Key Takeaways for Snowflake Stock

- Snowflake posted Q1 FY2027 product revenue of $1.334 billion, with growth accelerating to 34% year-over-year from 30% the prior quarter.

- Operating losses narrowed for the eighth consecutive quarter, with operating margins improving to negative 22% from negative 41% eight quarters ago.

- Non-GAAP operating margin expanded over 300 basis points year-over-year to 12% as headcount additions held to just 17 organic hires in the quarter.

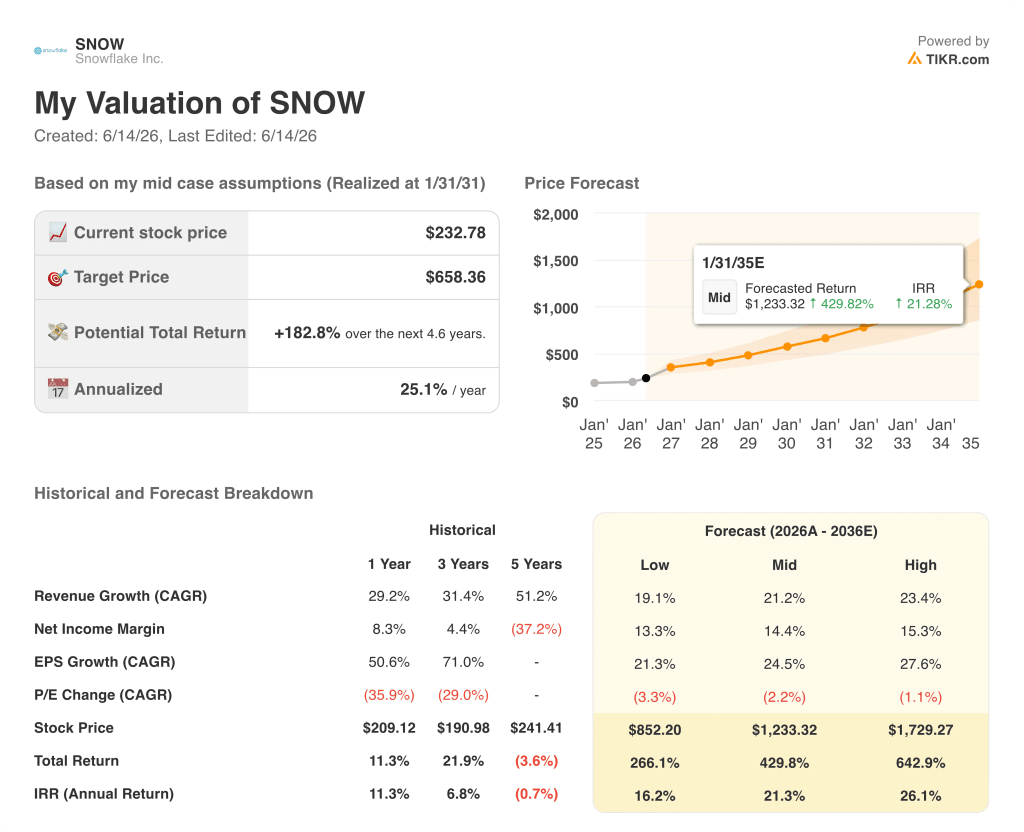

- TIKR’s model values Snowflake at approximately $658 by January 2031, implying around 183% total return from the current price of $233.

Snowflake Stock Posts 34% Product Revenue Growth as AI Compounding Takes Hold in Q1 FY2027

Snowflake Inc. (SNOW) reported Q1 FY2027 product revenue of $1.334 billion on May 27, 2026, with growth accelerating for the second consecutive quarter to 34% year-over-year.

CEO Sridhar Ramaswamy described the result in Q1 earnings call as the company’s “strongest sequential dollar growth in company history,” driven by both AI product traction and an acceleration in the core data cloud business.

Cortex Code, Snowflake’s AI coding agent known internally as CoCo, reached general availability on February 5, the first day of Q1, and became the primary catalyst behind the beat.

CFO Brian Robins told analysts that CoCo had “the largest driver to the increase in our forecast,” noting that the company layered its observed CoCo consumption behavior into the full-year model mid-quarter.

Snowflake raised its FY2027 product revenue outlook to $5.84 billion, representing 31% full-year growth, up from the 27% it had guided entering the year.

Net revenue retention improved to 126%, signaling that existing customers accelerated their spending on the platform rather than pulling back.

The company added 616 net new customers in the quarter, up 38% year-over-year, including 13 new Global 2000 accounts compared to 4 in the prior-year period.

Snowflake also announced a five-year, $6 billion expanded agreement with AWS to accelerate enterprise AI adoption globally.

Ramaswamy even framed the AI tailwind in structural terms: “AI is compounding Snowflake’s advantage in data.”

Snowflake’s Revenue Growth Outran Opex for the First Time in Years, and the Margin Gap Is Closing Fast

Snowflake’s revenue reached $1.39 billion in Q1 FY2027, a 33% year-over-year increase that exceeded the $1.32 billion Wall Street had estimated.

Gross profit grew to $930 million, with gross margins holding at 67%, consistent with the prior three quarters.

The more consequential shift ran below gross profit, where total operating expenses of $1.23 billion grew meaningfully more slowly than revenue over the trailing eight quarters.

Operating income improved to a loss of $310 million, the smallest operating loss in eight quarters, as the gap between gross profit and total operating expenses continued to narrow.

Operating margins improved to negative 22% in Q1 FY2027, a recovery of roughly 19 percentage points from the negative 41% operating margin recorded eight quarters earlier.

SNOW Leads MongoDB and Elastic on Revenue Growth, While Palantir Runs a Different Race

Snowflake posted 33% revenue growth in Q1 FY2027, its highest rate in eight quarters, reaching a level that MongoDB (MDB) and Elastic (ESTC) have not matched in any quarter across the same period.

MongoDB grew revenue 25% in the most recent quarter, a rate it last exceeded two years ago, while Elastic posted just 16% growth, its slowest in the eight-quarter window.

Palantir (PLTR) reported 85% revenue growth in the most recent quarter, a figure that reflects a fundamentally different business mix weighted toward government contracts and direct AI platform licensing rather than consumption-based data infrastructure.

Snowflake’s 33% growth rate marks its second consecutive quarter of re-acceleration after troughing at 26% four quarters ago, a trajectory neither MongoDB nor Elastic has matched across the same stretch.

The competitive read is that Snowflake’s CoCo-driven consumption acceleration is not a sector-wide lift: MongoDB and Elastic have not moved in the same direction over the trailing eight quarters, which isolates the inflection as company-specific.

Is Snowflake Stock Undervalued in 2026? TIKR’s $658 Target Suggests Yes, If the Leverage Holds

TIKR’s model values Snowflake at approximately $658 by January 2031, implying around 183% total return from the current price of $233, or roughly 25% per year.

For that target to be credible, operating margins need to continue recovering at the pace the last eight quarters have demonstrated: opex growth held below revenue growth as the platform scales.

The income statement has already shown that mechanism is active, with 19 percentage points of operating margin recovery recorded since the operating loss peaked eight quarters ago.

Should You Invest in Snowflake Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snowflake Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snowflake Inc. alongside every other stoc

Access Professional Tools to Analyze SNOW stock on TIKR for Free →