Key Stats for Snap Stock

- Current Price: $5.65

- Street Target (Mean): ~$8

- TIKR Model Target Price: ~$72

- Potential Total Return (bull scenario): ~1,179%

- Annualized IRR (bull scenario): ~158% / year

- Q4 2025 Earnings Reaction: -13.37% (February 4, 2026)

- Max Drawdown: -62.03% (March 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Snap (SNAP) stock fell 62.03% from its peak by March 27, 2026, as three headwinds hit the company in rapid succession.

The first hit came on February 4, when Snap reported Q4 2025 earnings.

Revenue of $1.72 billion beat estimates, and the company posted its first-quarter GAAP net income of $45 million. But global daily active users fell by 3 million quarter over quarter to 474 million, and Q1 2026 guidance of $1.50 billion to $1.53 billion landed below analyst expectations. The stock fell 13.37% that day.

Three weeks later, the European Commission opened a formal investigation into Snapchat under the Digital Services Act (DSA), the EU’s framework requiring large platforms to protect users from harmful content, citing concerns about child grooming, inadequate age verification, and the sale of illegal goods. Then the planned $400 million Perplexity AI integration stalled after both parties failed to agree on a path to broader rollout, as CFO Derek Andersen confirmed on the Q4 earnings call.

On April 15, Snap announced it was cutting roughly 1,000 full-time employees and closing more than 300 open roles, about 16% of its global workforce, targeting annualized cost savings of more than $500 million by the second half of 2026. Shares jumped approximately 7% to 8% that day. From the March lows near $4, the stock has since recovered to $5.65, a bounce of more than 40%.

CEO and Co-Founder Evan Spiegel framed the cuts in terms of AI efficiency.

In the SEC-filed memo to employees, Spiegel wrote that “rapid advancements in artificial intelligence enable our teams to reduce repetitive work, increase velocity, and better support our community, partners, and advertisers.”

On the Q4 earnings call, he had already flagged that AI was generating roughly 40% of new code at Snap, rising to over 65% by the time of the April announcement.

See historical and forward estimates for Snap stock (It’s free!) >>>

Is Snap Undervalued Today?

The stock has bounced 40% off its lows, but it still trades at $5.65 against a Street mean target of around $8. That gap reflects real tension between what the business is becoming and what it still needs to prove.

Snapchat+ subscribers grew 71% year-over-year to 24 million in Q4, and the subscription-driven segment grew 62% year-over-year to $232 million in revenue.

On the advertising side, total active advertisers were up 28% year-over-year in Q4, with small and medium-sized businesses (SMBs) driving the majority of ad revenue growth for the sixth consecutive quarter. Full-year 2025 free cash flow reached $437 million, nearly doubling year-over-year. These are reported results, not projections.

CEO Evan Spiegel outlined the gross margin path on the Q4 call: “as more of our ad revenue is derived from higher-margin placements such as Sponsored Snaps and Promoted Places, we expect advertising margins to improve.” Combined with a subscription business running on existing infrastructure, management has set a specific target of exceeding 60% gross margins in 2026, up from 59% in Q4 and 55% in Q3.

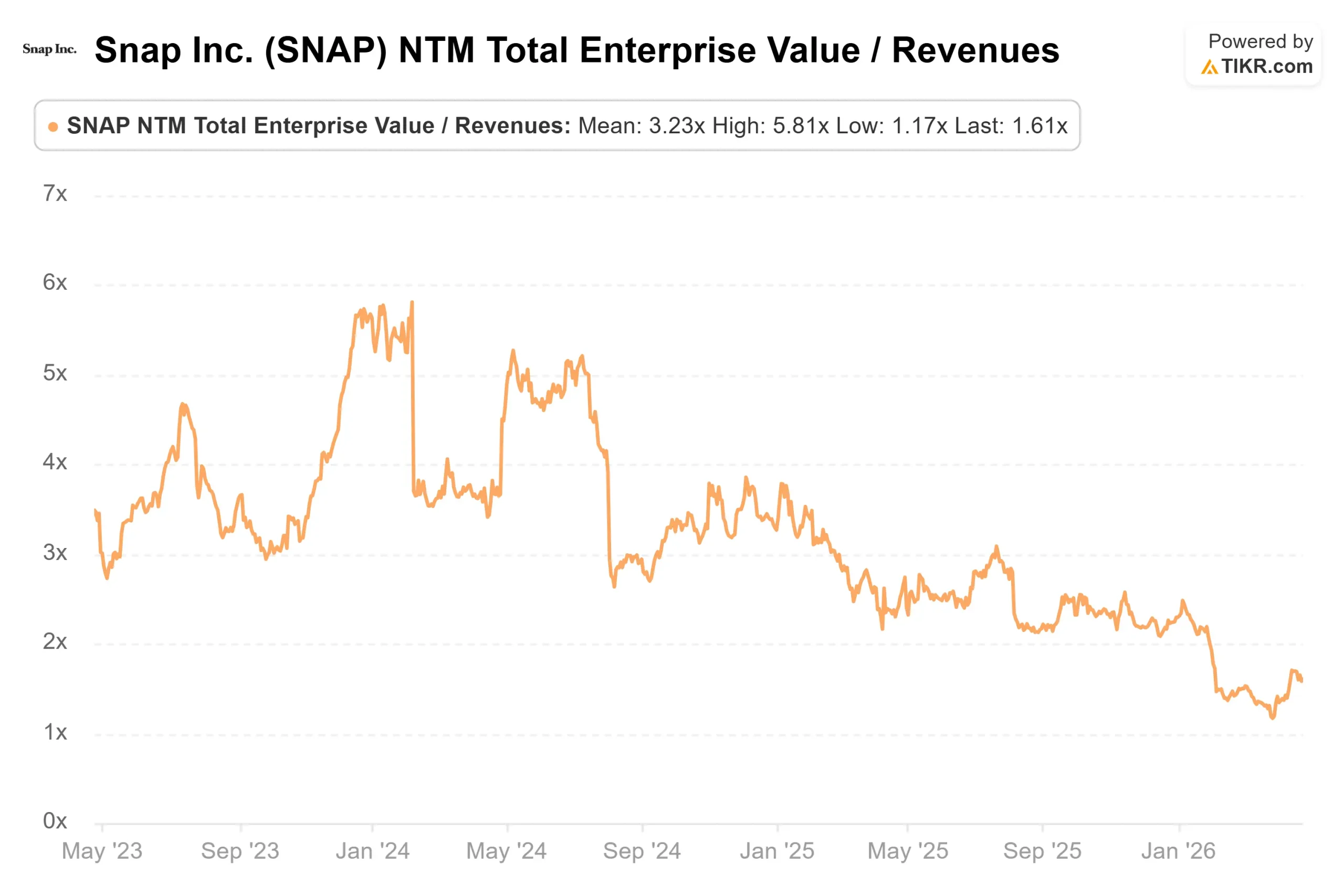

On valuation multiples, Snap currently trades at 9.60x NTM EV/EBITDA and 1.61x NTM EV/Revenue. Per TIKR’s Competitors page, Pinterest trades at 7.66x NTM EV/EBITDA and 2.21x NTM EV/Revenue, while Alphabet trades at 18.72x and 8.67x respectively. Snap’s revenue multiple looks cheap by comparison, but Pinterest is GAAP profitable and carries no active regulatory probe. The discount reflects execution risk, not a simple mispricing.

The risk picture is real.

The EU DSA investigation carries a potential fine ceiling of up to 6% of global annual revenue. At Snap’s 2025 revenue base of $5.93 billion, that ceiling is around $356 million.

North American DAUs declined again in Q4 to 94 million, the company’s most monetizable user base. The CFO transition, with Andersen departing May 8, adds uncertainty at a critical moment. And 30 of the 43 analysts covering SNAP rate it Hold, reflecting a market waiting for proof before committing.

See how Snap performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $5.65

- TIKR Model Target (Bull scenario): ~$72

- Potential Total Return: ~1,179%

- Annualized IRR: ~158% / year

See analysts’ growth forecasts and price targets for Snap stock (It’s free!) >>>

The TIKR bull scenario requires revenue growing at around 9% CAGR, driven by continued SMB advertiser growth and Snapchat+ subscriber expansion, alongside a meaningful P/E re-rating as GAAP profitability becomes consistent. Street consensus for NTM EBITDA has already moved from around $546 million at Q1 2025 to around $1.12 billion today, per TIKR’s Multiples page, reflecting some early confidence in the margin story.

The downside is straightforward: if the EU probe escalates into material fines, North American DAUs continue to decline, and the multiple stays compress at current levels, the restructuring savings alone are not enough to drive a re-rating. The 2.7-year timeline to December 2028 leaves limited room for execution slippage.

Conclusion

The number to watch at Snap’s Q1 2026 earnings on May 6 is North American DAU. A stabilization or reversal from 94 million would signal that the cost cuts did not accelerate user loss in the company’s most valuable market. That is the line between a real turnaround and a margin story built on a shrinking base.

The restructuring is real, the subscriber growth is real, and the free cash flow improvement is real. But the stock has already priced in much of that progress with a 40% bounce. May 6 needs to show the revenue engine is intact underneath the cuts.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Snap?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snap, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snap alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!