Key Stats for Applied Materials Stock

- Friday’s Performance: -6%

- 52-Week Range: $154 to $740

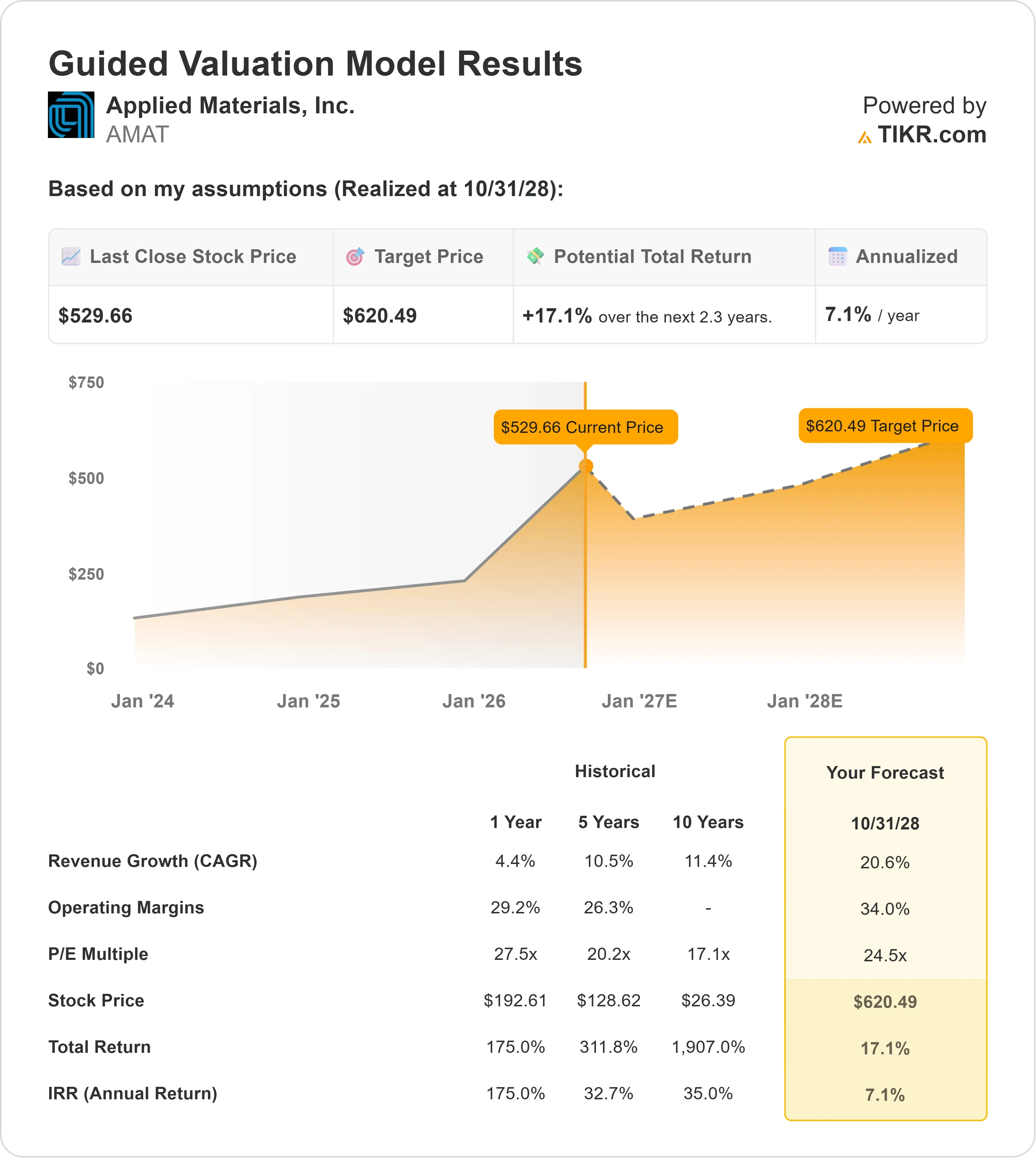

- Valuation Model Target Price: Around $620

- Implied Upside: Around 17%

Analyze your favorite stocks like Applied Materials with TIKR (It’s free) >>>

What Happened?

Applied Materials stock fell about 6% on Friday to $530 and briefly traded near $513 as investors questioned whether enormous AI infrastructure spending can generate enough profit to support premium valuations for semiconductor equipment companies. Approximately 10 million shares changed hands, slightly above the stock’s recent average, showing that the broader reassessment of AI stocks reached one of the industry’s largest chipmaking-equipment suppliers.

The stock fell because Moonshot AI’s Kimi K3 launch and reported setbacks involving Google’s Gemini 3.5 Pro revived doubts about whether massive AI infrastructure investments will produce adequate returns. Those concerns triggered profit-taking across the semiconductor sector, with the PHLX Semiconductor Index losing about 10% for the week. Applied declined more sharply than direct competitors Lam Research, which fell 2%, and KLA, which dropped 3%. Lam competes with Applied in chip-deposition and etching equipment, while KLA competes in inspection and process-control systems that identify manufacturing defects, making their smaller declines evidence that selling pressure was particularly sharp in Applied despite no new business warning.

Applied Materials’ June 25 DRAM and Advanced Packaging Master Class provided a fundamental counterpoint to the selloff. Management expects equipment spending on DRAM, the working memory that supplies processors with data, to remain more than twice as large as spending on NAND equipment, which produces lower-cost flash storage. Kevin Moraes said revenue from advanced packaging, which connects processors and memory closely to improve speed and energy efficiency, is expected to rise “more than 50% to more than $2 billion” this year. Applied also introduced systems that help manufacturers stack high-bandwidth memory, create metal connections between chips, and find microscopic defects, with two new inspection products already in production at multiple advanced-packaging customers across memory and logic.

Wall Street remained constructive despite the decline. UBS maintained its Buy rating and raised its price target to $705 from $570 on July 15, following increases by Needham to $740 from $530 and Stifel to $650 from $530 on July 10. Those targets sit around 23% to 40% above Friday’s closing price, although they depend on AI-related equipment demand remaining strong. The next major test is the fiscal third-quarter report expected around August 13, when Applied will need to support its guidance for around $9 billion in revenue and adjusted EPS of around $3.40 while demonstrating that orders for advanced processors, high-bandwidth memory, and chip-packaging equipment remain healthy.

Value Applied Materials instantly (Free with TIKR) >>>

Is Applied Materials Fairly Valued?

Under the valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): Around 21%

- Operating Margin: Around 34%

- Exit P/E Multiple: Around 25x

The 21% revenue-growth assumption is demanding because it is nearly twice Applied Materials’ five-year historical growth rate of approximately 11%. Reaching it requires chipmakers to continue expanding production of advanced processors and high-bandwidth memory while adopting more complex packaging methods. Applied Global Services, which generates recurring revenue from maintenance, replacement parts, and equipment upgrades, must also continue growing as the company’s installed equipment base expands.

The 34% operating-margin assumption is also demanding relative to Applied’s recent history. Operating income increased from $7.20 billion in fiscal 2021 to $8.51 billion in fiscal 2025, but operating margin declined from 31.2% to 30.0%, showing that higher earnings have not automatically produced greater profitability. Applied’s latest quarterly adjusted operating margin improved to 32.1%, but reaching 34% still requires higher factory utilization, continued service growth, and a larger contribution from specialized AI equipment.

Applied’s latest quarterly revenue growth of 11% was similar to KLA’s 11% but trailed Lam Research’s 24%. Its 32.1% adjusted operating margin also remained below Lam Research’s 35%. KLA remains a strong competitive benchmark because its process-control systems identify defects during chip production, an increasingly valuable capability as AI processors become more complex and expensive to manufacture.

The exit multiple of around 25x earnings sits below Applied’s current forward valuation but above its five-year historical average near 20x. This assumes that AI-driven growth preserves part of the stock’s valuation premium even as the semiconductor investment cycle matures. Earnings growth, rather than a higher valuation multiple, therefore needs to generate most of the projected return.

See analysts’ growth forecasts and price targets for Applied Materials (It’s free) >>>

Based on these inputs, the model estimates a target price of around $620, implying around 17% total upside over a little more than two years and an annualized return of around 7%. This suggests Applied Materials is fairly valued rather than clearly undervalued because the model already assumes substantial revenue acceleration and margin expansion.

Over the next 12 months, the largest earnings catalyst is the conversion of AI infrastructure spending into equipment orders for advanced processors, high-bandwidth memory, and advanced packaging, supporting management’s expectation that its semiconductor equipment business can grow more than 30% in calendar 2026. Gate-all-around transistor systems, which improve chip speed and power efficiency by giving the transistor gate greater control, can increase Applied’s revenue because customers need additional manufacturing steps and specialized materials. Panel-level packaging, which builds larger chip packages on rectangular panels instead of traditional circular wafers, could create another equipment opportunity as AI accelerators combine more processors and memory. Applied Global Services adds stability, with quarterly revenue rising 17% to $1.67 billion and operating margin improving to 29.2% from 26.6%, while China’s 27% share of quarterly revenue creates exposure to export restrictions and local competitors.

At $530, Applied Materials appears fairly valued, with strong AI-related business drivers balanced by ambitious model assumptions and an expected annual return of only around 7%.

How Much Upside Does AMAT Stock Have From Here?

Investors can estimate Applied Materials’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Applied Materials in under 60 seconds with TIKR (It’s free) >>>