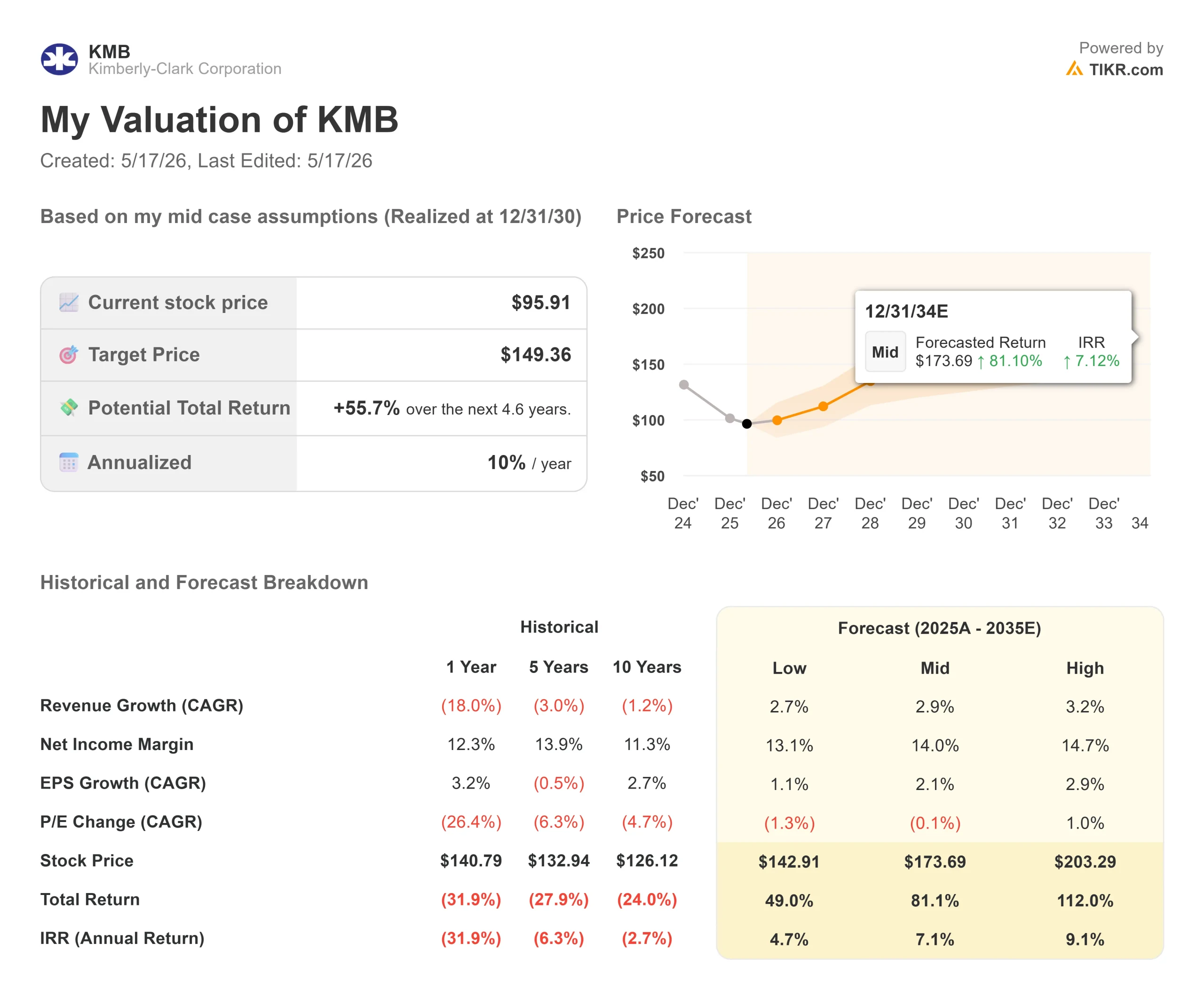

Key Stats for Kimberly-Clark Stock

- Current Price: $95.91

- Street Target: ~$114

- TIKR Target Price (Mid): ~$149

- Potential Total Return: ~56%

- Annualized IRR: ~10% / year

- Earnings Reaction: (2.38%) on 4/28/26

- Max Drawdown: (35.31%) on 4/7/26

- Dividend Yield: 5.4%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Kimberly-Clark Corporation (KMB) has shed 35% from its 52-week high, and investors still holding the stock are focused on two things: whether the Kenvue acquisition will create the value management is promising, and whether the dividend can survive the transformation. At the May 14, 2026, annual meeting, Chairman and CEO Mike Hsu addressed both directly, on the record.

When Q1 2026 earnings landed on April 28, adjusted EPS of $1.97 beat the $1.93 consensus, with actual revenue coming in at $4.163 billion. The market still sent the stock down 2.38% that day. The annual meeting, held two weeks later, is where Hsu went beyond the quarterly numbers and put the long-term thesis on the table.

What Hsu Said About the Kenvue Acquisition

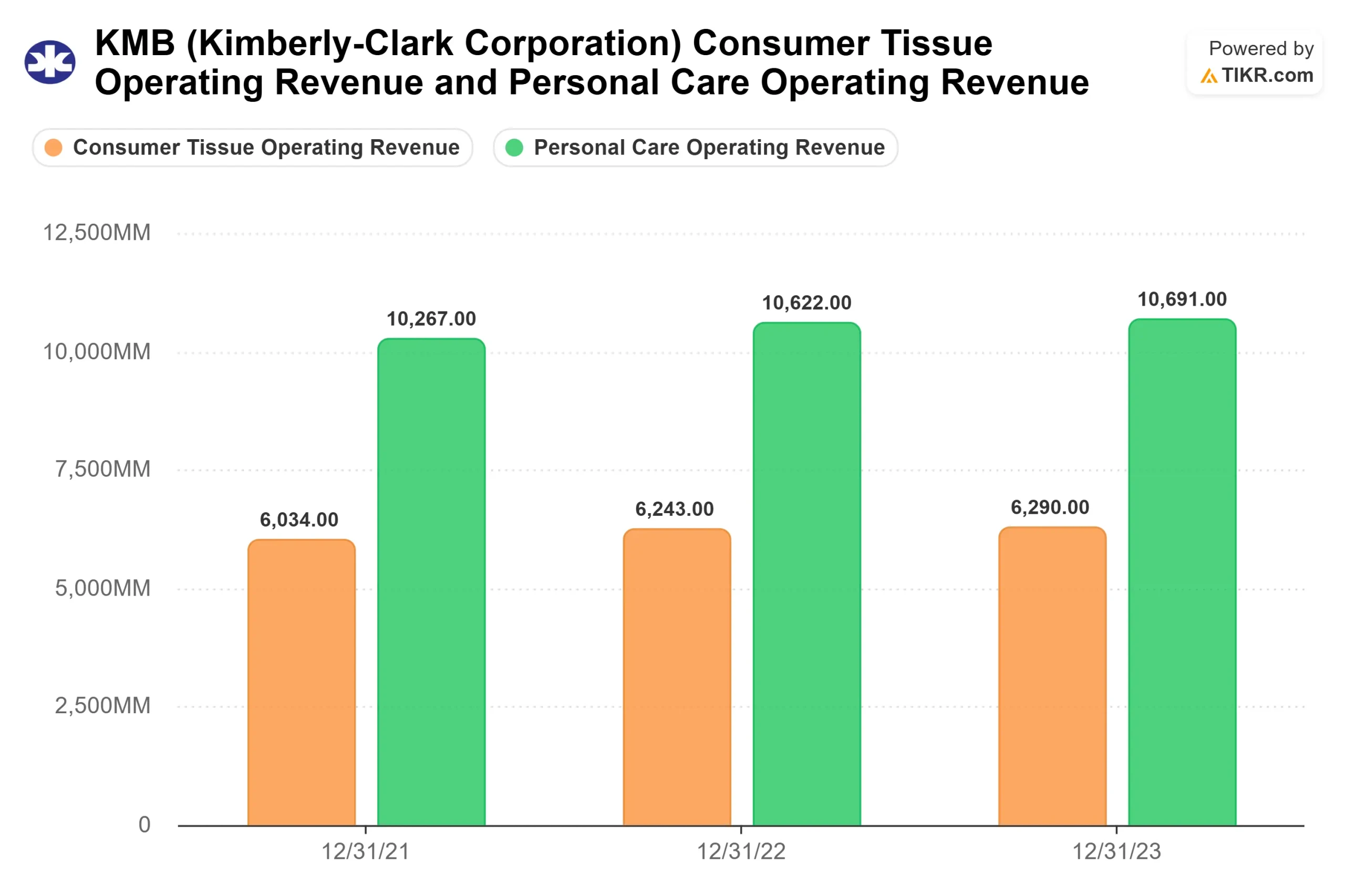

Hsu did not frame the Kenvue acquisition as a bet. He framed it as the natural extension of Powering Care, the company’s two-year operating transformation, applied to a new set of assets. “We’ve hit the ground running in 2026, and we are excited to seamlessly plug Kenvue’s brands and businesses into our proven durable operating model,” he told shareholders at the annual meeting. Volume-plus-mix growth in the core personal care business has run for nine or ten consecutive quarters as of Q1 2026, per the April 28, 2026, earnings release.

The Kenvue deal was announced in November 2025 at an enterprise value of approximately $48.7 billion, per Kimberly-Clark’s SEC filings. Shareholders from both companies approved the transaction in January 2026, with roughly 96% of KMB shares present voting in favor. The deal is expected to close in the second half of 2026, pending regulatory approval. Kenvue’s portfolio includes Tylenol, Neutrogena, and Listerine, brands that currently sit entirely off KMB’s books.

Alongside the Kenvue deal, Kimberly-Clark is contributing its International Family Care and Professional, or IFP, business, which covers tissue and professional products outside North America, to a joint venture with Suzano, a Brazilian pulp producer. Suzano takes 51% for approximately $1.7 billion in cash proceeds, per SEC filings, while KMB retains a 49% stake. Those proceeds help fund the cash portion of the Kenvue acquisition. Hsu confirmed at the annual meeting that the IFP joint venture remains on track to close in mid-2026.

Together, the two moves strip out lower-growth commodity-adjacent tissue operations and replace them with consumer health brands carrying structurally higher margins. That portfolio shift is the core of the bull case.

See historical and forward estimates for Kimberly-Clark stock (It’s free!) >>>

The Dividend Question, Answered on the Record

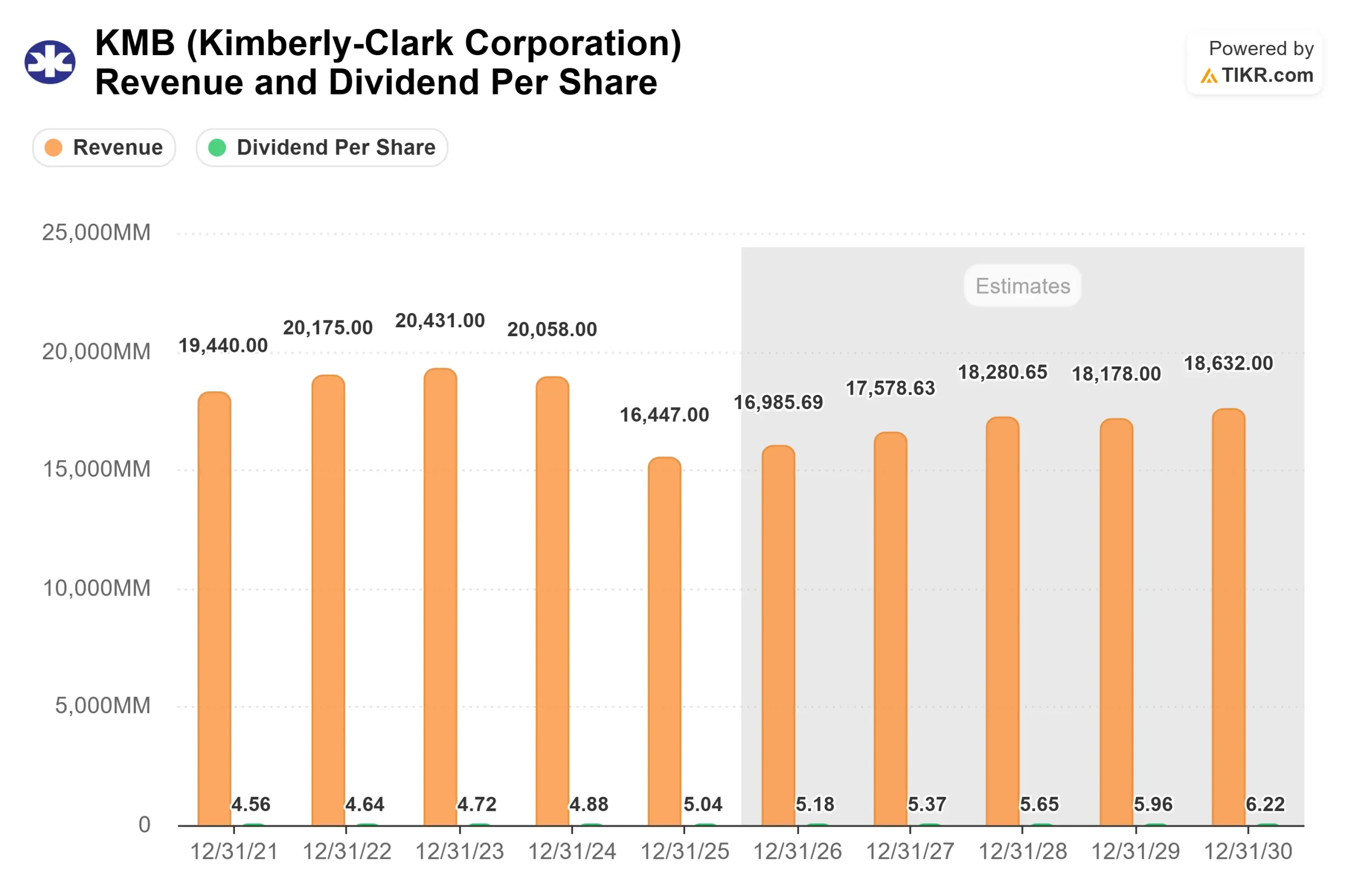

One exchange at the annual meeting did not make any earnings recap. A long-time shareholder named Phil Brown raised the payout ratio directly, noting his math showed it had reached a higher level. Hsu was candid: the 2025 payout ratio looked elevated because noncash restructuring charges had depressed reported earnings, not because the dividend itself was under pressure. “We feel great from a cash flow perspective that the dividend is an appropriate ratio for what the company can afford,” Hsu told Brown.

The TIKR data lets investors test that claim. The trailing payout ratio stands at 79.0%, and LTM free cash flow sits at approximately $1.05 billion. But TIKR’s forward estimates project free cash flow recovering to around $2.02 billion in 2026 as restructuring charges normalize, with free cash flow margins expanding from 10% in 2025 to around 12% by year-end 2026. If that recovery holds, the dividend coverage picture improves meaningfully.

KMB has raised its dividend for 54 consecutive years, qualifying it as a Dividend King, a company with at least 50 straight years of annual dividend increases. The 5.4% yield is among the highest in the consumer staples peer group. Kenvue’s acquisition will require issuing approximately 280 million new shares, per Kimberly-Clark’s 10-Q filing, which introduces near-term per-share dilution. Hsu’s pledge at the annual meeting to keep growing the dividend was direct.

How KMB Is Priced Against Peers

At 10.44x NTM EV/EBITDA, KMB trades above the peer group median of 8.36x from TIKR’s competitors page, but well below Procter & Gamble at 14.86x and Church & Dwight at 16.43x. The Clorox Company trades at 10.40x, roughly in line with KMB. On NTM P/E, KMB’s 12.95x sits below both Procter & Gamble’s 20.46x and the peer median of 13.93x.

KMB’s discount to peers is close to the widest it has been in years. Whether it closes depends on how cleanly the company executes two simultaneous deal closings under the same transformation framework.

See how Kimberly-Clark performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $95.91

- Target Price (Mid): ~$149

- Potential Total Return: ~56%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Kimberly-Clark stock (It’s free!) >>>

The mid-case target of around $149 by 12/31/30 rests on two CAGR drivers: organic volume-plus-mix growth in core personal care, and Kenvue integration, adding consumer health revenue that KMB does not currently carry. The model projects a revenue CAGR of around 3% through 2030, with net income margins expanding to around 14%.

The margin driver is productivity. Hsu has set 6% annual gross productivity as the operational benchmark, a rate matched in Q1 2026 per the April 28 earnings release. That engine funds reinvestment in innovation while absorbing input cost pressure.

The primary risk is execution complexity. This is the largest acquisition in Kimberly-Clark’s history, run alongside an active portfolio divestiture. At around 10x forward EV/EBITDA, the market is already pricing in meaningful uncertainty. Synergy shortfall or regulatory delay would extend that discount. A clean, on-time close would begin to close it.

Conclusion

The single event that defines KMB’s trajectory over the next twelve months is regulatory clearance for the Kenvue deal. A clean close in the second half of 2026, with synergy targets intact, removes the biggest overhang on the stock. A delay into 2027 or a demand for material divestitures resets the timeline and likely pushes the stock lower. Hsu’s tone at the May 14 annual meeting was forward-leaning, not defensive. The market is still pricing in uncertainty. That gap closes or widens when regulators decide, which makes the regulatory calendar the only data point that really matters between now and year-end.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Kimberly-Clark?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Kimberly-Clark, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Kimberly-Clark alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Kimberly-Clark on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!