Key Stats for Datadog Stock

- 52-Week Range: $98 to $279

- Current Price: $269

- Street Mean Target: $225

- Street High Target: $320

- Analyst Consensus: 34 Buys, 10 Outperforms, 2 Holds, 1 Underperform, 1 Sell

- TIKR Model Target (Dec. 2030): $394

Datadog Stock Surges 42% on a Q1 Beat That Changed the Revenue Growth Narrative

Datadog (DDOG), the cloud-based observability and security platform, climbed 42% in a single week following Q1 2026 earnings that reset the ceiling on what investors should expect from this business.

Revenue for the quarter reached $1.006 billion, up 32% year over year, and came in well ahead of analyst estimates of $961.3 million.

That 32% growth rate was not a one-quarter anomaly; it marked the fourth consecutive quarter of revenue growth acceleration, stepping up from 29% last quarter and 25% in the year-ago quarter.

The beat on the bottom line was equally clean, with adjusted EPS of $0.60 versus consensus of $0.51 and adjusted operating income of $223 million against estimates of $203.79 million.

Datadog stock’s post-earnings reaction reflected a market that had substantially underestimated where this business was heading.

CEO Olivier Pomel, speaking at the J.P. Morgan Global TMC Conference, framed the demand signal precisely: “We saw acceleration across every single part of our business. We saw acceleration with the brand-new AI-native companies, whether they’re small or very big. We saw also acceleration with the rest of our business, which is even more interesting.”

The non-AI customer cohort, which represents the bulk of the revenue base, accelerated to mid-20s percent year-over-year growth, up from 23% last quarter and 19% in the year-ago quarter.

That acceleration in the core business, alongside the AI-native cohort’s expansion, prompted Datadog to raise full-year 2026 revenue guidance to between $4.3 billion and $4.34 billion, up from its prior range of $4.06 billion to $4.10 billion, a raise of roughly $240 million at the midpoint.

Q2 guidance came in at $1.07 billion to $1.08 billion, representing 29% to 31% growth, well above pre-print analyst expectations of $961.3 million.

The company ended Q1 with approximately 4,550 customers at $100,000 or more in annual recurring revenue, up 21% year over year.

Platform adoption continues to deepen: 56% of customers now use four or more products, 35% use six or more, and 20% use eight or more, all up meaningfully from a year ago.

Datadog also disclosed 7-figure and 8-figure annualized deals with the AI research divisions at two of the world’s largest technology companies, specifically for training workflow observability and GPU monitoring, a category the company had previously described as too early for a market.

Datadog also received FedRAMP High certification from the U.S. federal government during the quarter, opening Datadog to sensitive federal workloads it previously could not pursue.

44 Analysts Back DDOG with Buy Ratings and the Revenue Trajectory Justifies Every One of Them

The consensus coming out of Q1 is as unified as it gets for a company at this scale.

The analyst mean price target of $225 sits below where DDOG trades today at $269, a gap created by the stock’s post-earnings move outpacing the speed of target revisions.

In the sessions following earnings, analysts revised aggressively: JP Morgan raised to $320, Stifel to $305, D.A. Davidson to $250, CIBC to $250, BofA to $225, and RBC to $250, with targets stepping up sharply from the $160 to $170 range many held before the print.

The revenue trajectory makes the conviction legible.

For Q2 2026, consensus estimates revenue at approximately $1,078 million, representing around 30% growth year over year.

For the fiscal year, the revenue estimate sits at approximately $4.3 billion at the midpoint, with growth decelerating from Q1’s 32% pace but still running well above the company’s historical baseline.

The structural driver behind the conviction is not just AI-native demand but the acceleration in the non-AI base, which signals that cloud migration and platform consolidation are compounding on top of the AI tailwind.

Net revenue retention for the trailing 12 months came in at the low 120% range, ticking up from approximately 120% last quarter, and gross revenue retention held stable in the mid- to high 90s percent, confirming that the installed base is not just growing but expanding in spend.

Free cash flow was $289 million in Q1 with a free cash flow margin of 29%, and consensus estimates point to approximately $214 million in Q2 before recovering to approximately $382 million in Q4.

With 44 analysts holding buy-equivalent ratings and the company having delivered four straight quarters of revenue acceleration at over $1 billion in quarterly revenue, DDOG carries a premium price today but one the forward growth trajectory justifies: the stock is undervalued relative to the long-duration compounding case the data supports.

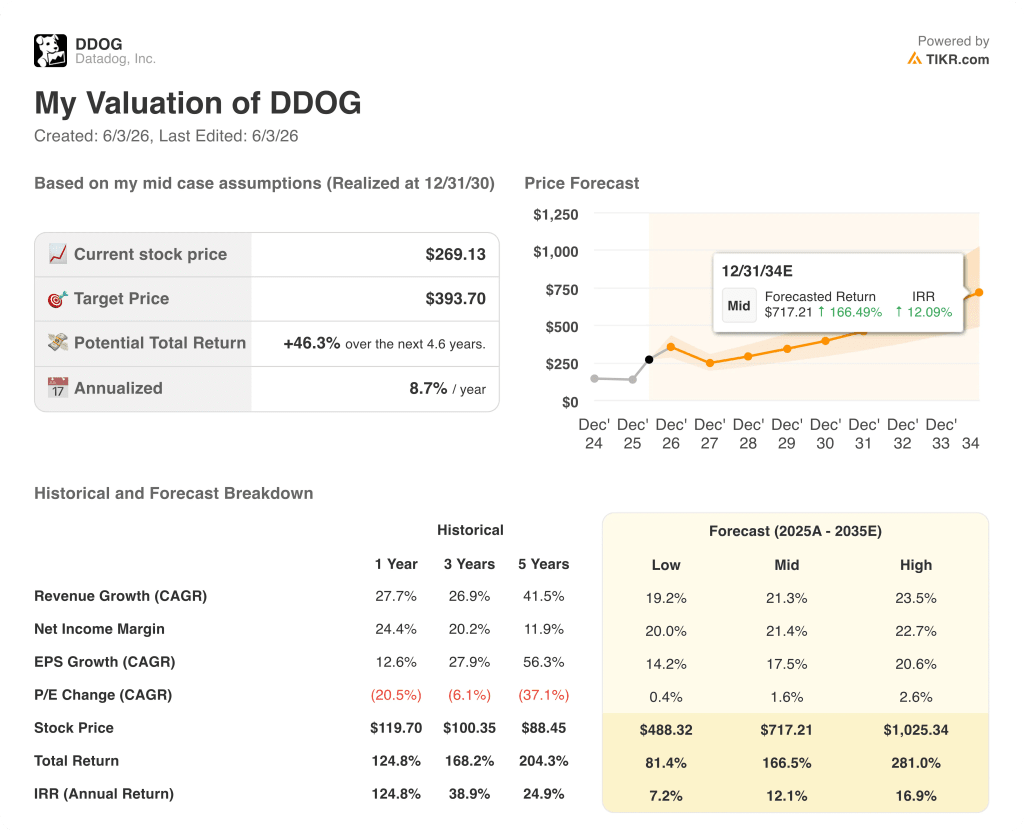

TIKR Puts DDOG at $394 by December 2030: The 46% Upside Case Rests on One Execution Question

TIKR’s base case values Datadog at approximately $394 by December 2030, implying around 46% total return from the current price of $269, or roughly 9% annualized over approximately 4 and a half years.

The model’s mid case assumes revenue growing at around 21% per year from 2025 through 2035, with a net income margin of approximately 21%, producing a stock price of approximately $717 by late 2034 with an IRR of around 12%.

The path to that outcome is already visible in Q1: Datadog holds roughly 14% of the ITOM observability market according to Gartner, and the CEO has cited that figure repeatedly as evidence of how early this company remains in its core addressable market, independent of any AI tailwind.

If the non-AI acceleration holds and AI-native demand continues to diversify from a handful of large model companies into the broader enterprise base, the low case (around 19% revenue CAGR) still produces a stock price of approximately $488 by late 2034 with an IRR of around 7%.

The high case, built on around 24% revenue CAGR and a net income margin of approximately 23%, prices DDOG at approximately $1,025, implying an IRR of around 17%.

The risk that breaks the mid case is not competitive displacement but a slowdown in the non-AI customer acceleration: if that cohort’s mid-20s growth rate proves a one or two-quarter event driven by deal timing rather than a durable inflection, estimates for 2027 and beyond would need to come down.

What do analysts say about Datadog stock?

The analyst consensus on DDOG is strongly bullish, with 34 Buys and 10 Outperforms among 47 covering analysts as of early June 2026.

The mean price target of $225 reflects where targets stood before the stock’s post-Q1 move to $269; many analysts have since raised targets into the $250 to $320 range. The Street high sits at $320.

Is Datadog stock a buy in 2026?

Datadog stock is backed by a Q1 print where revenue grew 32% year over year to $1.006 billion, the fourth consecutive quarter of acceleration, paired with a full-year guidance raise to approximately $4.3 billion at the midpoint.

TIKR’s mid-case model prices DDOG at around $394 by December 2030, implying roughly 46% total return from today’s price.

The key variable to watch is whether the non-AI customer cohort sustains its mid-20s growth rate through the second half of 2026.

Should You Invest in Datadog, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Datadog, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Datadog, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DDOG stock on TIKR for Free →