Key Stats for ICON Public Limited Company Stock

- Current Price: ~$138 (June 1, 2026)

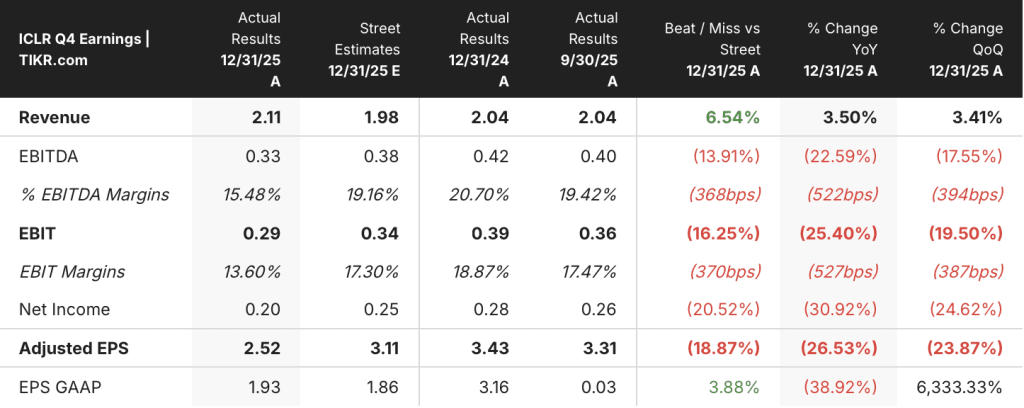

- Q4 2025 Revenue: $2.1B, +3.5% YoY (beat Street by 6.5%)

- Q4 2025 Adjusted EPS: $2.52, missed Street estimate of $3.11

- Q4 2025 Net Bookings: $2.9B, +19% YoY; Book-to-Bill 1.36x

- FY2025 Adjusted EPS: $12.53 vs. $13.37 in FY2024

- 2026 Revenue Guidance: $7.85B to $8.15B; Adjusted EPS $10 to $11

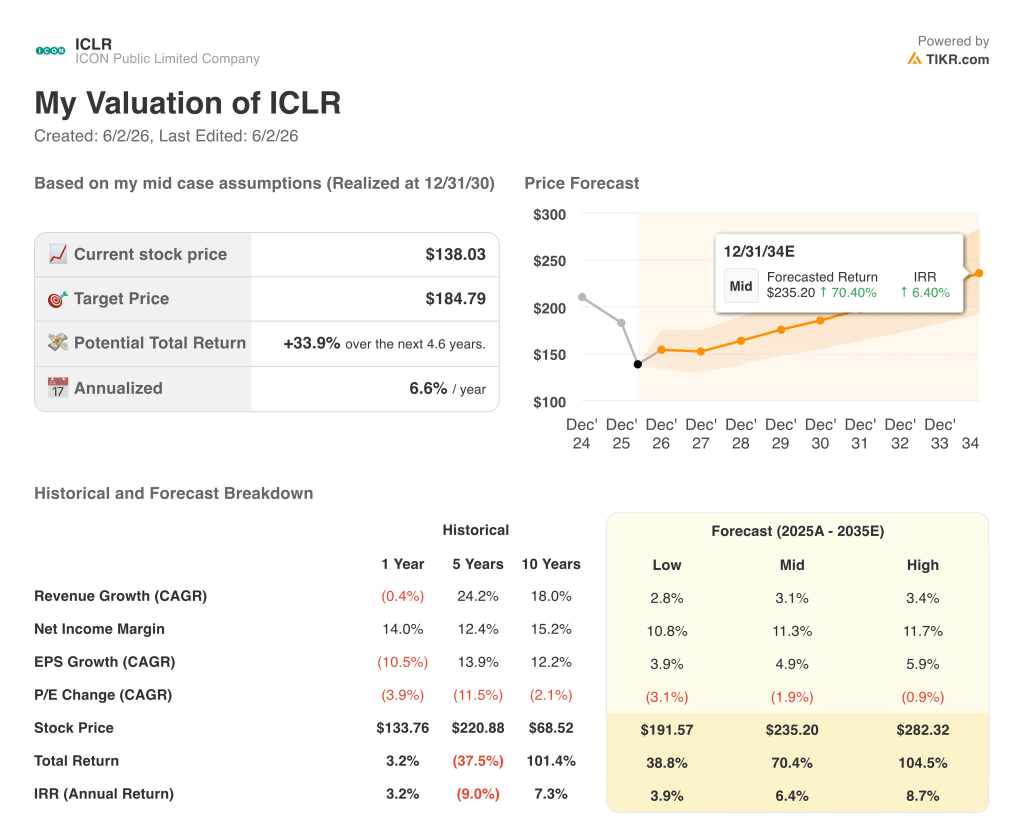

- TIKR Model Price Target (December, 2030): ~$185

- Implied Upside: ~34%

ICON Stock’s Accounting Investigation Closes as Bookings Hit a Turning Point

ICON Public Limited Company (ICLR) delivered Q4 2025 results on May 28 that simultaneously closed the most damaging chapter in the company’s recent history and revealed genuine commercial momentum that the market had been too distracted to fully price.

The news investors had been waiting on since October 2025 arrived first: the Audit Committee’s independent investigation concluded, identifying improper timing adjustments in clinical services revenue from Q3 2023 through Q4 2024, totaling an overstatement of $65 million in 2023 and $93 million in 2024.

Management was careful to frame the scope: the issues affected the timing of revenue recognition, not the quantum, and had no impact on reported cash flows or on customers.

Chief Executive Barry Balfe stated on the Q4 earnings call that “extensive measures have been taken to ensure the accuracy of our financial statements, and we are implementing a comprehensive remediation plan,” directly tying the remediation to four areas: organizational and personnel changes, revised revenue recognition policies, training, and enhanced controls over manual adjustments.

The investigation’s resolution removes the primary structural overhang for ICON stock, and the Q4 commercial performance underneath it signals the operational recovery is already in motion.

Net bookings reached $2.9 billion in the quarter, a 19% year-over-year increase, with a book-to-bill of 1.36x and meaningfully reduced cancellations of $365 million, down sharply from elevated levels in Q2 and Q3 2025.

Biotech win rates, a personal priority Balfe had flagged as underperforming on prior calls, posted a 5-point sequential improvement in Q4 and held into Q1 2026, driven by organizational changes including dedicated project management, medical affairs, and study start-up headcount for biotech customers.

Alongside the investigation resolution, ICON completed the divestiture of Symphony Health to HealthVerity, adjusted its backlog policy to reflect real-time cancellations rather than only formally papered terminations, and took a $3.9 billion backlog adjustment attributed primarily to awards from 2023 and earlier that were no longer expected to proceed.

ICON’s Income Statement Shows the Full Weight of the Margin Reset

Revenue across the eight quarters visible in the income statement shows a trough and partial recovery: after reaching $2.09B in Q1 2024, revenues dipped to $2.00B in Q1 2025 before recovering to $2.19B in Q4 2025, a 6.2% year-over-year increase in the most recent quarter.

The cost structure deterioration is more pronounced: cost of goods sold expanded from $1.43B in Q4 2024 to $1.69B in Q4 2025, compressing gross margin from 30.7% to 22.9% in a single year.

Operating income fell from $380M in Q4 2024 to $230M in Q4 2025, with operating margin contracting from 18.7% to 10.5%, reflecting the combined weight of the pass-through mix shift, the $50 million-plus cost-to-complete adjustment, and negative operating leverage on a sequentially stable top line.

Management guided explicitly for margin improvement through 2026 as the pass-through mix normalizes and commercial momentum rebuilds direct fee contribution, with the Q4 22.9% gross margin treated as a one-quarter trough rather than a new structural level.

Is ICON Stock Undervalued at the Current Price?

TIKR’s base case values ICON Public Limited Company at approximately $185 by December 2030, implying around 34% total return from the current price of $138, or roughly 7% annualized over the next 4 and a half years.

The TIKR model’s mid case embeds a P/E multiple compression assumption of approximately 1.9% annually through the forecast period, meaning the base case returns are driven by earnings growth alone, with the market expected to assign a lower multiple over time rather than re-rate the stock higher.

If 2026 bookings momentum holds and direct fee revenue recovers as projected, the TIKR low case points to a stock price of approximately $192, implying roughly 39% total return or around 4% annualized: a scenario where near-term margin pressure persists but commercial traction does not deteriorate further.

If biotech win rates sustain above Q4 levels, direct fee mix improves faster than the guidance midpoint assumes, and management executes on cost efficiency targets through 2026, the TIKR high case projects approximately $282, implying around 105% total return or roughly 9% annualized: a scenario contingent on both earnings recovery and some degree of multiple stabilization.=

How did ICON plc perform in Q4 2025 earnings?

ICON reported Q4 2025 adjusted EPS of $2.52, missing the Street estimate of $3.11, driven by a $50 million-plus cost-to-complete adjustment tied to the company’s accounting investigation cleanup.

Revenue of $2.1 billion beat the $1.98 billion consensus by 6.5%, primarily on pass-through revenues that exceeded expectations by more than $150 million.

Net bookings of $2.9 billion rose 19% year-over-year with a 1.36x book-to-bill, the strongest commercial performance indicator the quarter produced.

Management guided 2026 adjusted EPS to $10 to $11, with margin improvement expected to build sequentially through the year.

Should You Invest in ICON Public Limited Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ICON Public Limited Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ICON Public Limited Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ICLR stock on TIKR for Free →