Key Stats for Zscaler Stock

- Past week’s performance: consolidating

- 52-week range: $115 to $337

- Valuation model target price: $201

- Implied upside: 48.8% over 2.3 years

Value your favorite stocks like Zscaler with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Zscaler (ZS) stock was mostly flat this week, but shares remain under pressure after a sharp multi-month reset from prior highs near $337 to around $136. Investors appear cautious because high-growth software valuations compressed across 2026, especially after renewed debate around how AI could disrupt legacy software pricing models. Reuters reported broader software weakness in April as AI concerns hit the group.

Company-specific headlines also weighed on sentiment. Reuters reported on April 17 that EVP of Corporate Strategy Raj Judge resigned and exited the board. Leadership changes do not always alter fundamentals, but they can create uncertainty when a stock is already weak.

Earlier this quarter, Zscaler reported fiscal Q2 adjusted EPS of $1.01, ahead of the $0.90 consensus estimate. Even so, Reuters also noted shares dipped after the release as investors focused on a wider quarterly loss tied to higher spending. That suggests the market wants profitable growth, not just revenue beats, going forward.

Importantly, demand for cybersecurity has not disappeared. Zscaler sells cloud-based zero-trust security tools that help companies secure users and data without relying on traditional network perimeters. So while sentiment has weakened, the next move likely depends on whether growth reaccelerates and margins improve going forward.

See analysts’ growth forecasts and price targets for Zscaler (It’s free) >>>

Is Zscaler Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 21%

- Operating Margins: 23.5%

- Exit P/E Multiple: 32x

Based on these inputs, the model estimates a target price of $202, implying 48.8% total upside from the current share price and a 19.1% annualized return over the next 2.3 years.

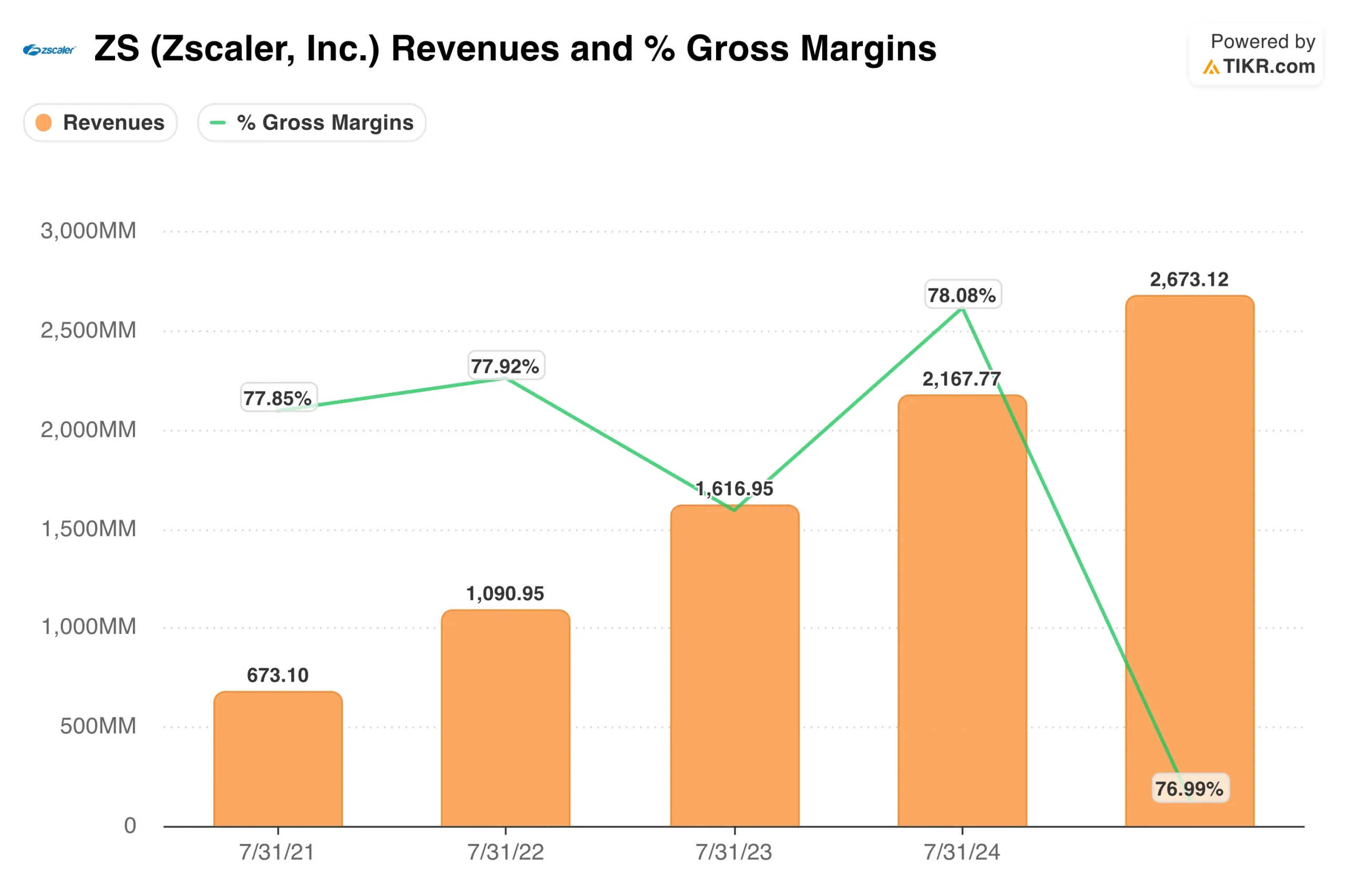

The valuation case starts with growth durability. Revenue rose from $673 million in fiscal 2021 to $2.67 billion in fiscal 2025, while the last twelve months’ revenue reached about $3.0 billion. That scale matters because it shows Zscaler is still gaining adoption despite a tougher software spending backdrop.

Margins are the second key variable. Gross margin remains strong at 76.6%, which is typical of premium software businesses. However, operating margin was negative 4.4% over the last twelve months, so investors want evidence that scale can translate into consistent earnings.

Cash generation supports the bull case. Free cash flow reached $946.8 million LTM, equal to a 31.5% margin. That means the business converts a meaningful share of sales into cash even while GAAP earnings remain pressured by stock compensation and growth spending.

The market still values Zscaler at about 5.6x next twelve-month revenue, well below prior premium software multiples. If growth stabilizes and margins expand, today’s price could reflect execution risk rather than full optimism going forward.

What’s Driving ZS Stock Going Forward?

The next major catalyst is earnings. Zscaler is expected to report fiscal Q3 2026 results on May 29. Investors will likely focus on billings, revenue guidance, and whether management can sustain double-digit growth in a cautious IT spending environment.

AI is both a risk and an opportunity. Some software names were sold off this year on fears that AI could compress pricing or reduce seat counts. But cybersecurity may also benefit because AI increases threat complexity and creates new demand for automated protection tools.

Partnership execution also matters. Reuters reported recent partnership announcements involving Singtel Singapore and Tata Consultancy Services. Deals like these can expand distribution, especially with global enterprise customers that need secure cloud networking.

Finally, investors will watch profitability discipline. If Zscaler can pair 20%+ growth with expanding operating margins, sentiment could improve quickly. If spending rises faster than revenue again, the stock may remain volatile going forward.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Zscaler?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ZS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ZS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Zscaler stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!