Key Stats for Astera Labs Stock

- 52-Week Range: $85 to $356

- Current Price: $356

- Street Mean Target: $245

- Street High Target: $297

- Analyst Consensus: 11 Buys, 7 Outperforms, 8 Holds

- TIKR Model Target (Dec. 2030): $828

Astera Labs Stock Rallies 320% Off Its Lows as Scorpio X Ramp Begins in Earnest

Astera Labs (ALAB), the semiconductor connectivity company powering the backbone of AI data centers, delivered fiscal Q1 2026 revenue of $308.4 million, up 93% year-over-year and 14% sequentially, beating consensus estimates of around $292 million.

The quarter was not built on one product or one customer.

Revenue growth was broad-based across the company’s signal conditioning, Ethernet AEC, memory controller, and fabric switch portfolios, with PCIe Gen 6 products crossing the one-third-of-total-revenue threshold for the first time.

The headline catalyst was the Scorpio X-Series: Astera’s scale-up AI fabric switches moved from preproduction into initial volume shipments during the quarter, with the flagship 320-lane configuration beginning to ship and full-volume production targeted for the second half of 2026.

CEO Jitendra Mohan framed the moment plainly on the Q1 2026 earnings call: “We expect strong revenue growth to continue through 2026 and into 2027, driven by the proliferation of AI fabrics and the industry’s transition to PCIe 6, 800 gig and 1.6T Ethernet connectivity.”

Beyond the switch ramp, the company won a second custom design using a modified version of its Leo CXL memory controller for a KV Cache offload application at a major hyperscaler, adding to the NVLink Fusion custom silicon program already in development with NVIDIA.

Astera Labs stock surged more than 17% on May 20 alone as chip stocks broadly rallied ahead of Nvidia’s earnings, a day when the Philadelphia Semiconductor Index jumped 4.5%.

Northland Capital downgraded ALAB to Market Perform from Outperform citing valuation, becoming the only significant downgrade following the quarter.

At Computex in June, the company hosted live demos of the Scorpio X-Series 320-lane switch, the first public showing of the device outside of a controlled customer environment.

The fiscal Q2 guidance targets revenue of $355 million to $365 million, representing sequential growth of around 15% to 18% at the midpoint of approximately $360 million.

ALAB Analyst Consensus: Why the $245 Mean Target Does Not Tell the Whole Story

The street mean target of around $245 sits roughly 31% below the current price of $356, a gap that looks bearish on first glance but reflects the timing problem of a consensus that was built before the Scorpio X ramp began in earnest.

As of early May, immediately after Q1 results, the highest active buy-side targets were clustering in the $260 to $297 range, with JPMorgan at around $280, Jefferies at around $270, and RBC at around $270, all raised post-earnings.

The hold-rated Barclays target sat at around $200, a figure set before the Scorpio X initial volume announcement and the Computex demo confirmation, illustrating how the distribution of targets reflects staggered update cycles rather than a unified view of the forward business.

The fundamental case for bulls rests on revenue trajectory: consensus estimates project revenue of around $360 million in Q2 2026, around $410 million in Q3, and around $470 million in Q4, implying roughly 87%, 78%, and 73% year-over-year growth rates respectively across the next three quarters.

Normalized EPS is also expected to accelerate through the same period, with the street projecting around $0.69 for Q2, around $0.79 for Q3, and around $0.91 for Q4, off the Q1 actual of $0.61.

The near-term risk the bulls are managing is gross margin compression: management guided Q2 non-GAAP gross margin of approximately 73%, down from 76.4% in Q1, with around 200 basis points of the decline attributed to a noncash warrant agreement with a key customer.

With 26 analysts covering ALAB and zero sell ratings, the distribution tells you one thing clearly: no one on the street thinks the story is over, and ALAB stock looks undervalued relative to its earnings trajectory even after the run.

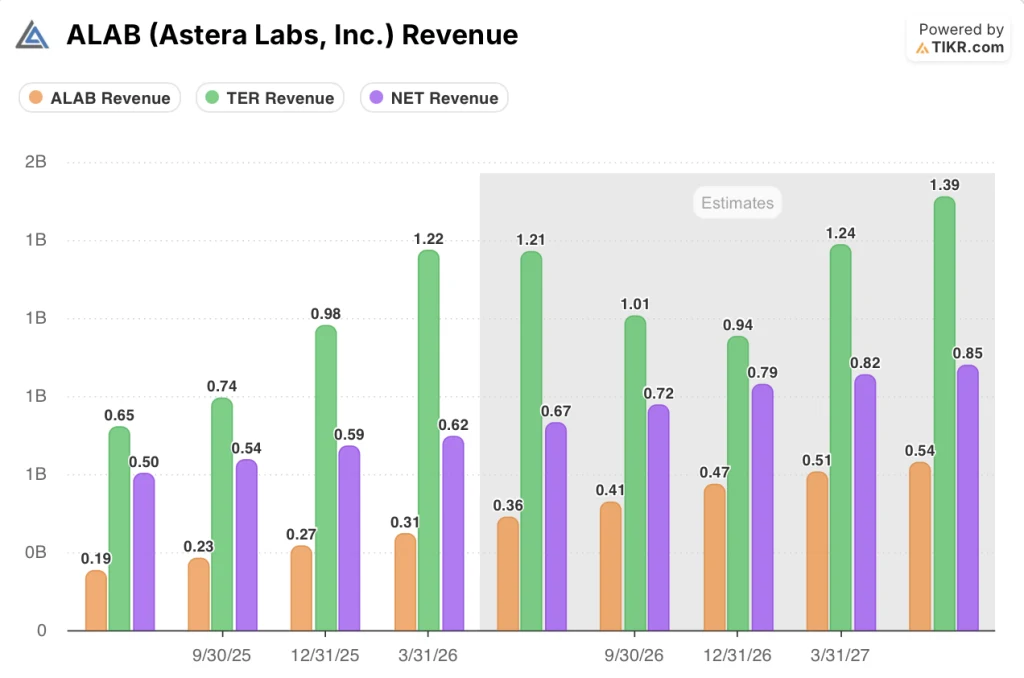

ALAB Revenue Is Smaller Than Both Peers Today — and Growing Faster Than Either

Astera Labs generates less quarterly revenue than both Teradyne (TER) and Cloudflare (NET) at the current snapshot, but the forward trajectory separates it sharply from either peer.

Teradyne posted quarterly revenue of $1.22 billion in Q1 2026 versus Astera Labs’ $0.31 billion, a near 4x gap, but consensus estimates project TER revenue declining to approximately $1.01 billion in Q3 2026 before recovering, with no quarter through mid-2027 meaningfully exceeding the Q1 peak.

Cloudflare is tracking a steadier upward path, with estimated quarterly revenue climbing from around $0.67 billion in Q2 2026 to approximately $0.85 billion by Q2 2027, roughly 27% growth over four quarters.

Astera Labs is projected to cover almost the same ground in absolute dollar terms, growing from around $0.36 billion in Q2 2026 to approximately $0.54 billion by Q2 2027, representing roughly 50% revenue growth over the same four quarters off a smaller base.

The comparison makes the structural case for ALAB stock without needing a valuation argument: it is the only one of the three with accelerating sequential revenue, no near-term cyclical decline in the estimate stack, and a product portfolio that has not yet begun shipping optical or custom silicon revenue.

TIKR Model on ALAB: Around $828 by 2030, With a Roadmap That Has Not Fully Priced In

TIKR’s base case values Astera Labs at approximately $828 by December 2030, implying around 133% total return from the current price of $356, or roughly 20% annualized over approximately 4 and a half years.

The mid-case scenario assumes a revenue growth CAGR of around 26% from 2025 to 2035, a net income margin of around 35%, and EPS growth of around 24% annually, producing a stock price of approximately $1,299 by December 2034 on the 10-year horizon, with an IRR of roughly 16%.

If execution slows — Scorpio X ramp delays, hyperscaler capex deceleration, or optical programs pushed past 2027 — the low case assumes around 24% revenue CAGR and net income margins near 33%, producing a stock price of approximately $881 by December 2034 and an annualized return of around 11%.

If the roadmap accelerates and custom silicon programs, UALink switches, and optical engines layer in ahead of schedule, the high case assumes revenue CAGR of roughly 29% and net income margins near 37%, producing a stock price of approximately $1,859 by December 2034 and an annualized return of around 21%.

The verdict: at $356, ALAB stock is undervalued against the mid-case TIKR model, with a five-product ramp that is still in its early phases, an optical revenue line that has not yet contributed, and two custom silicon programs that do not begin shipping until 2027.

Is Astera Labs Stock a Buy Right Now?

ALAB’s product roadmap is ahead of the consensus timeline in one critical respect: Scorpio X began shipping initial production volumes in Q1 rather than being a pure second-half event.

With zero sell ratings from 26 analysts, a TIKR mid-case target of roughly $828 by 2030, and EPS expected to grow from $0.61 in Q1 to approximately $0.91 by Q4 of this year, the fundamental case for ALAB stock is intact. The key variable is Scorpio X volume production in the second half of 2026.

Should You Invest in Astera Labs, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Astera Labs, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Astera Labs, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ALAB stock on TIKR for Free →