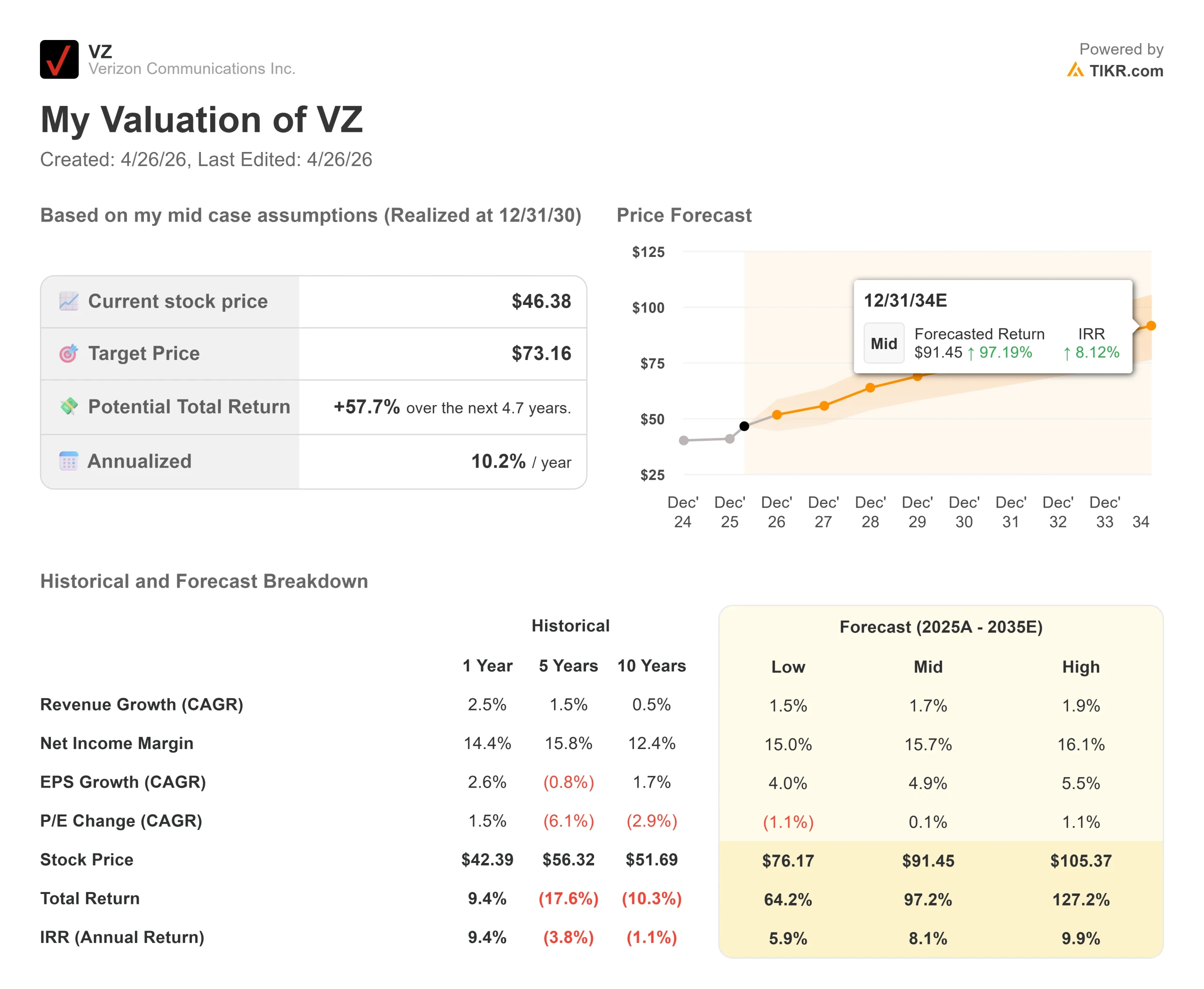

Key Stats for Verizon Stock

- Current Price: $46.38

- Target Price (Mid): ~$73

- Street Target: ~$52

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

- Most Recent Earnings Reaction: +0.20% (January 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Verizon (VZ) stock has spent most of the past five years rewarding patience rather than conviction. That changed in January 2026, when the company reported its strongest quarterly subscriber additions since 2019 and closed a $20 billion acquisition that doubled its fiber footprint overnight. The stock jumped toward a 2026 high of $51.68 before pulling back to $46.38, sitting about $5 below where the Street thinks it belongs.

The bulls point to a management team that is executing. The bears point to $165.8 billion in net debt and a churn rate that rose in Q4 2025.

The single unresolved question: can CFO Anthony Skiadas deliver the cost and volume targets he outlined in detail at the Deutsche Bank Media, Internet & Telecom Conference on March 10?

Skiadas was unusually direct. He described four concrete pillars: $5 billion in cost savings, a capital budget refocused entirely on mobility and broadband, 750,000 to 1 million postpaid net additions in 2026 (two to three times the 2025 total), and at least 7% free cash flow growth to a floor of $21.5 billion.

One risk has not gone away. On January 14, a software issue in Verizon’s 5G Standalone core disrupted service for over 1.5 million customers for more than 10 hours, and the FCC’s Public Safety and Homeland Security Bureau launched a formal investigation. For a turnaround built on improving customer experience and reducing churn, the timing was poor. Q1 2026 earnings on April 27 will be the first read on whether the outage affected subscriber behavior.

See historical and forward estimates for Verizon stock (It’s free!) >>>

Is Verizon Undervalued Today?

At $46.38, Verizon trades at 9.4x forward earnings and 6.8x forward EV/EBITDA, with a 6.1% dividend yield and a 9.2x forward market cap to free cash flow multiple. The Street’s mean target is $51.58, implying around 11% upside before dividends. Of 25 covering analysts, 11 rate it Buy or Outperform, and 14 rate it Hold. Nobody has a Sell.

For comparison, AT&T trades at around 7x forward EV/EBITDA at $26.20, and Comcast sits at around 5x at $27.56. Verizon’s premium to both is modest and reflects scale. The question is whether the convergence thesis earns a further re-rating.

The case for re-rating starts with the cost program. Skiadas detailed exactly where the $5 billion comes from: legacy copper network decommissioning, reducing inbound customer service calls through AI and experience improvements, IT stack consolidation, real estate rationalization, and the 13,000 workforce reductions from Q4 2025, most of whom were off payroll by Q1 2026. Frontier synergies are on top of that, with the target doubled to at least $1 billion in run-rate operating expense savings by 2028.

The more important data point is what Skiadas said about converged customers, those who bundle Verizon wireless with home fiber. They churn at a rate 30% lower than standalone wireless subscribers.

That is the core logic behind the $20 billion Frontier acquisition: the combined bundle makes customers structurally stickier. In Verizon’s most mature Fios markets, fiber penetration runs in the high 40% range. The Frontier footprint is far below that today, which means there is a long runway of convergence-driven churn improvement still ahead.

There is also an angle the market is not fully pricing in. Verizon’s AI Connect service uses the company’s dark fiber and wavelength infrastructure to deliver high-capacity routes to hyperscaler data centers. Verizon and AWS announced an agreement to build new long-haul fiber routes connecting AWS data center locations, and Skiadas confirmed at Deutsche Bank that additional hyperscaler deals are signed.

He called the margins attractive and described AI Connect as a potential offset to the legacy wireline declines that have pressured the Business segment for years.

The risks are real. Net debt stands at $165.8 billion, and the Frontier deal added about 0.25 turns of leverage above Verizon’s long-term unsecured target of 2.0x to 2.25x. Skiadas guided a return to that range by 2027, meaning debt paydown competes with buybacks for free cash flow for the next 18 months.

Interest expense runs near $7.5 billion annually through mid-decade, and wireless service revenue faces about 180 basis points of headwind in 2026 from lapping prior-year pricing actions.

See how Verizon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $46.38

- Target Price (Mid): ~$73

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Verizon stock (It’s free!) >>>

The TIKR mid-case model targets around $73 by 12/31/30, implying roughly 58% total return and a ~10% annualized IRR from today’s price. The two revenue drivers are broadband subscriber growth across the combined Frontier and Fios fiber platform and wireless service revenue recovery as churn improves. Net income margin expands toward around 16%, supported by the $5 billion cost program and Frontier synergies ramping toward $1 billion by 2028.

The primary risk to the model is the churn recovery stalling. That could happen if the January outage leaves a lasting mark on subscriber behavior, if competitors match Verizon’s convergence offers before the Frontier integration completes, or if interest expense runs above guidance. Any of those outcomes delays the timeline but does not change the structural case: Verizon has the fiber asset, the network scale, and the free cash flow to fund the return.

Conclusion

The metric to watch on April 27 is postpaid phone churn. Skiadas said a 5 basis point improvement in churn gets Verizon more than halfway to its 2026 net add target. If Q1 churn held flat or improved despite the January outage, the transformation thesis earns its first proof point. If it rose, the timeline extends.

At $46.38, Verizon offers a 6.1% dividend, a board-authorized $25 billion buyback over the next three years, 30 million fiber passings, and a CFO who laid out the mechanics of a real restructuring with unusual specificity. The TIKR mid-case points to around $73 by 12/31/30. Patient investors are being paid to wait.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Verizon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Verizon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Verizon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Verizon on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!