Key Takeaways:

- CrowdStrike generated $4.81 billion in revenue in its most recent fiscal year, with gross margins of approximately 75% and a path toward GAAP operating profitability, while SentinelOne crossed $1 billion in revenue for the first time, with matching gross margins of 74%, but still carries a GAAP operating loss of roughly 30%.

- CrowdStrike trades at 18.58x NTM EV/Revenue and 63.09x NTM EV/EBITDA, a meaningful premium to SentinelOne’s 3.52x NTM EV/Revenue and 31.57x NTM EV/EBITDA, reflecting the market’s confidence in CrowdStrike’s execution history and platform breadth.

- Analysts expect both companies to grow revenue at roughly 20% annually over the next two years, but CrowdStrike’s non-GAAP EPS is already $4.85, while SentinelOne’s is $0.34, illustrating where each company is in its profitability arc.

- Under mid-case assumptions, TIKR’s valuation model implies a 22.3% annualized return for CrowdStrike and a 23.8% annualized return for SentinelOne, a surprisingly tight gap that reflects SentinelOne’s lower starting valuation partially offsetting CrowdStrike’s stronger earnings base.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Cybersecurity is one of the few enterprise spending categories that is essentially non-discretionary. You can delay the implementation of a new ERP system. You cannot decide to protect your endpoints less aggressively. That dynamic gives both CrowdStrike (CRWD) and SentinelOne (S) a durable demand backdrop that most software companies would trade anything for.

The question is not whether both businesses will keep growing. They almost certainly will. The question is which one offers the better combination of quality, growth, and valuation relative to where each stock sits today.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Same Category, Different Chapters

CrowdStrike pioneered cloud-delivered endpoint protection and has since expanded into identity security, cloud workload protection, and SIEM. It is the incumbent in this category, the company that set the standard for what a modern endpoint security platform looks like, and it has the revenue base and customer relationships to prove it.

SentinelOne is a similar story told about four years later. Its Singularity platform covers endpoint, cloud, and identity security with an AI-driven architecture, and it has grown impressively from a standing start. What it does not yet have is CrowdStrike’s scale, its profitability, or its decade of enterprise relationships. What it does have is a lower valuation and a longer runway to grow into it.

The Margin Story Is Where They Start to Diverge

This is where the comparison gets interesting, because the stories look similar on the surface and quite different underneath.

SentinelOne has grown from $46 million in revenue in fiscal 2020 to just over $1 billion today, a remarkable rate of expansion. Gross margins have climbed steadily from 60% to 74%, which is a genuine signal of improving unit economics. The operating margin, still at negative 30%, is the unfinished business. The trajectory is moving in the right direction, but profitability at scale is still a forecast, not a fact.

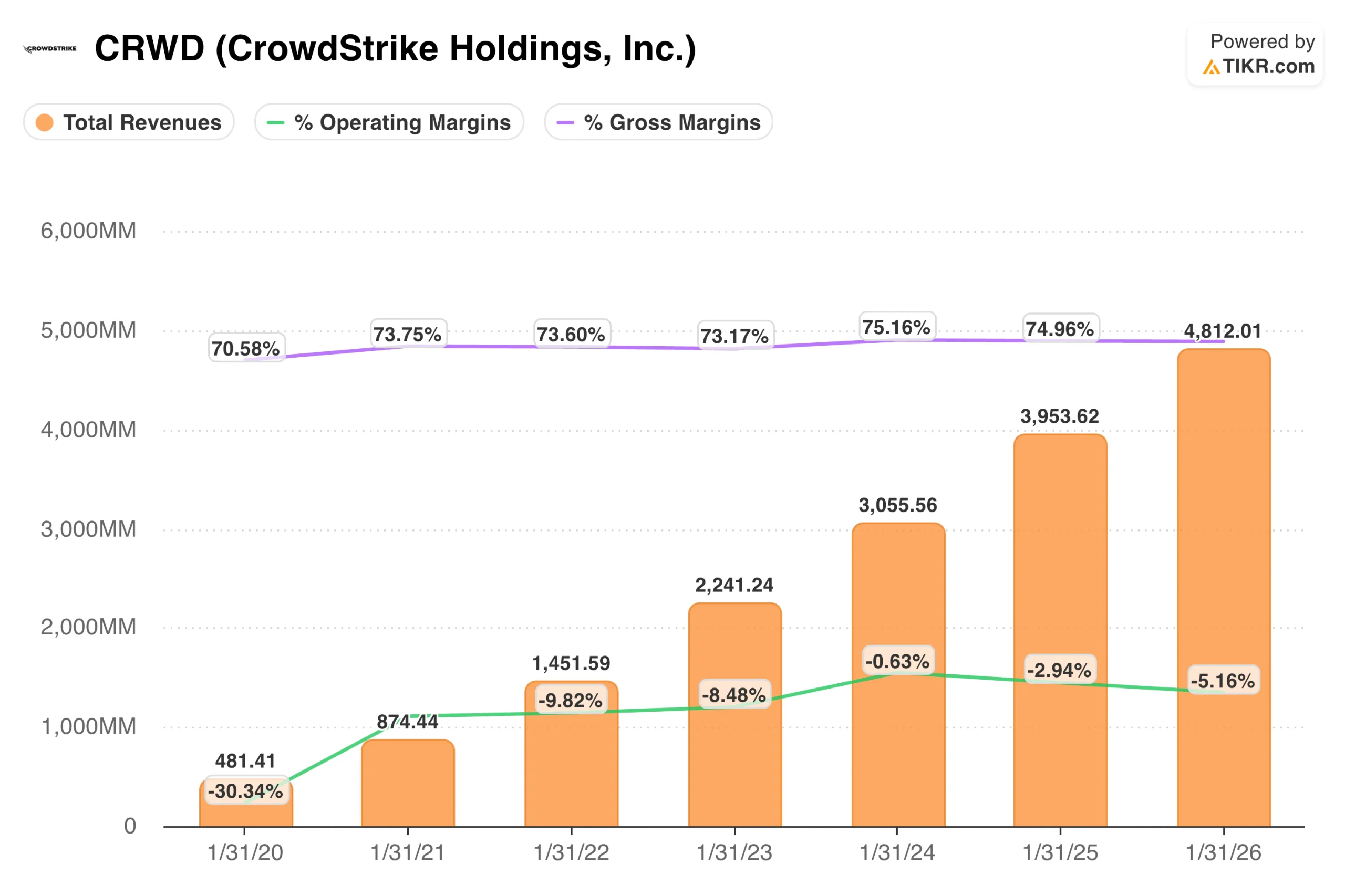

CrowdStrike’s chart tells a more mature version of the same story. Revenue has increased from $481 million to $4.81 billion over the same period, while gross margins have held steady near 75% throughout.

The operating margin has improved from deeply negative to roughly breakeven on a GAAP basis, with non-GAAP profitability already well established. The Falcon outage in mid-2024 created a temporary setback in customer sentiment, but retention held and the business continued to grow, underscoring how embedded the platform is.

One Trades at a Premium. The Other Trades at a Discount. Here’s Why Both Make Sense.

At 18.58x NTM EV/Revenue and 63.09x NTM EV/EBITDA, CrowdStrike is priced as a best-in-class franchise. That premium reflects its market position, platform depth, and proven ability to expand with existing customers. It is not cheap, and it does not pretend to be.

SentinelOne at 3.52x NTM EV/Revenue and 42.05x NTM P/E looks like a very different entry point. The lower revenue multiple reflects both its smaller scale and the uncertainty still embedded in its profitability timeline. For investors willing to bet that SentinelOne continues to close the gap with CrowdStrike, the valuation offers more upside. For investors who want a business with an already proven model, CrowdStrike is the cleaner story.

See what analysts think about CrowdStrike stock right now (Free with TIKR) >>>

What the Numbers Actually Show

Consensus has CrowdStrike growing revenue from $5.9 billion in fiscal 2026 to $7.2 billion in fiscal 2027, a growth rate of roughly 21%. Non-GAAP EPS is expected to reach $4.85 this year and $6.17 next year.

The P/E compresses meaningfully on a two-year forward basis as earnings scale, which is what makes the thesis work even at today’s headline multiples.

For its part, SentinelOne is expected to grow revenue from $1.2 billion to $1.4 billion over the same window, also around 20% annually. Non-GAAP EPS of $0.34 this year, growing to $0.48 next year, shows progress in profitability, but the GAAP picture remains negative for several years.

The Rule of 40 score, which combines revenue growth and free cash flow margin, is approaching but not yet consistently above the threshold that signals a healthy SaaS business.

See analysts’ full growth forecasts and estimates for SentinelOne stock (It’s free) >>>

The Models Are Closer Than You’d Think

TIKR’s mid-case model for CrowdStrike, using 20.2% revenue growth and 23.9% net income margins, points to a target price of $1,174.11 and a potential total return of 162% over the next 4.8 years, or approximately 22.3% annualized. The model assumes modest P/E compression of about 1.1% annually, meaning returns are driven by earnings growth rather than multiple expansion.

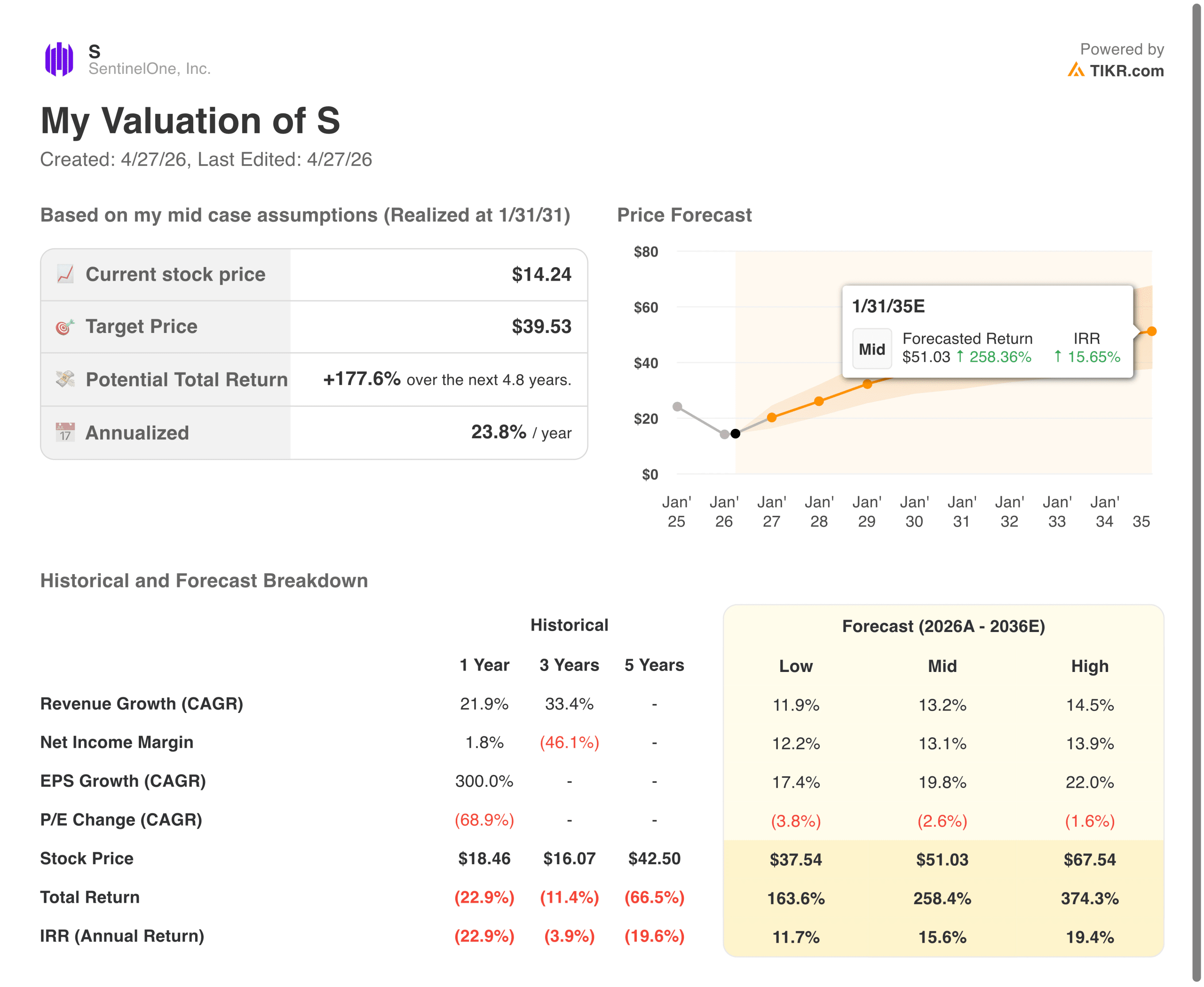

SentinelOne’s mid-case, using 13.2% revenue growth and 13.1% net income margins, implies a target price of $39.53 and a total return of 177.6% over the same horizon, or approximately 23.8% annualized. The model assumes more aggressive P/E compression of 2.6% annually, reflecting the higher starting multiple relative to current earnings.

The models are closer than most investors would expect. CrowdStrike’s higher absolute earnings base and lower valuation risk are partially offset by SentinelOne’s lower entry point and higher percentage upside if the profitability arc plays out as expected.

So, Which One Do You Actually Buy?

CrowdStrike is the business you buy when you want proven execution, platform depth, and a management team that has already navigated a serious reputational event and come out the other side. The premium is real, but so is the track record.

SentinelOne is the bet you make if you believe the endpoint security market is large enough for two dominant players and that SentinelOne’s gross margin profile, now matching CrowdStrike’s, signals the same kind of durable business model operating about four years behind on the maturity curve. The risk is that the profitability timeline slips or that CrowdStrike’s platform advantages prove too wide to overcome competitively.

For a long-term investor comfortable with a range of outcomes, there is a reasonable case for both. The models suggest similar annualized returns. The difference is how much uncertainty you are willing to hold alongside those returns.

Build your own Valuation Model to value any stock (It’s free!) >>>

How Much Upside Does Each Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!