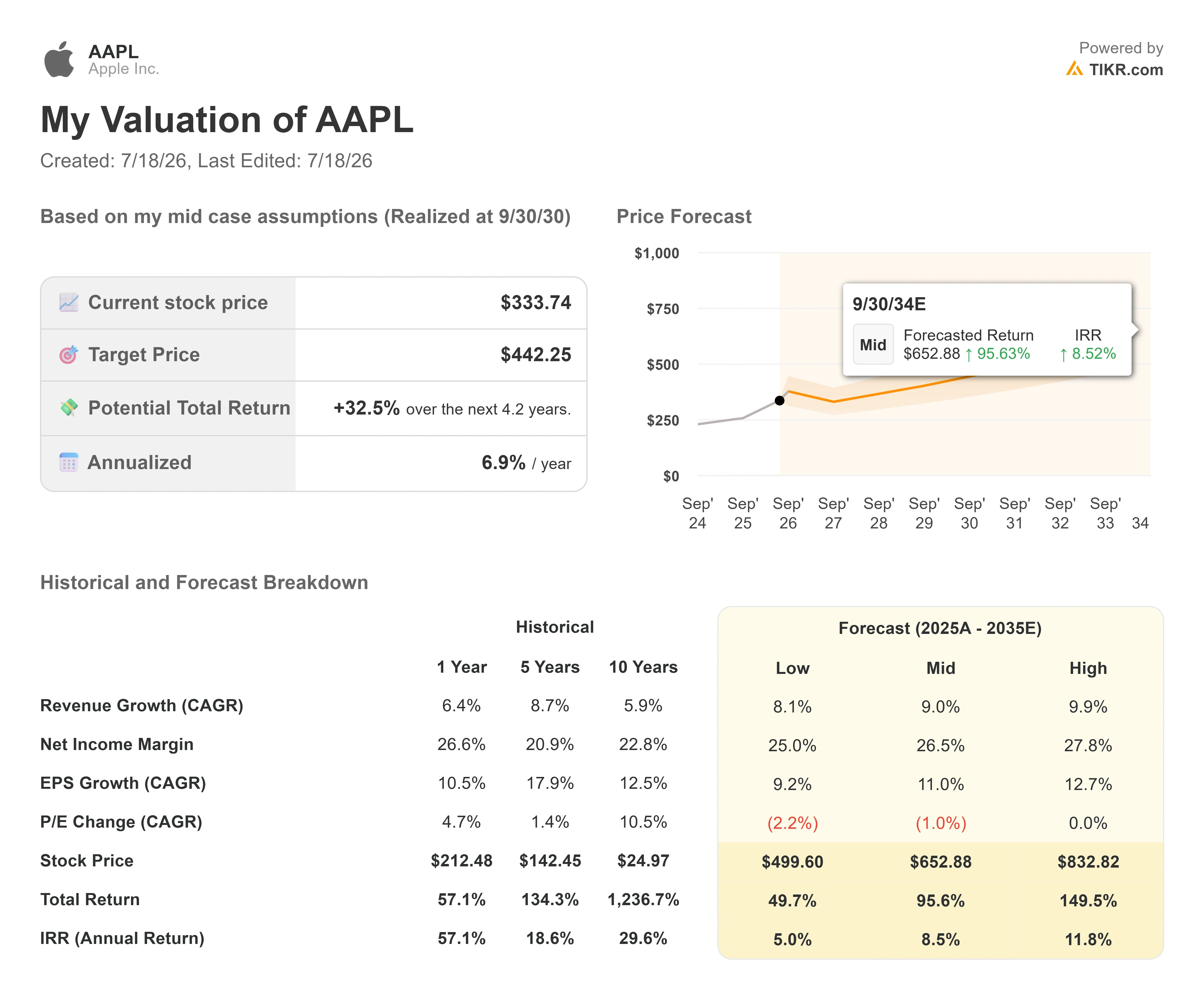

Key Stats for Apple Stock

- Current Price: $333.74

- Target Price (Mid): ~$442

- Street Target: ~$318

- Potential Total Return: ~33%

- Annualized IRR: ~7% / year

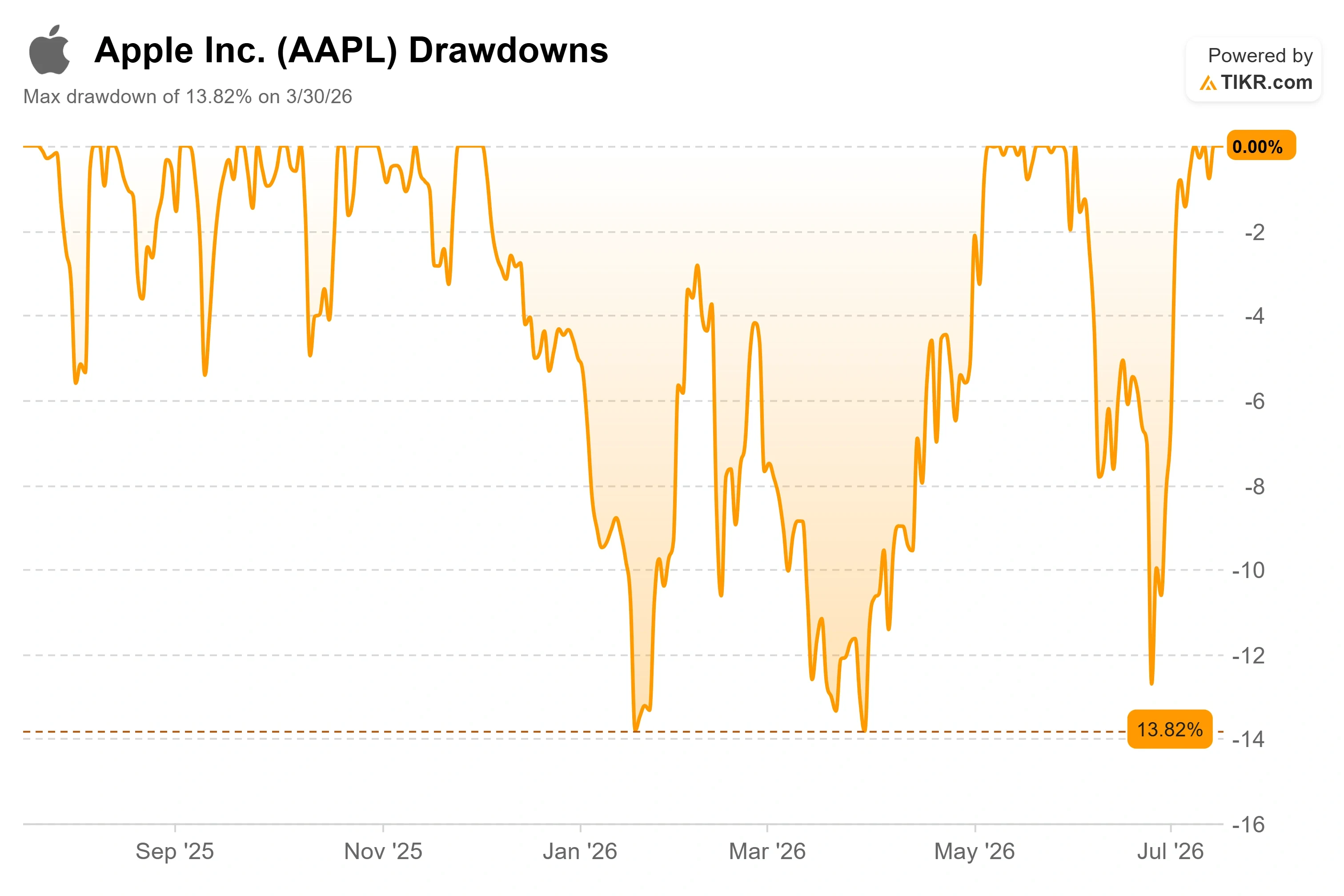

- Max Drawdown: 13.82% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Apple (AAPL) spent most of the last year being the AI trade’s punchline, the one megacap that supposedly missed the boat. On July 17, for part of a single session, it was worth more than any company on Earth. Apple’s market value edged above Nvidia’s intraday, roughly $4.88 trillion against $4.86 trillion, before Nvidia clawed the crown back and closed narrowly ahead. The lead lasted minutes, not a day. The symbolism landed anyway. It was the first time in more than a year Apple had touched the top spot, and it happened not because Apple out-innovated anyone on AI, but because investors started fleeing the companies that spend the most on it.

That is the strange logic driving the stock right now. Money is rotating out of the capital-hungry end of the AI market and into the one giant that refuses to play that game. The question underneath the milestone is harder than the headline: if the reason Apple is winning is that it spends almost nothing on AI infrastructure, how long can a hardware company ride a software revolution it outsourced?

The Rally That Was Built on Everyone Else’s Fear

Apple has climbed roughly 20% since bottoming at $275.15 on June 25, adding close to $600 billion in market value and printing a fresh record high. The catalyst was not a product. It was a mood shift. Investors spent early summer growing uneasy about the sums being poured into AI data centers with no clear timeline for a return, and Apple suddenly looked like the safe harbor.

The math behind that reframing is stark. HSBC noted that Apple invests only about 2.5% of estimated 2026 sales in capital expenditures, against roughly 39% for the hyperscalers building out AI compute. Apple gets its AI exposure by paying Google for access to Gemini, which now underpins the revamped Siri that shipped in the iOS 27 public beta. No fabs, no server farms, no multi-year depreciation drag. For a market that has started to punish spending, that asset-light posture flipped from weakness to strength almost overnight.

The move got a formal endorsement on July 17. HSBC analyst Nicolas Cote-Colisson upgraded Apple to Buy from Hold and lifted his price target to $366 from $260, a 41% increase in the target itself, calling the company “an operational turning point” that is “well placed to leverage its 2.5 billion installed device base with its forthcoming revamped Apple Intelligence.” That base matters because it is the distribution engine: Apple does not need to win the model race if it can staple someone else’s model to a billion and a half devices people already own.

See historical and forward estimates for Apple stock (It’s free!) >>>

Why the Crown Sits on Top of a Disagreement

Here is the part the milestone headline hides. At $333.74, Apple trades above where the average analyst thinks it should be. The Street’s mean target sits around $318, which puts the stock roughly 5% over consensus fair value, and the Street’s own target-to-price ratio as of July 17 sat at 95%, meaning the crowd sees modest downside, not upside, from here. HSBC’s $366 is an outlier above the pack, not the pack itself. Earlier that week, KeyBanc went the other direction and cut the stock to underweight on demand and valuation concerns.

So the record high is not a consensus victory lap. It is a momentum trade running ahead of the analysts who cover the name most closely. The stock now carries a trailing price-to-earnings ratio around 40x, a rich multiple for a company the model expects to grow revenue at high single digits. Options desks have noticed: put buying has climbed to unusually elevated levels even as the shares rise, a sign not everyone trusts the move.

That tension is the whole story into the July 30 print. Bulls are betting the AI rotation and the fall product cycle keep the bid alive. The skeptics are looking at a 40x multiple, a consensus target below the price, and an earnings print that could reset the narrative in either direction. Neither side is obviously wrong yet.

See how Apple performs against its peers in TIKR (It’s free!) >>>

The Margin Clock Management Is Watching

The fundamentals under the rally are genuinely strong, which is why this is a debate and not a bubble. In fiscal Q2 2026, reported April 30, Apple posted $111.2 billion in revenue, up 17% year-over-year, a March-quarter record that cleared the top of guidance despite supply constraints. iPhone drove it at $57 billion, up 22%, and gross margin landed at 49.3%, above the high end of the guide. Strong quarter. The problem is what management said comes next.

Pressed on margins, Cook was unusually direct about memory costs, the price Apple pays for the DRAM and flash storage inside every device. “We expect significantly higher memory costs,” he said of the June quarter, adding that “beyond the June quarter, we believe memory costs will drive an increasing impact on our business.” That matters because memory pricing is cyclical and outside Apple’s control, and it is why management already raised prices on Macs, iPads, and Home devices on June 25, the very move that triggered the June low before the rotation rescued the stock.

Cook’s repeated line when analysts pushed for specifics was that Apple would “look at a range of options,” which is management-speak for further price increases if the squeeze worsens. The June-quarter guide already reflects it: gross margin is guided to 47.5% to 48.5%, a step down from the 49.3% Apple just printed. The bull case assumes Apple’s pricing power and Services mix absorb the hit. The bear case is that a 40x multiple leaves no room for a margin miss.

TIKR Advanced Model Analysis

- Current Price: $333.74

- Target Price (Mid): ~$442

- Potential Total Return: ~33%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for Apple stock (It’s free!) >>>

That target implies roughly 33% upside over about four years, a milder return than Apple’s recent run because the model assumes the valuation multiple compresses slightly from today’s stretched level rather than expanding further.

The two revenue drivers are Services, growing high-teens and carrying a 76.7% gross margin that lifts overall profitability, and the iPhone installed base, where 2.5 billion active devices feed both upgrades and Services attach. The margin driver is that Services mix shift; the primary risk is the memory-cost trajectory Cook flagged, which pressures product gross margin exactly as the multiple leaves little cushion. Upside: an expected fall foldable iPhone and a genuinely useful Siri reaccelerate the upgrade cycle and justify the premium. Downside: memory costs bite, iPhone demand normalizes, and a stock trading above consensus reverts toward the ~$318 the Street already sees.

Conclusion

The milestone is a headline; July 30 is the verdict. That is when Apple reports fiscal Q3 2026, and it is the print that decides whether this rally is a re-rating or a rotation that overshot. Watch two lines. First, gross margin: management guided 47.5% to 48.5%, so a result at or above the high end says the memory squeeze is contained and pricing power is holding, while anything below 47.5% confirms the bears’ margin fear. Second, June-quarter revenue growth against the 14% to 17% guide, which tells whether iPhone momentum survived once supply constraints stopped being the excuse.

It is also Tim Cook’s last earnings call as CEO before John Ternus takes over on September 1, which adds scrutiny to every forward-looking word. A stock at a record high, trading above what most analysts think it is worth, does not get the benefit of the doubt on a soft quarter. In under two weeks, Apple has to show the crown was earned, not borrowed.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Apple?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Apple, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Apple alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!