Key Stats for Astera Labs:

- 52-week range: $97.89 – $499.48

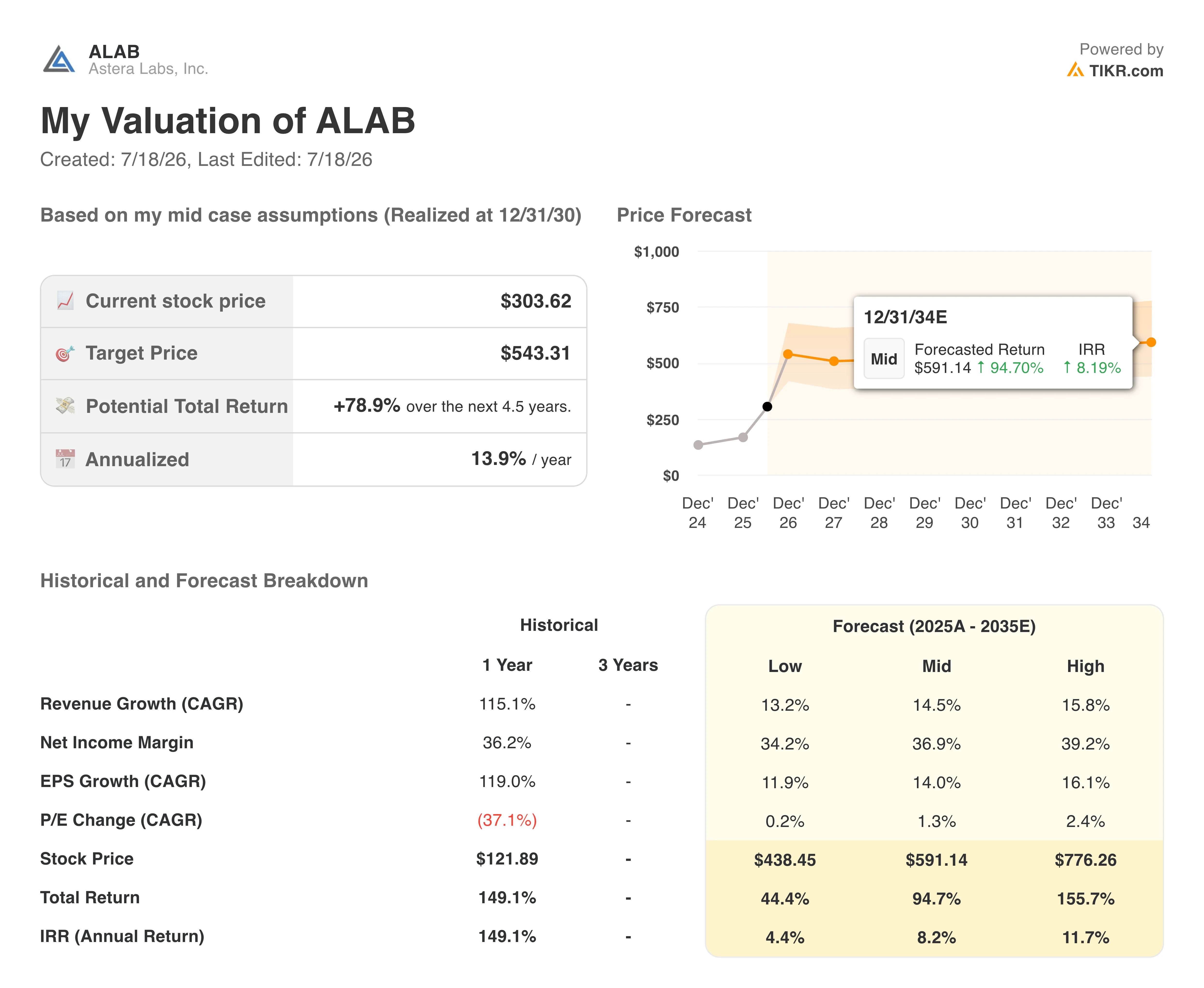

- Current price: $303.62

- Street mean target: ~$291

- Annualized IRR (TIKR mid case): ~14% / year

- Q1 2026 revenue: $308.4M (+93% YoY)

- Q1 2026 non-GAAP operating margin: ~43%

- Q1 2026 non-GAAP EPS: $0.47 (vs. $0.20 prior year)

- Q2 2026 revenue guidance: $355M – $365M

- LTM gross margin: 76%

- Market cap: $52B

Value your favorite stocks like ALAB with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

From $499 to $303: A 37% Drawdown on a Business Growing at 93%

Astera Labs (ALAB) is a fabless semiconductor company, meaning it designs chips but outsources manufacturing, focused entirely on the connectivity layer inside AI data centers.

When hyperscalers like Microsoft, Google, and Amazon build clusters of thousands of GPUs to train or run AI models, those GPUs need to communicate with each other and with memory at enormous speeds. Astera’s products handle that job.

Its Aries PCIe retimers extend signal reach across server backplanes, its Scorpio switches create the high-speed fabric that ties GPU clusters together, and its Taurus Ethernet modules handle scale-out connectivity between racks.

The company estimates its technology is embedded in roughly 90% of the world’s AI compute servers, making it one of the cleaner picks-and-shovels plays in the AI infrastructure buildout.

The stock peaked near $499 in late 2025, rode a massive wave of AI infrastructure spending, then sold off sharply twice this year. The max drawdown of 46.57% was hit on March 30, and the stock has since partially recovered before pulling back again to the current -37% from the peak.

The business did not cause either selloff. Q1 2026 revenue came in at $308.4 million, up 93% year over year and 14% sequentially, driven by strong demand for its PCIe 6 portfolio.

CEO Jitendra Mohan called it a record quarter and pointed to expanding design wins with hyperscalers and the initial shipments of the new Scorpio X-Series 320-lane AI fabric switch. Q2 guidance of $355 million to $365 million implies another 15% to 18% sequential step-up.

The selloffs were driven by broader market volatility and valuation anxiety, not execution. The question is whether the current price represents a genuine opportunity or just a less extreme version of the same premium.

See historical and forward estimates for Astera Labs stock (It’s free!) >>>

A Valuation That Has Already Compressed Significantly, and Still Isn’t Cheap

Understanding where ALAB’s multiple sits today requires more than citing a single number.

The NTM EV/Revenue chart covers the stock’s entire public history since the March 2024 IPO. The multiple launched near 50x, compressed all the way to 11x by late 2024 as early post-IPO enthusiasm faded, re-rated toward 47x at the October 2025 peak, then compressed again to around 11-12x in early 2026 before re-expanding sharply through April and May.

Today it sits at 28.93x, modestly above the long-term mean of 25.17x. The takeaway is nuanced: the stock is down 37% from its high, but the multiple is not obviously cheap by its own history.

What has changed is that revenue estimates have risen significantly alongside the stock’s recovery, meaning the compression in the multiple reflects genuine earnings growth, not just a price decline.

Competitors, including Marvell Technology and Credo Technology, are chasing the same hyperscaler relationships, which adds a layer of execution risk that the multiple should probably reflect.

See how Astera Labs performs against its peers in TIKR (It’s free!) >>>

What the Model Says, and What It Requires You to Believe

TIKR’s valuation model points to a mid-case target of around $543, implying roughly 79% total return over the next four and a half years, or about 14% annualized.

Being honest about what that requires: the model assumes revenue growth decelerates from 93% today to around 14-15% annually through 2030 and beyond.

If that deceleration happens faster than expected, perhaps because hyperscaler spending cycles are lumpy or a competitor wins key sockets in the next PCIe generation, the low-case scenario implies only around 4% annualized returns.

The high case at around 12% IRR requires everything to go right for a long time. The wide range of scenarios is appropriate for a company this young with this much concentration on a handful of large customers.

What works in ALAB’s favor is the margin structure: 76% gross margins and 43% non-GAAP operating margins are exceptional for a semiconductor business and suggest that, if growth sustains, earnings leverage will be significant.

The Scorpio X-Series, targeting a merchant-switch silicon market projected to reach $20 billion by 2030, gives the company a credible path to sustain hypergrowth beyond its current PCIe retimer base.

Should You Invest in Astera Labs?

Astera Labs is a genuinely compelling AI infrastructure business with exceptional margins, strong customer relationships, and a product roadmap that continues to expand the addressable market.

The stock’s 37% drawdown from its high has made it more interesting than it was at $499, but the current multiple still demands continued execution at a high level.

The model’s mid-case of around 14% annualized is a reasonable base case, not a layup, and the low case reminds investors that valuation risk is real at 90x forward earnings.

See analysts’ growth forecasts and price targets for Astera Labs stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!