Key Stats for Datadog:

- 52-week range: $98.01 – $278.71

- Current price: $258.63

- Street mean target: ~$254 (roughly in line with current price)

- Annualized IRR (TIKR mid case): ~21% / year

- Q1 2026 revenue: $834M (+32% YoY)

- Q1 2026 non-GAAP operating margin: 22%

- Q1 2026 non-GAAP EPS: $0.60 (vs. $0.46 prior year)

- Q1 2026 free cash flow: $289M (28% margin)

- Full-year 2026 revenue guidance: ~$4.16B

- Net revenue retention: above 120%

Value your favorite stocks like DDOG with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Up 96% This Year, With Three Separate 25% Drawdowns Along the Way

Datadog (DDOG) is a cloud monitoring and observability platform used by engineering teams to track the performance, security, and health of modern software applications.

The practical problem it solves is one that every company running software in the cloud faces: when something breaks across a complex system of microservices, containers, and third-party APIs, finding the source of the problem quickly is genuinely difficult.

Datadog gives engineering teams a unified view across their entire stack, pulling together metrics, logs, and traces into a single platform. As enterprises push more AI workloads into production, the complexity of monitoring those systems grows, and so does Datadog’s addressable opportunity.

The stock has gained 96% year-to-date, one of the strongest performances in software. But that number understates how volatile the journey has been.

The drawdowns chart shows three separate episodes this year in which the stock fell more than 20% from its recent peak, including a maximum drawdown of 27.45% on February 23. Each time, buyers stepped back in, and the stock recovered to new highs.

The pattern tells you something important about how the market is treating this name: conviction is high, but so is sensitivity to any sign that the growth story might be slowing. The Q1 results, reported in May, settled the debate for now.

Revenue came in above $1 billion for the first time in a single quarter, up 32% year over year, and the company raised its full-year guidance to around $4.16 billion. The stock surged more than 30% in the days following the report.

See historical and forward estimates for Datadog stock (It’s free!) >>>

A Revenue Trajectory Built on Every AI Dollar Spent in the Cloud

The core of the Datadog bull case is straightforward: every dollar enterprises spend on AI infrastructure creates downstream demand for observability. More GPU compute means more complexity to monitor, more agents to track, and more logs to analyze.

Datadog’s usage-based pricing model means its revenue naturally scales alongside customer cloud spending, without requiring a new contract negotiation every time a customer deploys a new workload.

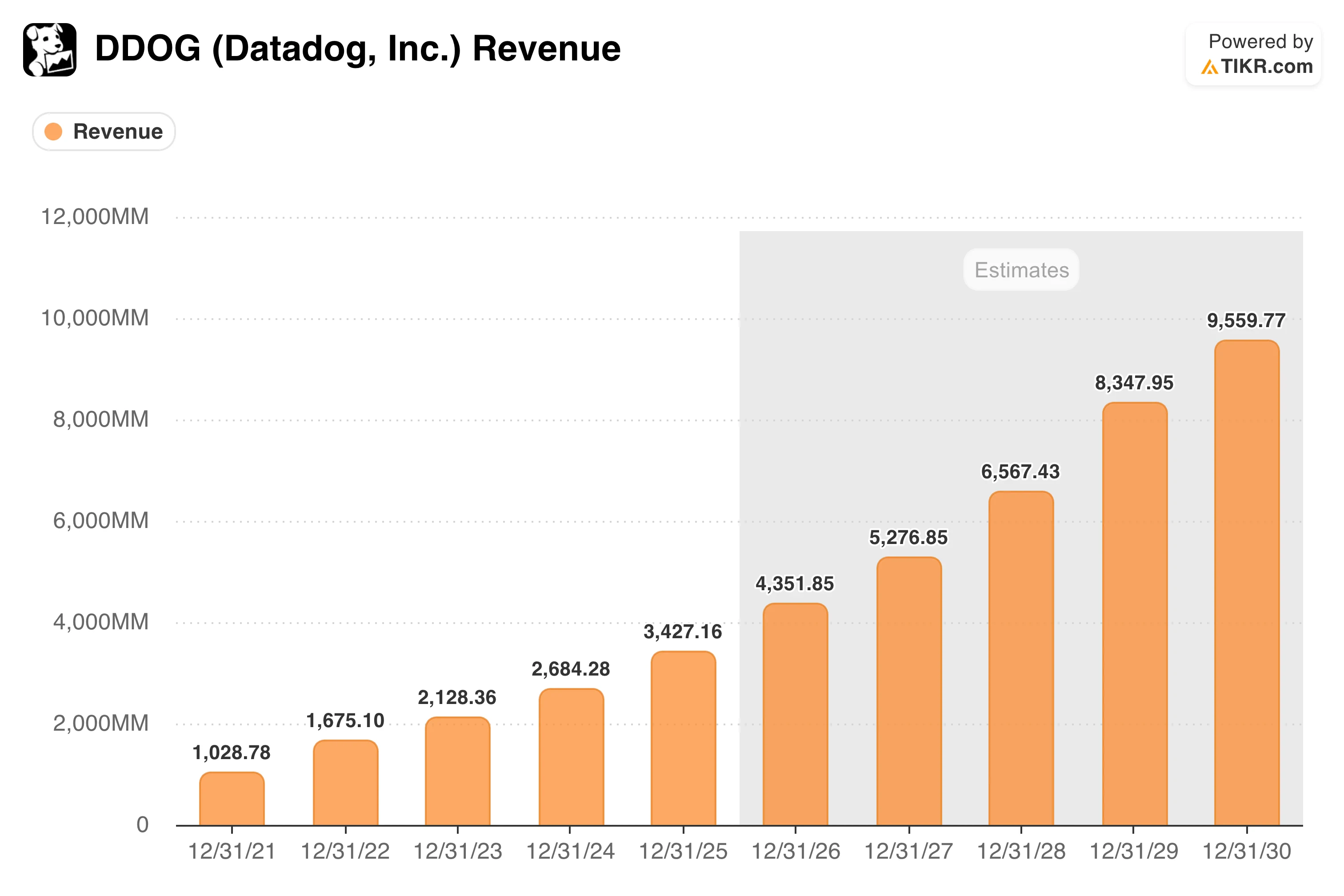

Revenue has grown from $1.03 billion in 2021 to $3.43 billion in 2025, with the acceleration remarkably consistent.

Consensus estimates project $4.35 billion in 2026, climbing to $5.28 billion in 2027 and nearly $9.6 billion by 2030. Net revenue retention above 120% means existing customers are spending meaningfully more each year, which is the engine under all of it.

The platform has expanded well beyond basic monitoring: Datadog now offers security, AI agent monitoring, and GPU observability products, and unveiled over 100 new features at its annual DASH 2026 conference.

It also secured FedRAMP High certification in May, opening the door to high-security U.S. federal workloads, a market that carries both scale and recurring contract value. The honest counterpoint is that non-AI demand has shown some softness, and as comparisons get tougher heading into 2027, sustaining 20%-plus growth becomes a higher bar to clear.

Truist recently upgraded to Buy with a $300 target, citing demand for AI observability, while some analysts have moved to Hold, arguing that the current price already reflects the best-case scenario.

See how Datadog performs against its peers in TIKR (It’s free!) >>>

What 106x Forward Earnings Is Actually Pricing In

At $258, Datadog trades at around 106x forward earnings and nearly 20x forward revenue. Those numbers sound extreme in isolation, but the context matters.

TIKR’s valuation model points to a mid-case target of around $620, implying roughly 137% total return over the next four and a half years, or about 21% annualized.

Unlike the Costco or UPS models, where returns are driven almost entirely by earnings growth with flat or compressing multiples, the Datadog model assumes a slight P/E expansion of around 2% annually in the mid case.

That assumption is worth examining carefully: it means the model is not just betting on continued earnings growth but also on the market maintaining or slightly increasing a premium multiple for this business. The scenario range runs from around 14% annualized on the low end to around 23% on the high end.

The low case, at $778 by 2034 on roughly 17% revenue growth and no multiple expansion, still represents a meaningful return from today’s price. What the model makes clear is that Datadog does not need everything to go right to generate strong returns. It needs execution to continue and the AI tailwind to remain durable.

Should You Invest in Datadog?

Datadog is one of the cleaner AI infrastructure stories available in public markets right now. The business model scales naturally with cloud spending, the platform keeps expanding, and the Q1 results showed growth actually accelerating rather than decelerating.

The honest tension is that at 106x forward earnings, the stock is priced for continued excellence, and any quarter that disappoints on growth will be punished quickly, as the drawdowns chart shows. The valuation model suggests the long-term return potential is genuinely compelling.

Whether the current multiple provides enough margin of safety is a judgment call that depends on how much conviction you have that the AI spending cycle will hold. TIKR gives you the tools to track every revenue data point and estimate revisions as the story develops.

See analysts’ growth forecasts and price targets for Datadog stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!