Key Takeaways for Disney Stock

- The Walt Disney Company reported Q2 fiscal 2026 revenue of $25.17 billion, up 7% year over year.

- Operating income reached $3.90 billion in the most recent quarter, with operating margins expanding to roughly 16%.

- Entertainment streaming operating income surged 88% year over year, with the segment crossing into double-digit margins for the first time.

- TIKR’s mid-case model values Disney stock at approximately $128 by September 2030, implying around 28% total return from the current price of $100.

If Disney’s income statement is telling a margin recovery story the market isn’t fully pricing in, the data to verify it is already on TIKR. Explore Disney’s full financial history on TIKR for free →

Disney Stock Posts 7% Revenue Growth: What New CEO Josh D’Amaro Inherited and Where It Goes Next

The Walt Disney Company (DIS) delivered fiscal Q2 2026 revenue of $25.17 billion following its May earnings release, beating Wall Street’s estimate and marking the first quarterly report under new CEO Josh D’Amaro.

D’Amaro used his inaugural earnings call to frame four strategic priorities: creative excellence, streaming strengthening, ESPN’s direct-to-consumer build-out, and accelerating the Experiences business.

The transcript’s most concrete data point was in streaming, where entertainment direct-to-consumer (DTC) subscription video on demand revenue growth accelerated from 11% in Q1 to 13% in Q2.

D’Amaro tied that acceleration directly to churn reduction, stating that the integrated Disney+ and Hulu bundle continues to benefit retention, and that reducing churn may be “the single most significant opportunity” the company has.

Zootopia 2 generated $1.9 billion in global box office and crossed 1 billion hours streamed on Disney+, reinforcing management’s argument that franchise IP compounds across theatrical, streaming, and Experiences in a way competitors cannot replicate.

The Experiences segment produced both revenue and operating income that were Q2 records, despite domestic park attendance running down 1% due to international visitation headwinds that management expects to lap in Q3.

CFO Hugh Johnston addressed in MoffettNathanson conference that Disney is “betting $8 billion this year” on its own stock through buybacks, framing the repurchase commitment as a direct expression of management’s view that DIS is undervalued.

Disney’s operational transformation is accelerating — and the income statement is the place to see exactly how far it has come. Pull up Disney’s segment-level data and margins on TIKR for free →

Disney’s Streaming Margin Cross Above 10% Signals a Structural Shift the Stock Hasn’t Priced In

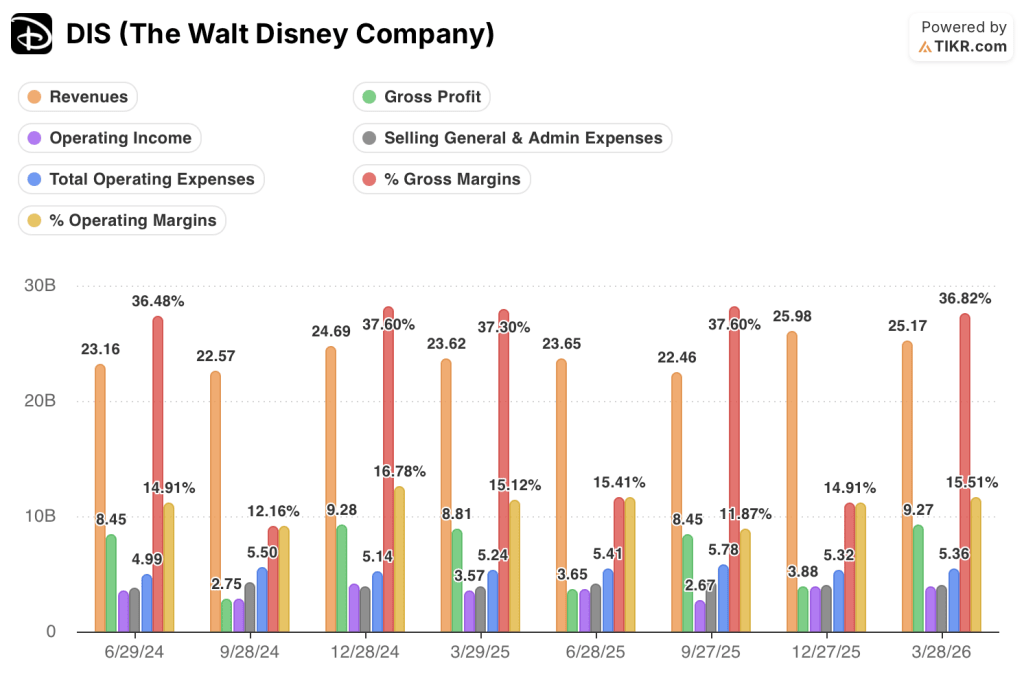

Revenue of $25.17 billion in the March quarter grew 7% year over year, sustaining the positive trajectory from the prior period.

Gross profit of $9.27 billion came in at a 37% gross margin, consistent with the year-ago period when the same metric sat at roughly 37%.

The structural argument lives one level lower: operating income of $3.90 billion in the most recent quarter reflects a business finally converting top-line growth into bottom-line expansion, with operating margins reaching approximately 16%.

That operating margin figure represents a meaningful recovery from the trough of 12% recorded in the September 2024 quarter.

The cost dynamic behind the recovery shows SG&A holding at $3.96 billion in the March 2026 quarter, essentially flat versus the year-ago period of $3.92 billion, while revenue climbed 7%.

When revenue scales faster than SG&A, operating leverage converts directly into margin points; the eight-quarter income statement shows exactly that pattern from the September 2024 trough to the present.

Total operating expenses of $5.36 billion in the most recent quarter are nearly flat with the $5.24 billion recorded in the year-ago period, reinforcing that the cost structure is not expanding in proportion to the top line.

The tension inside this story is that gross margins remain range-bound near 37%, meaning the expansion in operating margin is entirely a function of opex discipline rather than pricing power, a distinction that will matter when content investment cycles back up.

Disney Leads Comcast and Warner Bros. Discovery on Operating Margins, But the Gap With Comcast Is Narrowing

Disney’s operating margin of roughly 16% in the March 2026 quarter sits above Warner Bros. Discovery’s (WBD) 9%, a spread that reflects the structural drag WBD carries from its debt-heavy balance sheet and ongoing content rationalization.

Meanwhile, Comcast Corporation (CMCSA) posted a 13% operating margin in the same period, trailing Disney by approximately three points after running as high as 22% in the June 2024 quarter.

The more revealing data point is the directional divergence: Disney’s margin recovered from a 12% trough in the September 2024 quarter back toward 16%, while Comcast’s margin compressed from that same June 2024 peak of 22% to 13% by March 2026.

Warner Bros. Discovery swung from negative 1% in the June 2025 quarter to positive 9% in March 2026, the steepest recovery of the three, though from the lowest absolute base.

Disney’s margin advantage over both peers has narrowed over eight quarters, which means the thesis that Disney’s opex discipline is differentiated depends on whether SG&A continues to hold flat as content investment cycles back up in the second half.

Is Disney Stock Undervalued in 2026? TIKR’s $128 Model Points to Margin Execution as the Key

TIKR’s model values Disney at approximately $128 by September 2030, implying around 28% total return from the current price of $100, or roughly 6% per year.

That target is credible if the operating leverage pattern visible in the income statement continues: specifically, if SG&A remains range-bound as revenue compounds at or above the current rate.

Johnston’s framing at MoffettNathanson that Disney is “building a reliable track record” as an earnings compounder is the condition the TIKR model is stress-testing; the August Q3 report will be the next data point that either confirms or challenges that thesis.

The TIKR model lets you stress-test every assumption behind that $128 target with your own inputs. Build your own Disney valuation model on TIKR for free →

Should You Invest in The Walt Disney Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Walt Disney Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Walt Disney Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DIS stock on TIKR for Free →

What did Disney say about parks demand on the Q2 2026 earnings call?

CFO Hugh Johnston confirmed domestic park and resort demand remains healthy and that bookings are pacing up strongly, with Q3 attendance expected to improve versus the 1% decline reported in Q2.

Is Disney stock a buy right now?

Disney stock trades near $100 while generating roughly 6% annualized total return under TIKR’s mid-case model, and management has committed to $8 billion in buybacks for fiscal 2026, signaling confidence in the current price level.