Key Stats for Marvell Technologies Stock

- 52-Week Range: $61 to $225

- Current Price: $219

- Street Mean Target: $223

- Street High Target: $300

- Analyst Consensus: 31 Buys, 8 Outperforms, 5 Holds, 1 Underperform, 1 Sell

- TIKR Model Target (Jan. 2031): $490

Marvell Technology Stock Raised Its FY28 Revenue Forecast by $1.5 Billion in a Single Quarter

Marvell Technology (MRVL) posted record first-quarter FY2027 revenue of $2.42 billion following its May 27 earnings call, beating analyst estimates of $2.40 billion and growing 28% year over year.

CEO Matt Murphy guided Q2 revenue to approximately $2.70 billion, plus or minus 5%, ahead of the $2.60 billion analyst consensus at the time.

The company now expects FY2027 revenue to grow approximately 40% year over year to nearly $11.5 billion, up from earlier guidance of around 30% growth.

FY2028 guidance moved to approximately $16.5 billion, a $1.5 billion increase from the outlook provided just one quarter earlier.

Data center revenue reached $1.83 billion in Q1, representing 76% of total company revenue and growing 27% year over year.

Murphy even cited “exceptional AI-related bookings” as the primary driver, with custom silicon, optical interconnect, and Ethernet switching all contributing to the beat.

Marvell Technology stock has effectively become a proxy for the hyperscaler capital spending cycle, with the company holding active custom silicon engagements with all five major U.S. hyperscalers.

The interconnect business, which encompasses high-speed optical products for AI data center networking, is now expected to grow more than 70% in FY2027, up from a prior expectation of 50%.

Murphy stated on the Q1 2027 earnings call: “We have custom engagements across the board at all the U.S. hyperscalers.”

Marvell completed the acquisitions of Celestial AI and XConn during Q1, expanding its silicon photonics platform and scale-up networking capabilities.

The company also announced an expanded NVIDIA partnership anchored by three pillars: silicon photonics collaboration, NVLink Fusion integration for custom chip interoperability, and AI-RAN infrastructure combining 5G workloads with NVIDIA GPU compute.

Scale-out switch revenue is projected to exceed $600 million in FY2027, doubling from FY2026, with line of sight to more than $1 billion annualized in FY2028.

Custom silicon revenue is on track to grow more than 20% in FY2027 and is guided to more than double year over year in FY2028.

Murphy targets the custom business delivering over $10 billion in revenue by FY2029.

Why MRVL Analysts Raised Targets After Earnings but the Mean Still Underestimates the Ramp

The consensus conviction on Marvell Technology stock is unusually firm: 31 buy ratings and 8 outperform ratings from 41 analysts, against only 5 holds and 2 cautious views.

At least twelve brokerages raised their price targets following Q1 results, with individual targets spanning $200 at TD Cowen to $275 at Benchmark and Needham.

The street mean target of $223 implies only modest upside from the current price, which understates the scale of the revenue acceleration now locked into guidance.

Consensus estimates project Q2 FY2027 revenue at approximately $2.70 billion, representing around 35% year-over-year growth and accelerating from the 28% posted in Q1.

Quarterly revenue growth is then expected to run at least 10% sequentially through Q3 and Q4, with management targeting approximately $3 billion in quarterly run rate by Q3, one quarter ahead of the prior outlook.

Looking to FY2028, analysts project quarterly revenue reaching around $3.35 billion in Q1 and approximately $3.93 billion by Q3, reflecting year-over-year growth of approximately 51% and 46% in those periods.

J.P. Morgan noted after earnings that Marvell is being “very conservative” on FY2028 projections, citing firm plans for the next Tier-1 custom chip program ramping into high-volume manufacturing next fiscal year.

The key risk anchoring the cautious views is concentration: the custom silicon revenues remain tied to the cadence of a small number of hyperscaler programs, and competitive pressure from Broadcom and potential new entrants in the ASIC market adds execution risk.

With revenue tracking toward approximately $11.5 billion in FY2027, approximately $16.5 billion in FY2028, and the custom business alone targeting over $10 billion by FY2029, the revenue compounding implied by management guidance outpaces what a mean target of $223 prices in.

MRVL Revenue Growth Trails Broadcom Today but the Custom Silicon Gap Is Closing Fast

Broadcom (AVGO) remains the scale leader in custom AI silicon, with quarterly revenue of $22.12 billion in the quarter ended April 2026 against Marvell Technology’s $2.42 billion in the same period.

Meanwhile, Advanced Micro Devices (AMD) posted quarterly revenue of $9.92 billion for the same quarter, reflecting its GPU-driven data center acceleration but a fundamentally different product mix than Marvell’s interconnect and custom ASIC franchise.

On a forward basis, consensus estimates project Marvell Technology stock at approximately $2.70 billion in quarterly revenue for July 2026, growing around 34% year over year from $2.01 billion in July 2025.

AMD is projected at approximately $11.28 billion for the same quarter, while Broadcom is expected to reach approximately $28.47 billion, with each reflecting a more mature position in the current AI spending cycle.

The competitive implication for MRVL is structural: Broadcom built its custom silicon dominance over a decade of hyperscaler engagements, and Marvell is executing the same playbook now with all five U.S. hyperscalers actively engaged and a Tier-1 new program entering high-volume manufacturing in FY2028.

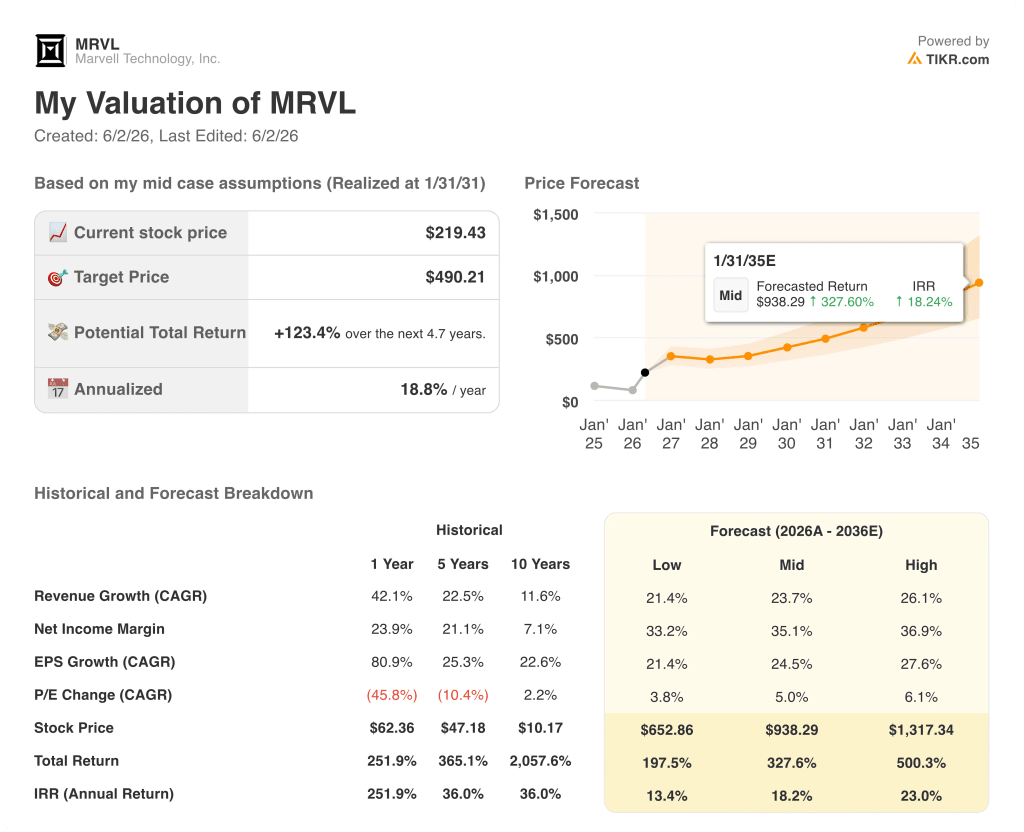

Is Marvell Technology Stock Undervalued in 2026? TIKR’s $490 Mid-Case Says the Ramp Has Years to Run

TIKR’s base case values Marvell Technology at approximately $490 by January 2031, implying around 123% total return from the current price of $219, or roughly 19% annualized over approximately 4.7 years.

If Marvell sustains a revenue CAGR of approximately 26% through fiscal 2036 while expanding net income margins toward approximately 37%, the TIKR high case points to a stock price of around $1,317 and an annualized return of approximately 23%.

If growth moderates to a revenue CAGR of approximately 21% with net income margins settling near 33%, the TIKR low case produces a stock price of around $653 and an IRR of approximately 13%.

The mid case assumes a revenue CAGR of around 24% and net income margins reaching approximately 35%, both conservative relative to the FY2027 and FY2028 guidance already on record.

At $219, Marvell Technology stock does not price in a scenario where the custom business reaches $10 billion by FY2029 and interconnect compounds above cloud CapEx growth for several more years.

Is Marvell Technology stock a buy right now?

Forty-one analysts rate MRVL, with 31 buys and 8 outperforms. The street mean target of $223 sits close to the current price, but TIKR’s mid-case model points to approximately $490 by January 2031, implying roughly 19% annualized returns.

The near-term valuation debate is real, but the multi-year revenue ramp from custom silicon and interconnect, with FY2028 guided to approximately $16.5 billion, gives long-term investors a substantive thesis.

What do analysts say about Marvell Technology stock?

Thirty-nine of forty-one analysts covering MRVL rate it buy or outperform, with a mean target of $223 and a high target of $300.

Following Q1 FY2027 results, at least twelve brokerages raised their price targets, with Benchmark and Needham reaching $275.

The primary bull thesis centers on custom silicon acceleration, interconnect dominance in AI data centers, and a new Tier-1 chip program ramping to high-volume production in FY2028.

Should You Invest in Marvell Technology, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Marvell Technology stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marvell Technology, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MRVL stock on TIKR for Free →