Key Takeaways for Lowe’s Stock

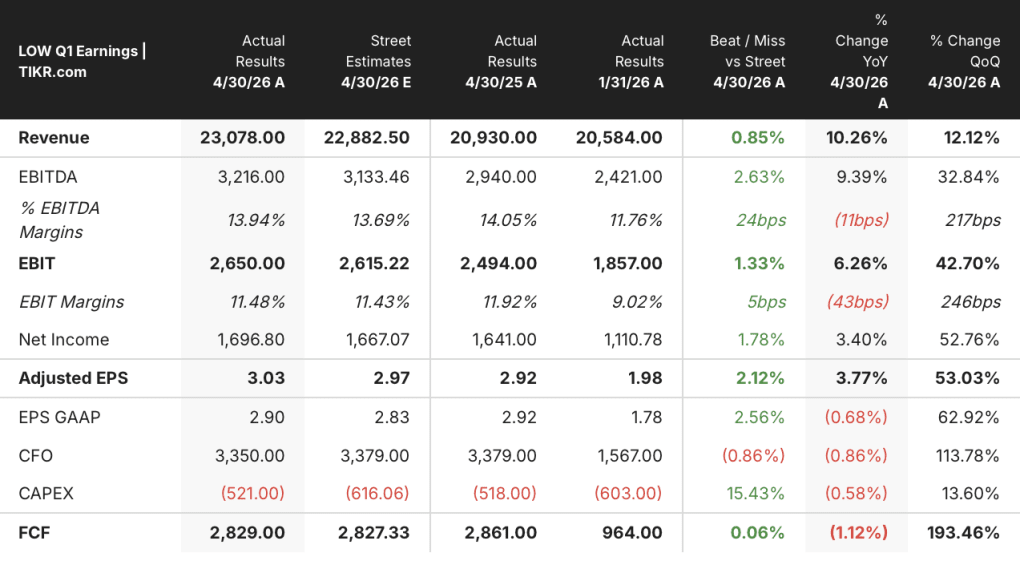

- Lowe’s posted Q1 revenue of $23.1 billion, up 10% year-over-year, beating Street estimates of $22.9 billion.

- Adjusted diluted EPS came in at $3.03, up from $2.92 in the prior-year period, beating consensus by approximately 2%.

- Adjusted operating margin landed at 11.5%, down 43 basis points versus last year, driven by FBM and ADG acquisition dilution.

- TIKR’s model values LOW stock at approximately $324 by January 2031, implying roughly 47% total return from the current price.

Lowe’s Stock Beats Q1 Estimates as Pro, Online Drive Growth Despite DIY Headwinds

Lowe’s Companies (LOW) delivered Q1 revenue of $23.1 billion following its May 2026 earnings call, beating Street expectations as the home improvement retailer extended its streak of positive comparable sales to four consecutive quarters.

The company is the second-largest home improvement chain in the United States, selling products and services to both do-it-yourself consumers and professional contractors.

Comparable sales grew 0.6% in the quarter, with February dragged down by winter storms before accelerating sharply through March.

Online sales grew 15.5% in Q1, powered by loyalty program enhancements, improved fulfillment, and Mylow, the company’s AI-powered shopping assistant.

Mylow now handles over 1 million customer inquiries per month, and CEO Marvin Ellison noted that online customers using Mylow convert at triple the rate of those who do not.

Pro, home services, and appliances also contributed to the quarter’s growth, partially offsetting continued pressure in big-ticket DIY discretionary categories.

Ellison captured the macro tension directly and said on Q1 earnings call: “We’ve delivered 4 quarters of positive comps in an environment where the DIY has faced more economic pressure than I’ve ever seen before.”

Management reaffirmed full-year fiscal 2026 guidance for sales of $92 billion to $94 billion and adjusted diluted EPS of approximately $12.25 to $12.75.

The acquisitions of Foundation Building Materials (FBM) and Artisan Design Group (ADG), two building materials distribution businesses targeting new residential and commercial construction, are on track for integration and positioned to capture demand as housing starts recover.

Lowe’s Gross Margin Compressed as Acquisitions Dilute the Income Statement in Q1

Lowe’s gross margin contracted in Q1 as the FBM and ADG acquisitions introduced structurally lower-margin revenue into the income statement.

Gross margin came in at 32.7% for the quarter, down from 33.8% in the comparable prior-year period.

The 11% revenue growth from $20.9 billion to $23.1 billion year-over-year masked the dilutive margin mechanics underneath.

Gross profit reached $7.54 billion in Q1, up 8% from the year-earlier quarter.

SG&A held at $4.42 billion in the quarter, and operating expenses as a whole rose to $4.99 billion from $4.49 billion a year ago.

Operating income landed at $2.55 billion, up approximately 2% year-over-year.

Operating margin compressed to 11.1% from 11.9% in Q1 of the prior fiscal year, with the acquisition-driven dilution the primary driver rather than underlying cost deterioration.

CFO Brandon Sink confirmed that the company’s perpetual productivity improvement (PPI) initiatives, which are internally funded operational efficiency programs, continue to deliver offsetting benefits, and that acquisition margin dilution is expected to anniversary in the second half of fiscal 2026.

Lowe’s Trails Fastenal by 12 Points on Gross Margin, but Leads Home Depot by Less Than 1

Lowe’s posted a gross margin of 33% in its most recent quarter, sitting nearly identical to Home Depot’s (HD) 33% and roughly 12 points below Fastenal’s 45%.

The Lowe’s-versus-HD gap has been essentially flat across eight consecutive quarters, with both retailers holding within a point of each other through the full period shown in the data.

On the other hand, Fastenal’s (FAST) structural 12-point gross margin advantage reflects a fundamentally different business model, one built on industrial distribution with higher-margin fasteners and supply chain services, making that gap a business model comparison rather than a competitive indictment of Lowe’s pricing power.

The more meaningful signal for Lowe’s stock is that its gross margin of 33% in Q1 fiscal 2027 matches Home Depot’s 33% almost precisely, which means the acquisition-driven compression visible in the income statement has not yet opened a structural gap between the two home improvement retailers.

Is Lowe’s Stock Undervalued? TIKR’s $324 Target Implies 47% Upside If Margins Recover

TIKR’s model values Lowe’s at approximately $324 by January 2031, implying around 47% total return from the current price of $220, or roughly 9% per year.

The credibility of that target depends on the gross margin trajectory established in the income statement reversing its acquisition-driven compression as FBM and ADG anniversary.

Lowe’s operating leverage story is already visible, with PPI initiatives holding SG&A in line even as revenue expanded by more than $2 billion year-over-year, and that structural cost discipline is the income statement mechanism the TIKR target assumes persists.

If gross margins recover toward the 33% to 34% range Lowe’s held before the acquisitions closed, the operating income expansion required to support the target price is directly implied by the cost base already in place.

Should You Invest in Lowe’s Companies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lowe’s Companies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lowe’s Companies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LOW stock on TIKR for Free →