, but the gap reflects mix rather than product quality. Cisco benefits from high-margin software and services revenue, which runs above 71% gross margin on the services side. Arista’s margin is compressed by a higher weighting toward large cloud customers, who negotiate harder on price than enterprise buyers.

Both companies are absorbing elevated memory costs, and both are managing it differently: Cisco raised prices on hardware SKUs and secured supply agreements, while Arista is holding pricing steady with key customers and accepting near-term margin pressure to protect long-term relationships.

Revenue growth is where the comparison sharpens.

Arista grew 35% in its most recent quarter, accelerating from 28% a year earlier. Cisco grew 12%, recovering from negative territory in mid-2024 but unlikely to sustain double-digit growth across all segments simultaneously. Consensus expects Arista to grow quarterly revenue in the 25% to 28% range over the next four quarters and Cisco in the 9% to 15% range. At those rates, Arista’s revenue doubles in roughly four years while Cisco’s grows by 40% to 50%.

TIKR’s Model Targets an 18% IRR for Arista Networks and 5% for Cisco Systems

TIKR’s valuation model on Arista Networks stock targets a price of around $339, implying a total return of approximately 109% from the current price of $162, at an annualized rate of around 18%.

The model assumes a revenue growth CAGR of roughly 17% and a net income margin of roughly 40%. Both are conservative relative to where Arista is today, which gives the upside case room to run if demand holds through the platform transition.

Cisco’s picture looks different. TIKR’s valuation model on Cisco Systems stock targets a price of around $145, implying a total return of approximately 20% from the current price of $121, at an annualized rate of around 5%.

The model assumes a revenue growth CAGR of roughly 6% and a net income margin of roughly 28%, reflecting Cisco as the large, stable business it is today. That framing does not price in a successful AI transition. Mark Patterson, Cisco’s CFO, guided for at least $6 billion in AI revenue recognition in fiscal 2027, and if that order book converts, the target of around $145 is likely too conservative.

The IRR gap of roughly 13 percentage points is the clearest version of the story: Arista Networks stock offers meaningfully higher annualized returns for investors willing to pay for faster growth, while Cisco Systems stock suits those who want stability and income at a lower entry price.

Should You Invest in Arista Networks, Inc. or Cisco Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Arista Networks stock and Cisco Systems stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down for both companies.

You can build a free watchlist to track Arista Networks stock and Cisco Systems stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ANET and CSCO stock on TIKR for Free →