Key Takeaways for Trade Desk Stock

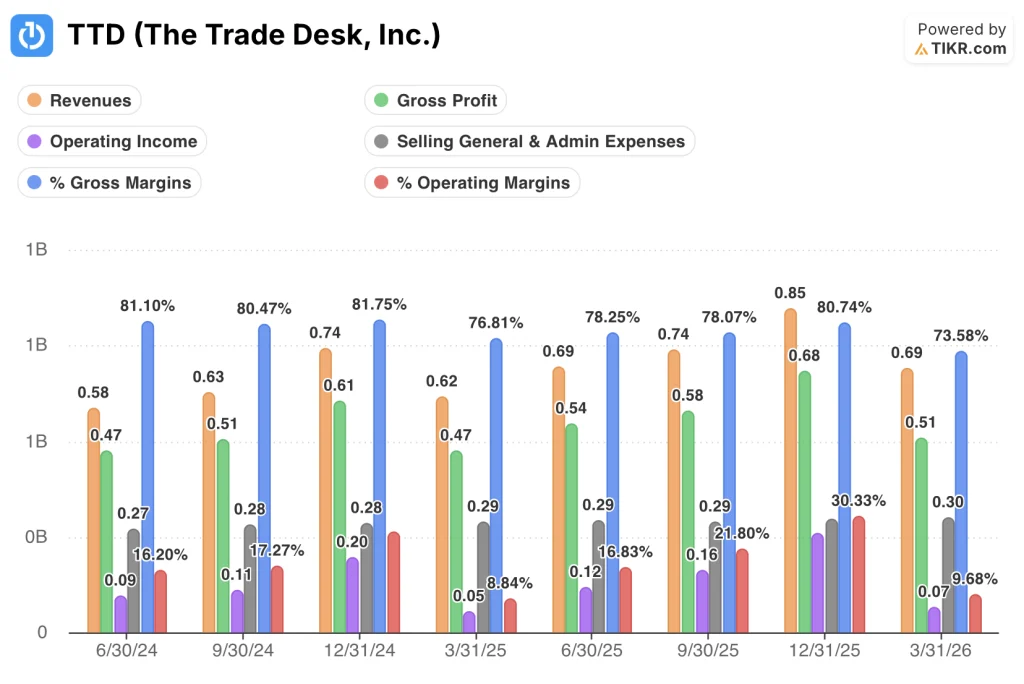

- The Trade Desk delivered Q1 2026 revenue of $689 million, growing 12% year over year and beating the $679 million Wall Street estimate.

- Operating margins compressed to 10% in Q1 2026, down from 30% in Q4 2025, driven by a sequential cost step-up as the company executes its year of disciplined reinvestment.

- JBP (joint business plan) signings grew 55% year over year in Q1, with 45 agreements signed in March alone, including a deal that will increase one client’s spend by 114%.

- TIKR’s mid-case model values Trade Desk stock at approximately $26 by December 2030, implying around 37% total return from the current price of $19.

TTD Posts 12% Revenue Growth in Q1 but Operating Margins Tell a More Complex Story

The Trade Desk (TTD), the largest independent demand-side platform (DSP) for programmatic advertising, posted Q1 2026 revenue of $689 million following its May earnings call, beating analyst estimates by roughly $10 million while simultaneously guiding Q2 revenue to at least $750 million, below the $771 million Wall Street had expected.

CEO Jeff Green framed the near-term pressure as a product of a deliberate investment posture, telling investors on the Q1 earnings call that “2026 is a year of disciplined reinvestment.”

The beat-and-guide-down dynamic landed against a backdrop of macro softness: Green cited geopolitical instability, tariffs, and consumer pressure on CPG and automotive brands as the primary headwinds dragging on advertiser budgets.

What the headline numbers obscured was the platform-level evidence of demand: total JBP count grew 55% year over year, with 45 new agreements executed in March, and new JBP deal spend grew 40% year over year during the quarter.

One example from Green illustrated the competitive trajectory: a major pharmaceutical advertiser that had shifted some investment to Amazon’s PG product returned to The Trade Desk in Q1 and signed a JBP that will increase its platform spend by 114% year over year.

CTV (connected television) led channel growth, representing a low-50s percent share of business in Q1, with audio growing faster than any other channel during the quarter.

International represented approximately 18% of revenue and grew faster than the domestic business, reflecting the benefit of multi-year investment in EMEA and APAC markets.

Trade Desk’s Operating Leverage Is Under Pressure, and the Income Statement Shows Why

Trade Desk’s revenue grew to $689 million in Q1 2026, marking the third consecutive quarter of sequential deceleration from the 19% year-over-year growth rate The Trade Desk posted a year prior.

Gross profit came in at $510 million for the quarter, reflecting the platform’s high-margin infrastructure but the gross margin rate fell to 74%, its lowest point across the eight quarters in the income statement.

Gross margin had held above 76% in every quarter through Q3 2025, making the Q1 2026 compression a visible step down rather than a one-quarter fluctuation.

The gap between gross margin and operating margin is where the cost story becomes clearest: operating income reached only $70 million in Q1 2026, leaving a 64-point spread between what the platform earns before overhead and what it earns after.

Operating margin landed at 10% in Q1 2026, essentially flat with the 9% posted in Q1 2025, which means a full year of revenue growth produced no operating leverage on a year-over-year comparable basis.

The sequential picture sharpens the tension further: operating margin compressed from 30% in Q4 2025 to 10% in Q1 2026, a 20-point swing that reflects the seasonal pattern but also the cost step-up from continued investment in platform operations and AI tooling.

SG&A held at $300 million in Q1 2026, unchanged from Q4 2025, even as revenue dropped sequentially from $850 million to $690 million, confirming the fixed-cost nature of the current investment phase.

The Trade Desk Trails Alphabet and Meta on Operating Margins, and Magnite Shows the Gap Is Not Just Scale

The Trade Desk posted a 10% operating margin in Q1 2026, running 26 points below Alphabet’s 36% in the same quarter and 31 points below Meta’s 41%.

That gap has been structurally consistent across all eight quarters in the data: Alphabet has held operating margins between 30% and 34% throughout the period, and Meta has held between 38% and 48%, while The Trade Desk has ranged from 9% to 26%.

Magnite, the closest pure-play ad-tech comparable in this dataset, posted a 5% operating margin in Q1 2026, which confirms that single-digit margins in Q1 are not unique to The Trade Desk’s cost posture.

The most instructive quarter in the comparison is Q4 2024, when The Trade Desk reached 26% operating margin while Magnite hit 21%, narrowing the gap between the two ad-tech platforms to its tightest point in the dataset.

What Q1 2026 shows is that the seasonal compression is real for both ad-tech names: The Trade Desk fell from 30% to 10% sequentially, and Magnite fell from 25% to 5%, while Alphabet and Meta absorbed the same seasonal turn with far smaller drawdowns.

The structural question for the TIKR $26 mid-case is whether The Trade Desk can sustain the 21% to 26% operating margin range it demonstrated in Q3 and Q4 2025 as revenue re-accelerates, rather than settling into the single-digit seasonal trough as the new baseline.

Is Trade Desk Stock Undervalued in 2026? TIKR’s $26 Mid-Case Model Says the Business Has to Deliver

TIKR’s model values The Trade Desk at approximately $26 by December 2030, implying around 37% total return from the current price of $19, or roughly 7% per year.

That target is credible only if the operating leverage that disappeared in Q1 2026 begins to surface as the cost cycle matures: the model requires the 64-point gap between gross margin and operating margin to narrow as revenue scales against a stabilizing cost base.

The company’s own guidance for a full-year adjusted EBITDA margin of at least 40% signals management believes cost discipline will hold through the investment phase, which is the central assumption the mid-case depends on.

Should You Invest in The Trade Desk, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Trade Desk, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Trade Desk, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TTD stock on TIKR for Free →