Key Stats for CAVA Stock

- 52-Week Range: $43 to $99

- Current Price: $75

- Street Mean Target: $92

- Street High Target: $110

- Analyst Consensus: 13 Buys / 3 Outperforms / 10 Holds / 1 Sell

- TIKR Model Target (Dec. 2030): $213

CAVA Stock Surges on 10% Same-Store Sales as Traffic Drives Every Dollar of It

CAVA Group (CAVA) delivered first-quarter fiscal 2026 results on May 19 that reset expectations for a restaurant chain operating in one of the most pressured consumer environments in years.

Revenue hit $438.27 million, a 32.1% increase year over year and a decisive beat against the $411 million consensus estimate.

Same-restaurant sales grew 9.7%, but the composition of that number is the signal: 6.8% came from guest traffic, not price.

In an industry where most chains are reporting flat-to-negative traffic and leaning on menu price hikes to manufacture comp growth, CAVA stock moved because the comp was earned a different way.

The company ended the quarter with 459 restaurants across 29 states and Washington, D.C., after opening 20 net new locations, with new restaurant productivity tracking above 100% of system averages.

Adjusted EBITDA reached $61.7 million, a 37.6% year-over-year increase, and operating cash flow came in at $64.1 million compared to $38.6 million in the same quarter last year.

CEO Brett Schulman addressed the question investors were asking directly on the Q1 2026 earnings call: “Guided by the same steady focus that has shaped our business for the past 15 years, we will continue building for the long term as we gain market share with significant white space ahead while deepening our relationships with guests through a value proposition that clearly resonates.”

CAVA raised its full-year 2026 guidance to same-restaurant sales growth of 4.5% to 6.5%, up from the prior range of 3% to 5%, and lifted its adjusted EBITDA outlook to $181 million to $191 million, against the previous guidance of $176 million to $184 million.

CFO Tricia Tolivar also confirmed on the call that second-quarter same-restaurant sales trends are “in line with the first quarter and tracking above our revised full year guidance.”

The chain launched its first-ever national seafood offering, Pomegranate-Glazed Salmon, at the start of Q2, which management expects to run through at least the fourth quarter.

Digital revenue mix rose to 39.9%, a 1.9 percentage-point gain year over year, and the company held its balance sheet at zero debt with approximately $403 million in cash and investments.

The COO role, filled by Douglas Thompson in recent months, is now focused on three priorities: people development, new restaurant opening excellence, and hospitality delivery across all shifts, reinforcing the operational consistency that underpins the unit economics.

Analysts Raise Targets After CAVA Earnings, but the Mean Still Sits Below Where the Model Points

The street’s response to the Q1 print was a broad-based target increase, with Stifel moving to $105, BofA raising to $108, Bernstein to $95, Jefferies to $95, and Piper Sandler to $92, alongside an upgrade from Argus to Buy.

The mean price target now sits at around $92 against a current price of $75, implying around 23% upside from where the stock trades today.

The bull case rests on revenue acceleration: the company delivered 32% year-over-year growth in Q1, and consensus estimates project around 29% growth for the quarter ending June 2026, before moderating to around 23% in the back half of the year.

EBITDA growth is the operating confirmation of that trajectory, with Q1 delivering 37.6% year-over-year improvement and forward estimates projecting around 26% growth for the June quarter.

The traffic quality is the variable bulls keep returning to: a 6.8% traffic-driven comp, in a macro environment where the CEO described consumers as “discerning,” suggests CAVA is gaining diners who are choosing it over alternatives, not returning because of a discount.

The bears and holds in the coverage universe center on valuation, with the stock commanding a premium multiple that requires sustained execution over multiple years to justify at current levels.

The structural argument is harder to dismiss: Tolivar confirmed new restaurant productivity is running above 100%, system AUVs have reached $3 million, and restaurants in the top AUV quartile are already generating restaurant-level margins above 30%.

The path to 1,000 restaurants by 2032, from 459 today, represents a doubling of the unit count with demonstrated economics already in place, and that is what keeps buy-side conviction ahead of the analyst median target.

With 13 buys, 3 outperforms, 10 holds, and 1 sell, CAVA stock looks undervalued relative to the revenue trajectory the operating data is building toward.

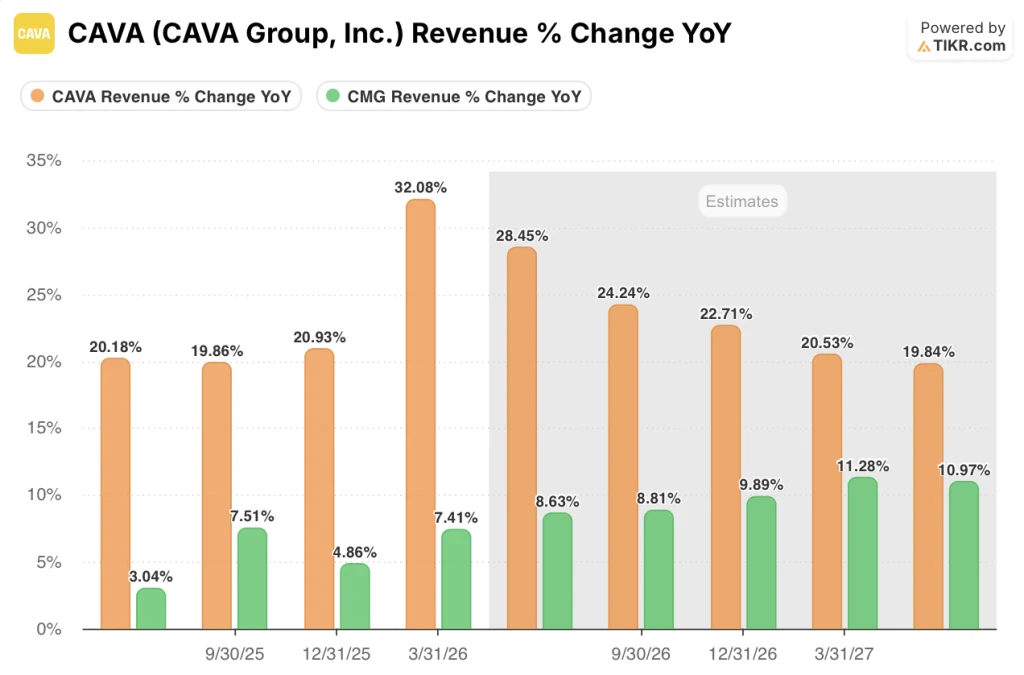

CAVA Revenue Growth Is Running 3x Chipotle’s Rate, and the Gap Persists Through 2027

CAVA’s 32.08% revenue growth in the quarter ended March 2026 ran against Chipotle’s 7.41% in the same period, a gap of nearly 25 percentage points between two fast-casual chains that investors routinely compare.

The spread is not a one-quarter anomaly: CAVA posted 19.86% and 20.93% growth in the two prior quarters while Chipotle delivered 3.04% and 4.86% respectively, meaning CAVA has grown revenue at roughly 4x Chipotle’s pace across the last three reported periods.

Consensus estimates show the gap narrowing but not closing: CAVA is projected to deliver around 28% growth for the June 2026 quarter against Chipotle’s estimated 9%, and even as CAVA moderates toward around 20% by mid-2027, it is still expected to grow revenue at roughly twice Chipotle’s estimated rate of around 11%.

For a stock trading at a premium multiple, the peer comparison reinforces rather than complicates the bull case: CAVA stock is not expensive relative to Chipotle because the market has mispriced it, it is expensive because the revenue engine behind it is running at a fundamentally different speed.

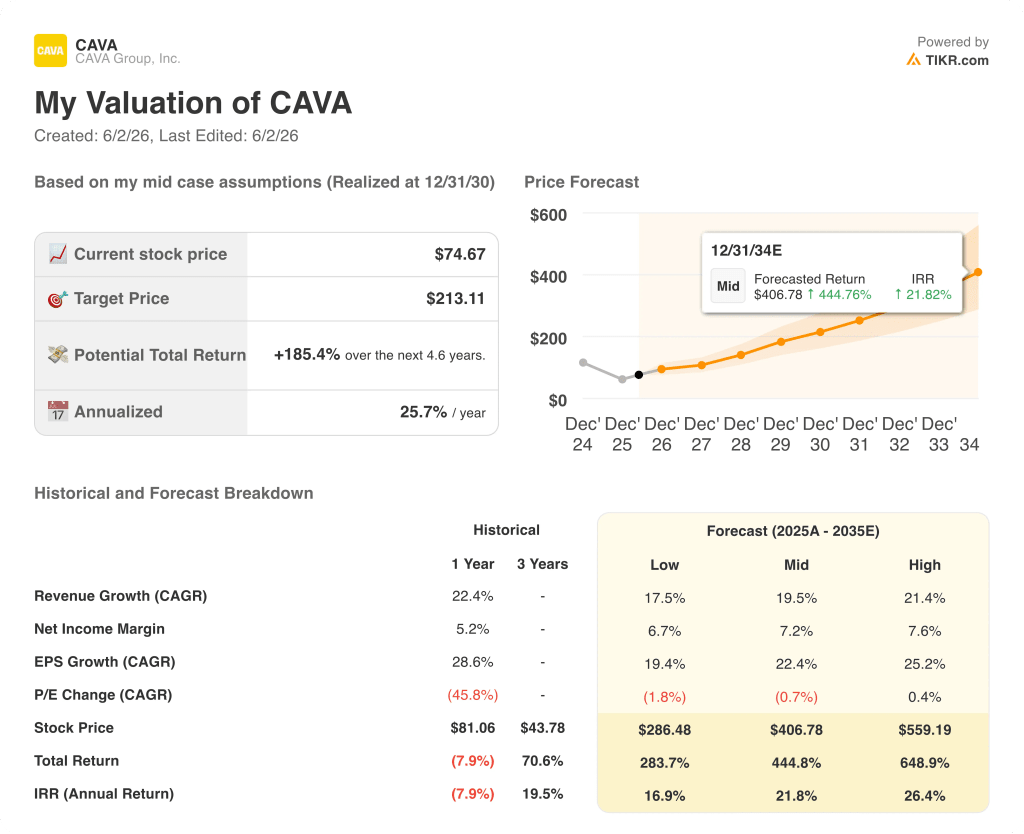

TIKR’s $213 Target on CAVA Stock: What the Model Needs to Hold

TIKR’s base case values CAVA Group at approximately $213 by December 2030, implying around 185% total return from the current price of $75, or roughly 26% annualized over approximately 4 and a half years.

The low case, anchored on roughly 17% revenue CAGR and around 7% net income margins, produces a stock price near $286 by 2034, delivering approximately 17% annualized returns.

The base case assumes around 20% revenue CAGR and net income margins approaching 7%, arriving at approximately $407 by late 2034 with roughly 22% annualized returns.

If unit economics hold at the top of the range and AUV growth continues compounding, the high case carries revenue growing at approximately 21% per year with net income margins near 8%, pointing toward a stock price near $559 and around 26% annualized returns.

All three scenarios rest on the same foundation: the unit growth runway is real, the company has publicly targeted at least 1,000 restaurants by 2032, new markets are opening with productivity above system averages, and Q1 cohort performance is tracking in line with or ahead of the 2025 class.

The risk the model watches is operational: whether CAVA can hold restaurant-level margins in the 23% to 24% range while absorbing the salmon launch headwind, rising energy costs, and continued wage investment in the AGM leadership program.

Is CAVA stock undervalued in 2026?

At a current price of $75 against a street mean target of approximately $92, and TIKR’s base case pointing toward approximately $213 by December 2030, CAVA stock looks undervalued for investors with a multi-year time horizon.

The Q1 traffic figure of 6.8% growth, at a time when most fast-casual peers are reporting flat-to-negative traffic, is the clearest data point that the brand’s value proposition is working at scale.

What do analysts say about CAVA stock?

The current consensus is 13 Buys, 3 Outperforms, 10 Holds, and 1 Sell, with a mean price target of around $92 against a current price of $75. Post-Q1, Stifel raised its target to $105, BofA moved to $108, and Bernstein lifted to $95.

The key variable for targets moving higher is whether Q2 same-store sales confirm the Q1 acceleration, which management has indicated is currently running above full-year guidance.

Should You Invest in CAVA Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CAVA Group, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CAVA Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CAVA stock on TIKR for Free →