Key Stats for Bloom Energy Stock

- 52-Week Range: $18 to $323

- Current Price: $274

- Street Mean Target: $263

- Street High Target: $335

- Analyst Consensus: 9 Buys / 5 Outperforms / 11 Holds / 1 Underperform / 2 Sells

- TIKR Model Target (Dec. 2030): $842

Bloom Energy Stock Doubles Revenue in Q1 and Rewrites Its Own Growth Ceiling

Bloom Energy (BE), a San Jose-based manufacturer of solid oxide fuel cell systems, reported Q1 2026 revenue of $751.1 million on April 28, marking the first quarter of greater than 100% year-over-year growth in the company’s history as a public company.

Product revenue drove the result, reaching an all-time high of $653.3 million, up 208.4% year over year.

Bloom Energy stock had already more than doubled year-to-date heading into earnings, but the quarter’s scale forced a recalibration across the coverage universe.

At least six brokerages raised price targets the same day results dropped, and the company raised its full-year 2026 revenue guidance from a range of $3.1 billion to $3.3 billion to a new range of $3.4 billion to $3.8 billion.

The guidance raise was not incremental.

At the midpoint, the new range represents around 80% year-over-year revenue growth, up from a prior midpoint implying around 60%.

The catalyst behind the acceleration is structural, not cyclical.

Bloom is deploying fuel cell systems to power AI data center campuses entirely off the grid, replacing gas turbines, diesel backup generators, and battery arrays with what the company calls a “100% Bloom” solution.

On April 13, Bloom expanded its Oracle partnership to supply up to 2.8 gigawatts of fuel cell capacity, with 1.2 gigawatts already contracted and deployment underway.

Separately, on May 21, Bloom announced a deal to power Nebius’s AI infrastructure build-out, with a first project of 328 megawatts of installed capacity expected to be operational this year.

CEO K.R. Sridhar characterized the Oracle deal not as an isolated win but as a market inflection: “Where Oracle is going is where the broader market is headed.”

Sridhar went further on the competitive moat and said on Q1 2026 earnings call: “Their supply to current orders arrives only in 2029 or later, irrespective of the customers’ needs. Ours arrives this year or the next or whenever the customer is ready.”

The service business is also compounding, with service revenue of $61.9 million in Q1, up 15.6% year over year, and service margins reaching 18%, up 13 percentage points from Q1 last year.

Bloom ended Q1 with $2.52 billion in total cash.

BE Analyst Targets Are Rising but Still Trailing the Fundamental Shift Underway

The Q1 beat was not a close call.

Bloom Energy stock came into earnings with consensus revenue expectations of around $552 million; the company delivered $751.1 million, a beat of more than 36%.

Wall Street’s response was swift: Mizuho raised its target to $285 from $110, Morgan Stanley moved to $310 from $184, RBC jumped to $335 from $143, and BMO moved to $279 from $188, all in the days surrounding the print.

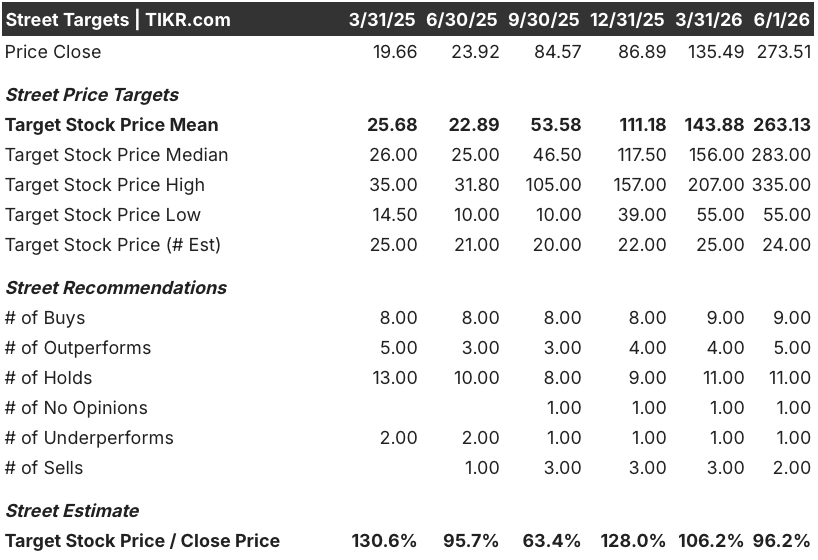

That flurry of upgrades still left the street’s mean target at around $263, below the current price of $274.

The consensus distribution reflects unresolved disagreement: 9 Buys, 5 Outperforms, 11 Holds, 1 Underperform, and 2 Sells, with 24 analysts covering the stock as of June 1.

The Holds and Sells are not a valuation argument, they are a credibility argument: whether revenue at this scale is durable or front-loaded into a narrow window of hyperscaler capex.

The data on the actuals and estimates table answers that question directly.

Consensus projects Q2 2026 revenue at around $820 million, up around 103% year over year, meaning the hyper-growth does not decelerate in the next reported quarter.

Revenue growth is then expected at around 79% for Q3 2026 and around 51% for Q4 2026, pointing to a full-year 2026 revenue figure at the midpoint of around $3.6 billion.

The forward trajectory into 2027 shows revenue estimated at around $1.15 billion in Q1 2027 and around $1.3 billion in Q2 2027, representing growth of around 53% and around 60% respectively.

EBITDA margins are projected to expand from around 19% in Q1 2026 to around 23% to 24% by late 2026 and early 2027, reflecting the operating leverage Bloom’s management flagged on the Q1 call.

JP Morgan, in its Q1 reaction, called the full-year guidance raise “not a typo” and highlighted “margin leverage as the business continues to scale.”

A company generating triple-digit revenue growth with a confirmed hyperscaler pipeline, durable service annuity revenue, and expanding margins on a platform its largest competitor cannot match for delivery speed — BE stock looks undervalued at current prices against the long-duration cash flow picture this trajectory implies.

Bloom Energy Is Outpacing Plug Power on Revenue by More Than 5 to 1 and the Gap Is Widening

Bloom Energy generated $750 million in revenue in Q1 2026, compared to $140 million for Plug Power (PLUG) in the same quarter, a gap of more than five times on the same core metric across two companies both positioned as clean on-site power solutions.

That gap is not narrowing on the forward estimates: consensus projects Bloom Energy revenue at around $1.17 billion in Q4 2026 while Plug Power is expected to reach around $280 million in the same quarter, keeping the ratio above 4 to 1 through year-end.

By Q2 2027, Bloom Energy’s estimated revenue of around $1.30 billion sits roughly six and a half times above Plug Power’s estimated around $200 million, meaning the absolute dollar distance between the two continues to expand even as both companies are expected to grow.

Is Bloom Energy Stock Undervalued in 2026? TIKR’s $842 Mid-Case Points Well Beyond Current Street Consensus

TIKR’s base case values Bloom Energy at approximately $842 by December 2030, implying around 208% total return from the current price of around $274, or roughly 28% annualized over 4 and a half years.

If Bloom executes on its mid-case assumptions, including around 25% revenue CAGR through 2035 and around 25% net income margins, the stock reaches around $1,009 by December 2034, delivering around 269% total return at around 16% IRR.

If execution falls short and the low case prevails, around 23% revenue CAGR and around 22% net income margins, the model produces a 2035 price of around $645 and a total return of around 136% at around 10% annualized.

If the AI infrastructure buildout accelerates beyond current projections and Bloom captures share faster than modeled, the high case implies around $1,528 by December 2035 and roughly 459% total return at around 22% IRR.

The mid-case IRR of around 16% annualized sits well above most equity hurdle rates, even after a 225% YTD move in BE stock, because the TIKR model’s revenue CAGR assumption of around 25% is conservative relative to the 130% actual growth Bloom just reported and the 80% full-year guidance midpoint currently in effect.

Is Bloom Energy stock a buy right now?

Bloom Energy stock posted Q1 revenue of $751.1 million, up 130.4% year over year, and raised its full-year 2026 revenue guidance midpoint to approximately 80% growth.

TIKR’s mid-case model targets approximately $842 by December 2030, implying around 208% total return from current levels.

The key variable is whether hyperscaler contract velocity continues to outpace grid alternatives.

What is the price target for BE stock?

The street mean target for BE stock stands at around $263, with the high target at $335, as of June 1, 2026. TIKR’s mid-case model projects approximately $842 by December 2030.

The spread between the street mean and the TIKR long-term target reflects disagreement not about Bloom’s current results, but about whether the AI power buildout is durable enough to sustain 25% revenue CAGR through the end of the decade.

Should You Invest in Bloom Energy Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Bloom Energy Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Bloom Energy Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BE stock on TIKR for Free →