Key Takeaways for Cloudflare Stock as of July 2026

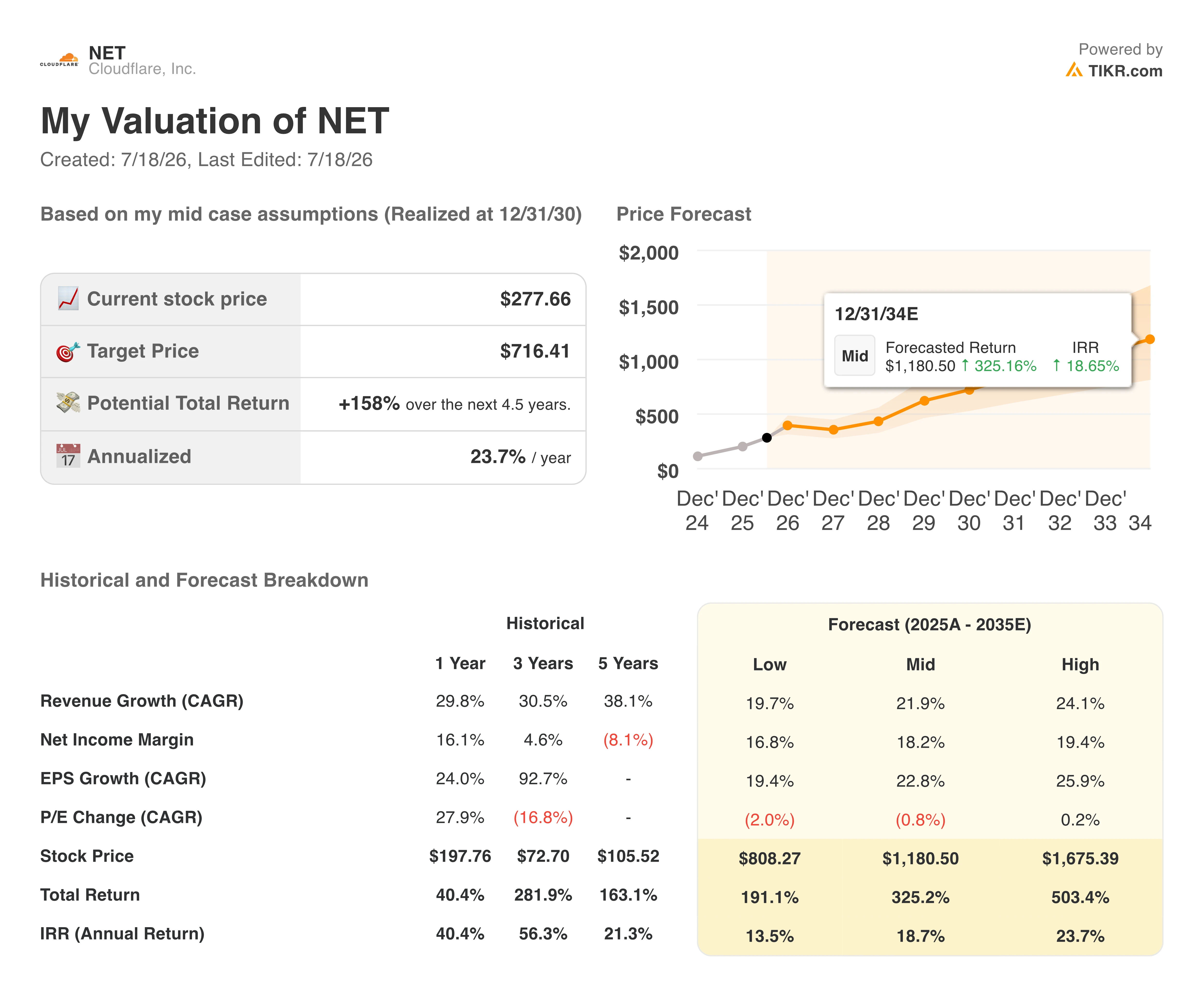

- TIKR’s valuation model implies 158% upside for Cloudflare stock, reaching $716.41 by December 2030 for a 24% annualized return.

- Wall Street carries 17 buys, 7 outperforms, 8 holds, 1 underperform and 1 sell on Cloudflare stock, with a $254.36 mean target that sits below the current price.

- On May 7, 2026, Cloudflare cut over 1,100 jobs, roughly 20% of its workforce, the same day it reported 34% revenue growth to $640 million.

- Full year operating income guidance held at $418 million to $421 million even after management booked $140 million to $150 million in restructuring charges.

Cloudflare Stock Cuts 20% of Staff Right After Its Strongest Quarter Yet

Cloudflare (NET) cut its workforce by more than 1,100 people, about 20% of its staff, on May 7, 2026, the same day it reported first quarter revenue of $639.8 million, up 34% year over year. The cuts landed across every function except quota carrying sales, and management framed the move not as cost cutting but as a rebuild of how the company operates.

CEO Matthew Prince addressed the timing directly on the Q1 call: “We’ve just seen that there are roles at Cloudflare that just aren’t the roles that we need for the future. I think just because you’re fit doesn’t mean you can’t get fitter.” He pointed to internal AI coding tool usage that jumped more than 600% in three months, with 97% of R&D staff now using AI coding tools and every production code change reviewed by autonomous agents before it ships.

The restructuring carries a real cost. Cloudflare booked $140 million to $150 million in severance and restructuring charges for full year 2026, about $40 million of it noncash and concentrated in the second quarter. CFO Thomas Seifert held free cash flow guidance unchanged despite that hit, with 25% to 30% of full year cash generation still expected in the second and third quarters. Operating income reached $73.1 million in the first quarter, up 31% year over year, and the full year outlook now calls for $418 million to $421 million.

That combination, a workforce cut announced from a position of accelerating growth rather than distress, is the detail the market hasn’t fully processed yet. Cloudflare is betting that AI-driven productivity lets it grow revenue 30% while shrinking its own cost base, and if operating income guidance holds despite $150 million in one-time charges, the margin math starts working in the company’s favor almost immediately.

NET Stock Trades Above Its Own Analyst Target After a 37% Drawdown

Cloudflare stock hit a maximum drawdown of 37% on February 23, 2026, erasing much of the run built through late 2025. Shares have since clawed back to sit just 1.45% below that peak, a recovery that predates the May restructuring news and suggests part of the operating shift was already priced in before Prince confirmed it.

Wall Street carries 17 buy ratings, 7 outperforms, 8 holds, 1 underperform and 1 sell on Cloudflare stock, with a mean price target of $254 as of July 17, 2026. That target sits below the current price of $277.66, meaning Cloudflare stock already trades roughly 8% above where the average analyst thinks it belongs.

The high estimate reaches $322, the low sits at $136, a gap wide enough to show the Street still disagrees sharply on how durable the AI-driven traffic story turns out to be.

TIKR Values Cloudflare Stock at $716, Pricing In a Structural Margin Shift

TIKR’s mid-case model values Cloudflare stock at $716.41 by December 2030, implying a 158% total return from the current price of $277.66, or 24% annualized over 4.5 years.

That annualized return sits well above what investors typically demand from a company already generating positive operating income, and it prices in Cloudflare’s shift from a subscription-heavy content delivery business into a compute and security platform built to monetize agent traffic directly.

The target is reachable because the restructuring math already shows up in guidance. Operating income is set to reach $418 million to $421 million for full year 2026 even after $150 million in severance charges, with management targeting operating margin above 30% and a Rule of 50 by 2027.

Cloudflare stock’s re-rating rests on the Street reading that headcount cut as sustained margin expansion rather than a one-time adjustment, and the early guidance numbers already support that read.

Should You Invest in Cloudflare, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cloudflare, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cloudflare, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NET stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!