Key Stats for Lowe’s Stock

- Past week’s performance: -3%

- 52-week range: $210 to $293

- Valuation model target price: $320

- Implied upside: 31.0% over 2.8 years

Value your favorite stocks like LOW with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lowe’s (LOW) stock fell about 3% this week, with shares closing near $244. The move came as investors continued to weigh solid company execution against a still-pressured housing market. Lowe’s recently said Q4 comparable sales rose 1.3%, helped by Pro, online, home services, and holiday demand.

The concern is that management’s 2026 outlook still reflects uncertainty in home improvement demand. Lowe’s guided for total sales of $92 billion to $94 billion, but comparable sales are expected to be flat to up 2%. That means the market is not yet pricing in a strong housing-led recovery.

CEO Marvin Ellison said the housing macro remains pressured, but Lowe’s is focused on productivity initiatives and taking share. That message helped frame the stock’s pullback as a debate over timing, not a collapse in execution. Investors appear to be waiting for clearer signs that big-ticket DIY spending is improving.

The stock also remains sensitive to cost actions. In February, Lowe’s eliminated about 600 corporate and support roles, equal to less than 1% of its workforce, to better support stores and frontline employees. That reinforces the market’s focus on margin protection if Lowe’s stock faces softer demand going forward.

See analysts’ growth forecasts and price targets for LOW (It’s free) >>>

Is Lowe’s Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.3%

- Operating Margins: 12.1%

- Exit P/E Multiple: 19.4x

Based on these inputs, the model estimates a target price of $320, implying a 31.0% total return from the current share price of $244 and an annualized return of 10.2% over the next 2.8 years.

That expected return is attractive but not aggressive. Lowe’s trades at about 19.4x next-twelve-month earnings, which is close to the model’s exit multiple. The valuation, therefore, depends more on steady earnings growth than multiple expansion.

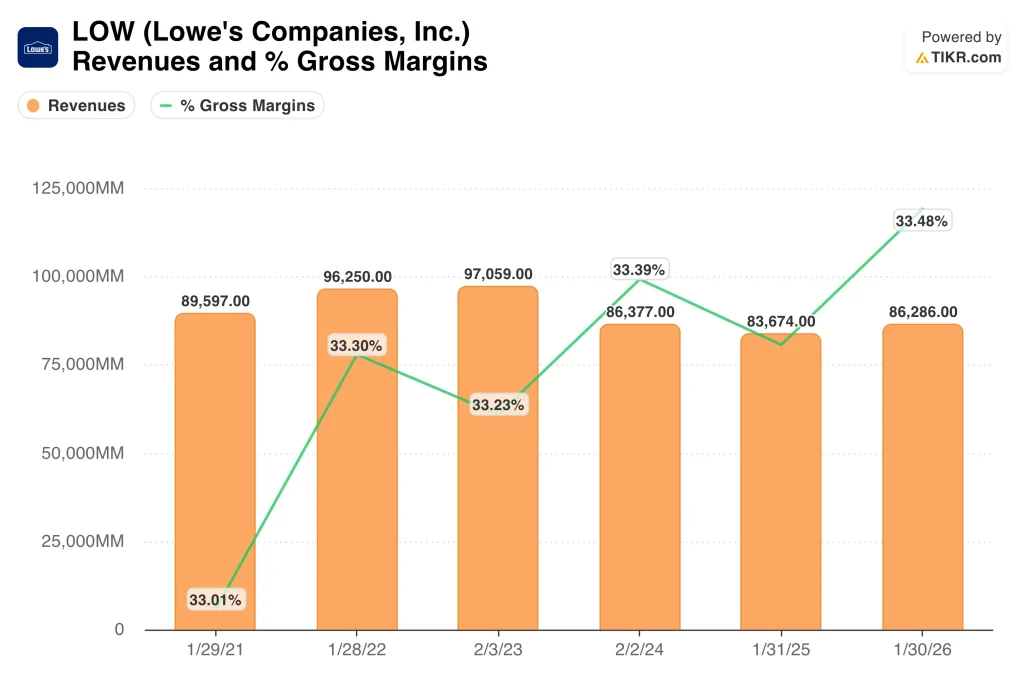

The business still has durable cash generation. Fiscal 2025 sales rose 3.1% to $86.3 billion, but net earnings fell 4.4% to $6.7 billion. Comparable sales increased just 0.2%, as a higher average ticket offset fewer transactions.

Margins remain the key swing factor. Lowe’s LTM gross margin is 33.5%, and its operating margin is 11.8%. If Pro demand, online sales, and productivity initiatives support margins, the current valuation can work even without a sharp housing rebound.

What’s Driving Lowe’s Stock Going Forward?

The biggest catalyst is the next earnings update, expected on May 20, 2026. Investors will watch whether comparable sales stay positive and whether management keeps the full-year outlook intact. A stronger Pro customer trend could help offset weaker discretionary DIY projects.

Housing remains the main external driver. Lowe’s sells products tied to repairs, remodeling, seasonal projects, and professional construction work. So higher mortgage rates or weak home turnover can pressure big-ticket categories, while repair and Pro demand can provide stability.

Capital returns also matter for the stock. Lowe’s declared a $1.20 quarterly dividend payable May 6, 2026, to shareholders of record on April 22. The company also paid $2.6 billion in dividends during fiscal 2025, showing that shareholder returns remain a core part of the story.

The path forward depends on whether Lowe’s can protect profitability while demand normalizes. Management is leaning on productivity, Pro growth, online sales, and home services to support earnings.

If those drivers hold, the stock’s 10.2% modeled annual return could stay credible going forward.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Lowe’s Companies?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LOW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track LOW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lowe’s stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!