Key Stats for CVS Health Stock

- 52-Week Range: $58 to $85

- Current Price: $78

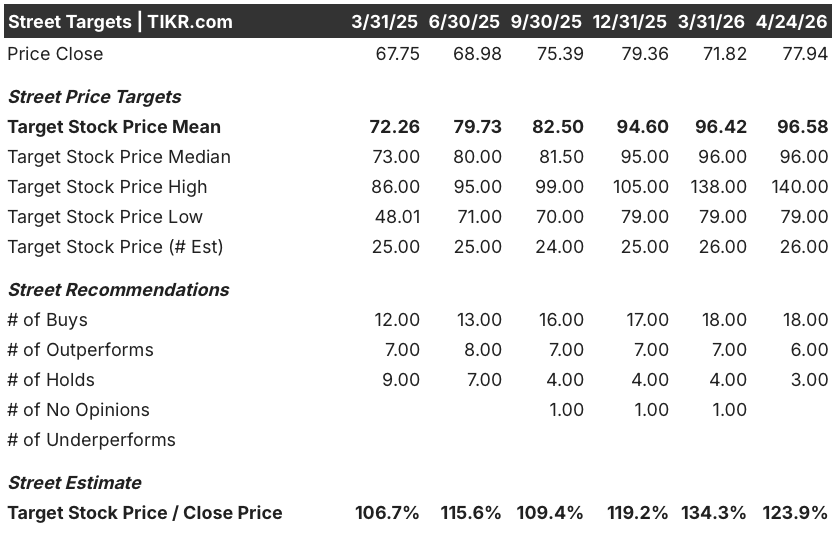

- Street Mean Target: $97

- Street High Target: $140

- Analyst Consensus: 18 Buys, 6 Outperforms, 3 Holds

- TIKR Model Target (Dec. 2030): $125

What Happened?

CVS Health Corporation (CVS) is one of the largest healthcare companies in the United States, operating a pharmacy benefits manager in Caremark, a national insurance business in Aetna, and roughly 9,000 retail pharmacy locations under the CVS Pharmacy banner.

The story entering 2026 is a recovery, not a turnaround attempt.

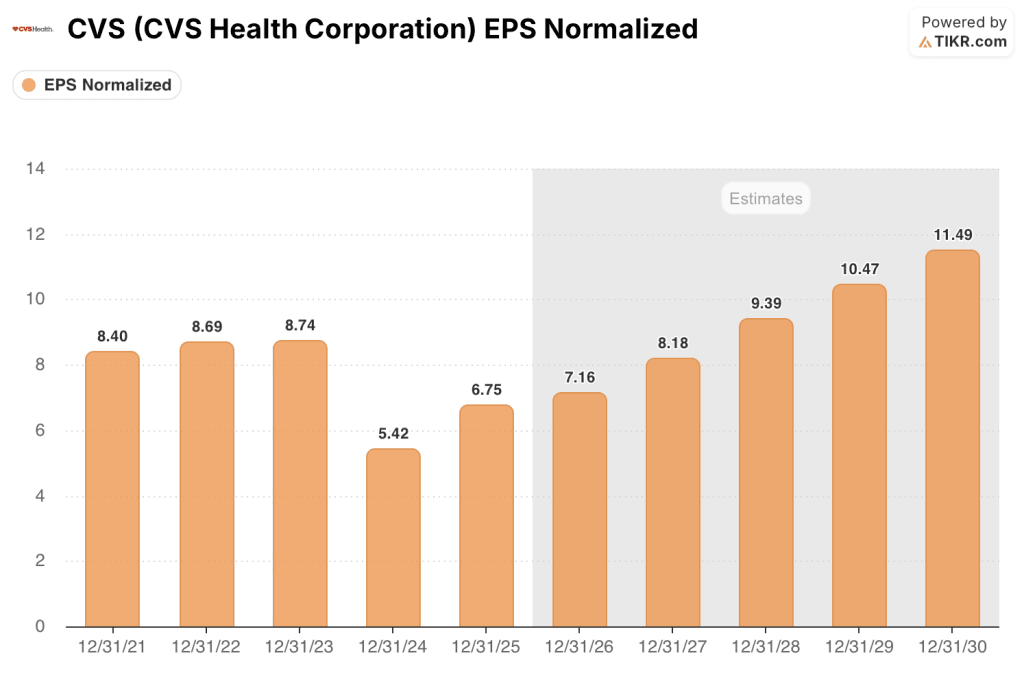

CVS delivered full-year 2025 adjusted EPS of $6.75, exceeding its own initial guidance by approximately 15%.

That beat came despite a genuinely difficult environment: elevated medical cost trends, Medicare Advantage rate pressure, and a Medicaid business absorbing higher-acuity member shifts across multiple states.

The single most important number out of 2025 was Aetna’s performance: the Health Care Benefits segment delivered a year-over-year adjusted operating income improvement of over $2.6 billion, pulling the division from a loss position toward the path CEO David Joyner has called a return to “target margins.”

Joyner, closing out his first full year at the helm, said on the Q4 2025 call: “We still have an incredible amount of earnings power to unlock across our diversified business, but our progress to date has been impressive.”

On April 6, CMS finalized a 2.48% average payment rate increase for Medicare Advantage plans in 2027, well above the near-flat 0.09% initially proposed in January, representing more than $13 billion in additional payments to the industry, which sent CVS Health stock up nearly 7% in a single session.

Aetna followed that macro tailwind with its own operational signal: as of April 24, the unit reported it had standardized 88% of its prior authorization volume, with more than 95% of eligible requests completed within 24 hours and 83% processed in real time.

On the pharmacy side, CVS opened its first pharmacy-only location in Chicago in late March, the first of nearly 20 planned for 2026, targeting a smaller neighborhood format averaging roughly 3,000 square feet focused exclusively on pharmacist-led care.

The Pharmacy and Consumer Wellness segment closed 2025 with over $6 billion in adjusted operating income, a 4.5% year-over-year increase, and management set the long-term outlook for this business to at least flat earnings annually going forward.

CVS also reached a proposed FTC settlement on insulin pricing in late March, removing a regulatory overhang that had clouded the PBM business.

The company reaffirmed full-year 2026 adjusted EPS guidance of $7 to $7.20 and updated its 2026 operating cash flow outlook to at least $9 billion.

Wall Street’s Take on CVS Stock

The Medicare Advantage rate improvement reframes the 2027 margin debate, but the more durable argument for CVS Health stock sits in what the earnings trajectory already proves about 2025 and 2026.

CVS’s normalized EPS hit $6.75 in 2025, up around 25% from the 2024 trough of $5.42, and consensus now projects around $7 in 2026 and around $8 in 2027, a recovery arc that makes the current multiple look structurally mispriced relative to the company’s embedded earnings power.

Of 27 analysts covering CVS Health stock, 18 rate it a Buy, 6 an Outperform, and 3 a Hold, with a mean price target of around $97 implying roughly 24% upside; what the Street is specifically waiting for is confirmation that Medicare Advantage margins can sustain improvement into 2027 given a rate environment that, while better than feared, remains below the level management considers adequate.

The high target of $140 suggests at least one analyst is modeling a scenario in which the enterprise multiple re-rates materially as Aetna reaches target margins, while the low of $79 reflects a camp that believes medical cost trends could re-accelerate and cap near-term EPS.

Priced at roughly 11x the 2026 consensus EPS estimate against a recovery taking normalized earnings from $5.42 in 2024 toward around $8 by 2027, CVS Health stock appears undervalued relative to the scale of the earnings rebound already underway, particularly as Aetna’s $2.6 billion AOI improvement in 2025 removes the central uncertainty that caused the multiple to collapse two years ago.

The April 7 Medicare Advantage rate finalization is not just a sentiment catalyst: it provides Aetna with a more predictable cost model for 2027 plan bids, which structurally reduces the earnings variability the market has been discounting into the multiple.

The risk is that medical cost trends, while in line with expectations through Q4 2025, remain elevated across all product lines, and any re-acceleration would compress the margin recovery timeline and delay the P/E re-rating the thesis depends on.

The catalyst is the Q1 2026 earnings call on May 6, where the medical benefit ratio trajectory across Aetna’s segments will either confirm that trend assumptions are holding or force a guidance revision that resets the recovery narrative.

What Does the Valuation Model Say?

The TIKR model’s $125 mid-case target, implying roughly 61% total return over approximately 5 years at an annualized rate of around 11%, rests on a revenue CAGR of around 4% through 2030 and a net income margin expanding from 1.8% in 2025 to around 2.6% at mid-case: modest top-line assumptions paired with a margin recovery that the 2025 results have already partially validated.

At roughly 11x forward earnings on a business delivering around 14% EPS growth annually through 2028, with Aetna’s $2.6 billion operating income improvement already banked and a pharmacy segment committed to at-least-flat earnings indefinitely, CVS Health stock appears undervalued against an earnings recovery that is no longer speculative.

The question CVS Health stock forces is whether the 11x multiple reflects a business in durable recovery or one still one bad trend quarter away from replicating 2024’s collapse.

The Opportunity

- Normalized EPS recovered from $5.42 in 2024 to $6.75 in 2025, a 24.5% rebound, with consensus projecting around $7 in 2026 and around $8 in 2027, building toward a multi-year CAGR of around 14% through 2028

- Aetna delivered over $2.6 billion in adjusted operating income improvement in 2025, with management guiding for continued margin progress across Medicare, Medicaid, and commercial lines in 2026

- The April 7 CMS finalization of a 2.48% Medicare Advantage rate increase (total effective increase of around 5% including risk assessment adjustments) gives Aetna a more stable planning base for 2027 bids

- Aetna standardized 88% of prior authorization volume as of April 24, with 95% of eligible requests completed within 24 hours and 83% processed in real time, reducing administrative friction that contributed to margin compression in 2023 and 2024

- CostVantage reimbursement transition is complete across all commercial, Medicare, and Medicaid lines, locking the Pharmacy and Consumer Wellness segment into a predictable per-script margin model with at-least-flat earnings as the permanent baseline

The Risk

- Medical cost trends remain elevated across all product lines, and management has explicitly said it would need to see a “durable and persistent break” in trend before changing its cautious forecast assumptions: if Q1 2026 trends re-accelerate, the Aetna margin timeline extends and the around $8 EPS estimate for 2027 becomes less reliable

- The 2027 Medicare Advantage rate at 2.48%, while better than January’s 0.09% proposal, remains below what CVS management considers adequate for current medical cost trends, creating ongoing bid discipline risk and potential Medicare membership pressure as Aetna continues repricing its individual and group MA products

- The Teamsters strike authorization at the Fredericksburg, Virginia distribution center, covering over 500 drivers and warehouse workers ahead of a May 1 deadline, introduces a near-term logistics risk across mid-Atlantic stores and pharmacies, even with CVS stating contingency replenishment plans are in place

Should You Invest in CVS Health Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CVS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CVS Health Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CVS stock on TIKR for Free →