Key Stats for Pinterest (PINS):

- 52-week range: ~$16 – $28

- Current price: $23.20

- Street mean target: ~$28

- Annualized IRR (TIKR mid case): ~18% / year

- Q1 2026 revenue: $1.008B (+18% YoY)

- Q2 2026 revenue guidance: $1.133B – $1.153B

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

A 44% Drawdown on a Platform That Keeps Growing

Pinterest, Inc. (PINS) is a visual discovery platform where more than 630 million people search for ideas across home design, fashion, food, travel, and nearly every consumer category.

The key distinction from other social platforms is intent: Pinterest users are not passively scrolling a feed of content from people they follow. They are actively searching for things they want to buy, build, or do.

Over 80 billion searches happen on the platform every month, with roughly half carrying clear commercial intent. For advertisers who care about reaching consumers at the moment of consideration, Pinterest offers something genuinely different from Meta or TikTok.

The stock has not been rewarded for any of it. A max drawdown of 44.07% hit on February 13, 2026, and while the stock has partially recovered, it remains nearly 16% below where it started this period.

The selloff was not driven by a deteriorating business. Revenue crossed $1 billion in a single quarter for the first time in Q1 2026, up 18% year over year, and the company reported its tenth consecutive quarter of double-digit user growth.

What drove the stock lower was a $47 million restructuring charge and investor impatience with the pace of international monetization, a tension that has followed this stock for years.

CEO Bill Ready put it plainly: “We’re seeing continued momentum driven by our differentiated visual search product experiences.

As we continue building an AI-powered ads platform that delivers performance for advertisers, we remain focused on ensuring monetization more fully reflects the strength of our engagement.” The gap between engagement and monetization is the whole story with Pinterest, and closing it is what the bull case depends on.

See historical and forward estimates for Pinterest stock (It’s free!) >>>

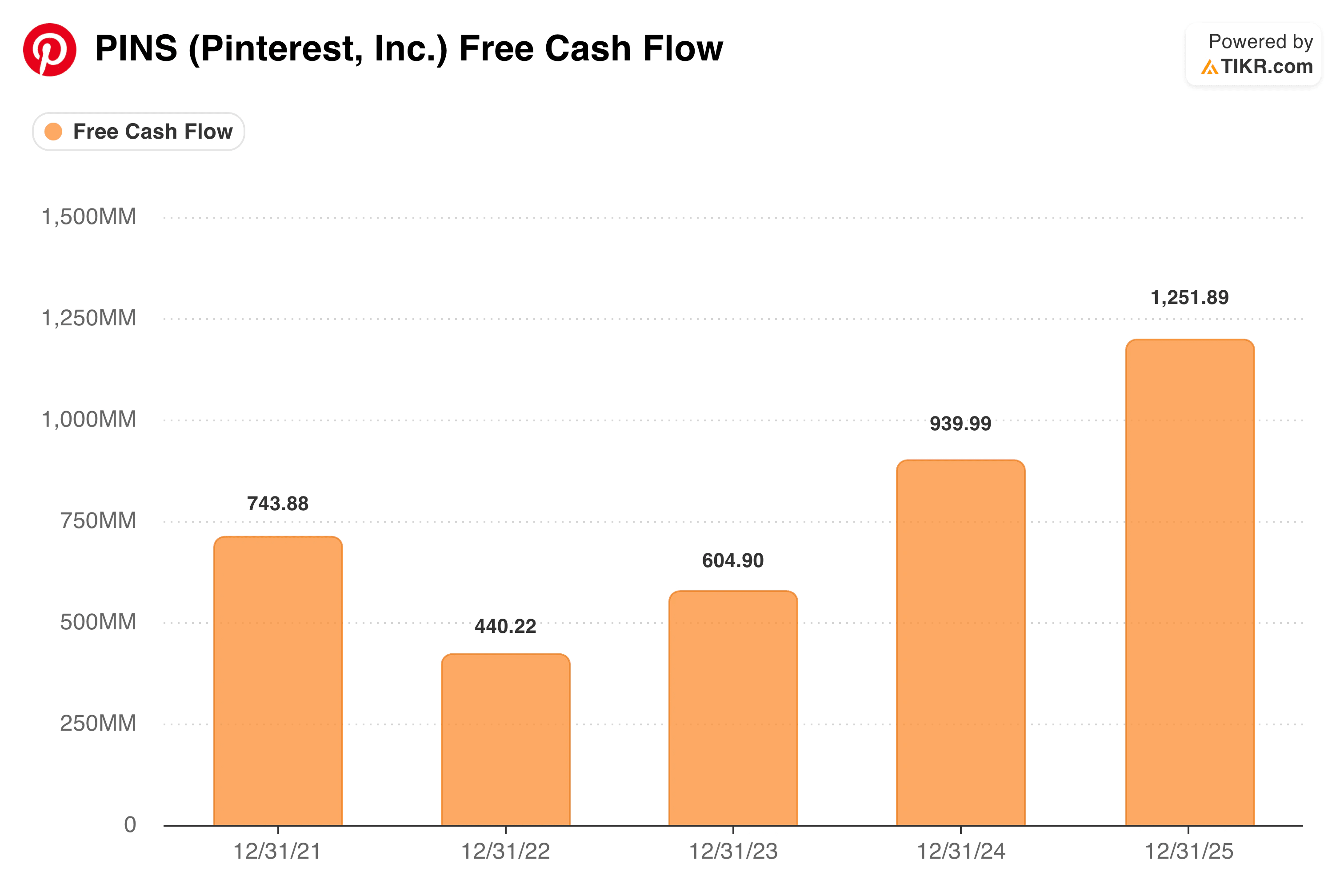

The Free Cash Flow Story the Stock Price Ignores

Whatever the market thinks of Pinterest’s monetization pace, the cash flow numbers are hard to argue with.

Annual free cash flow dipped to $440 million in 2022 during a period of heavy investment, then climbed steadily: $605 million in 2023, $940 million in 2024, and $1.252 billion in 2025.

In Q1 2026 alone, Pinterest generated $312 million in free cash flow. A company producing that kind of cash at a market cap of roughly $14 billion is trading at around 11x trailing free cash flow, a multiple that would look reasonable for a slow-growth industrial business, let alone a platform with 631 million users and growing.

The company has been putting that cash to work aggressively, completing $2 billion in share repurchases in Q1 and issuing convertible notes to fund additional buybacks.

Elliott Management has also taken an activist position, adding further pressure for management to close the gap between the platform’s size and its market value. The advertising tools are getting sharper: Pinterest Performance+, an AI-powered lower-funnel ad product, now manages roughly 30% of lower-funnel ad revenue.

The acquisition of TVScientific adds connected TV targeting capabilities. Europe revenue grew 27% in Q1 and Rest of World revenue grew 59%, both from small bases but moving in the right direction. User growth remains concentrated in international markets where monetization is still early, and that is the honest constraint on the pace of earnings expansion.

See how Pinterest performs against its peers in TIKR (It’s free!) >>>

What the Model Says and What It Requires

TIKR’s valuation model points to a mid-case target of around $49, implying roughly 110% total return over the next four and a half years, or about 18% annualized.

The model assumes around 8% annual revenue growth and net income margins expanding toward 31%, with mild P/E compression across all scenarios.

The return is driven almost entirely by earnings growth rather than multiple expansion. The scenario range runs from around 7% annualized on the low end to around 15% on the high end, reflecting genuine uncertainty about how quickly international ARPU can move.

The honest context is that the five-year historical return on PINS has been deeply negative, down 68% over that period, which is why the market applies a skepticism discount even as the fundamentals improve.

TD Cowen has called Pinterest a best small-to-mid-cap idea for 2026, citing Performance+ adoption and improved ad measurement.

A broader group, including Goldman Sachs, JPMorgan, and Citi, has recently raised price targets. The street mean sits around $28, implying around 20% upside from current levels, which is more conservative than the TIKR model but still constructive.

Should You Invest in Pinterest?

Pinterest is one of the more interesting value cases in digital media right now. The platform is large, free cash flow is real, buybacks are meaningful, and monetization tools are improving.

The stock’s problem has always been execution pace, and the market has been burned by prior optimism that international ARPU would close the gap.

At $23, the model suggests the risk-reward has shifted toward the patient investor. Whether it actually pays off depends on whether the AI-powered ad improvements and international monetization push can sustain 15% or better revenue growth over the next several years.

See analysts’ growth forecasts and price targets for Pinterest stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!