Key Stats for Meta Platforms Stock

- 52-Week Range: $520.26 to $796.25

- Current Price: $570.98

- Street Mean Target: ~$829

- TIKR Target Price (Mid): ~$1,181

- TIKR Annualized IRR (Mid): ~17% per year

- Q1 2026 Revenue: $56.3B (up 33% year over year)

- Q1 2026 EPS: $10.44 (vs. $6.66 consensus)

- Q1 2026 Operating Margin: 41%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

A Record Quarter That Still Sent the Stock Lower

It is a strange place to find a company like Meta (META), with revenue of $56.3 billion, up 33% year over year, and EPS of $10.44, against a consensus of $6.66. The Family of Apps segment, which includes Facebook, Instagram, WhatsApp, and Messenger, generated $26.9 billion in operating income at a 41% margin. These are not the numbers of a business in trouble.

The problem is the bill that comes with them. Meta raised its 2026 capital expenditure guidance to between $125 billion and $145 billion, up from an already ambitious prior forecast of $115 billion to $135 billion. That number stops investors in their tracks, and it has. The stock dropped roughly 10% the day after earnings and has stayed under pressure since.

What the market is wrestling with is straightforward: the income statement looks exceptional, and the balance sheet is being asked to fund a vision that won’t show up in earnings for years. Those two things can both be true at the same time, and right now the stock is reflecting the tension between them.

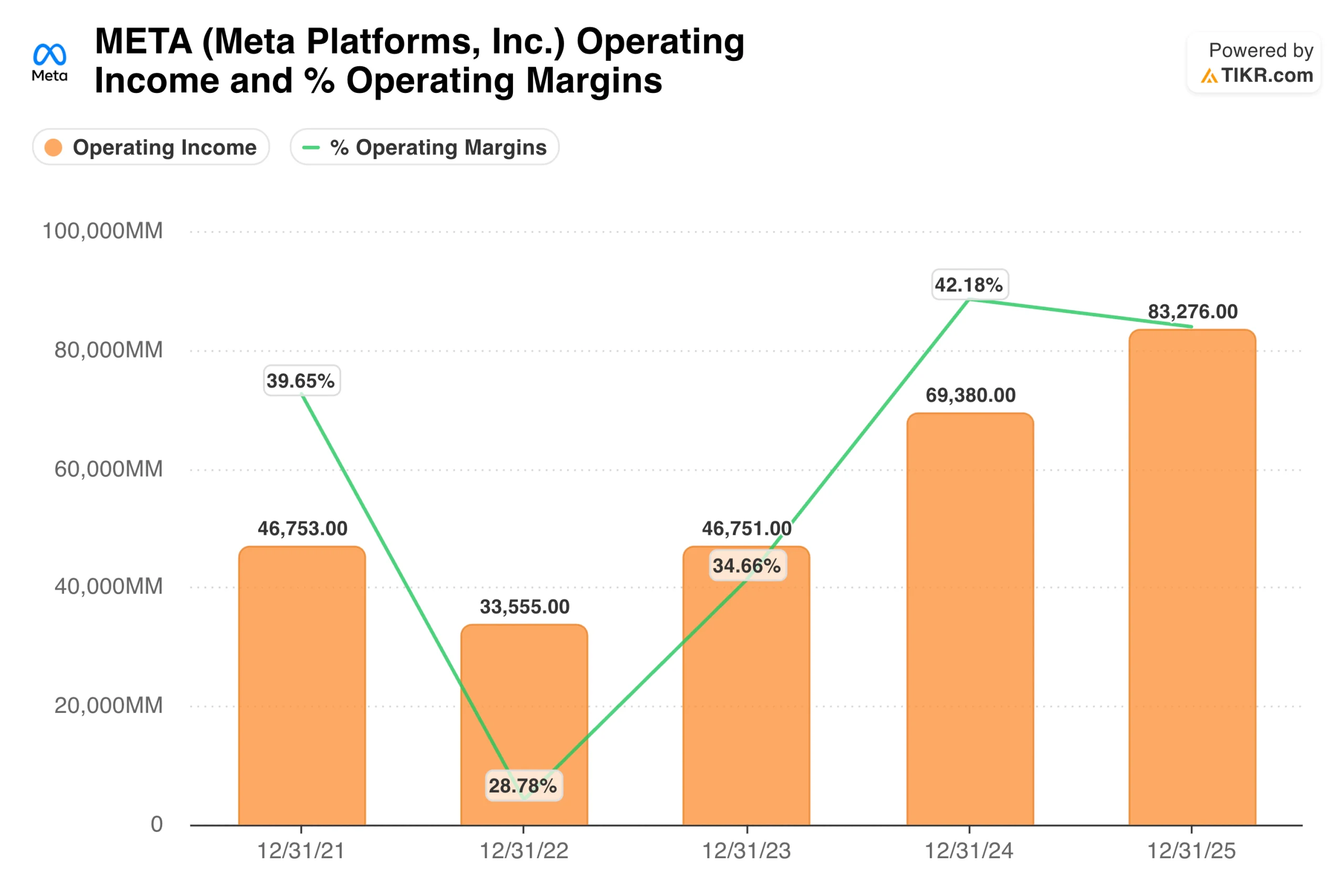

The operating income chart tells the story of how Meta got here. After the brutal 2022 drawdown, when margins collapsed to 29%, and the stock lost two-thirds of its value, Zuckerberg initiated what he called the “year of efficiency.”

Operating income recovered from $33.6 billion in 2022 to $83.3 billion in 2025, with margins expanding back above 42%. That recovery is what gives Meta the financial foundation to spend at this scale now. The question is whether the market gives them credit for the execution history or penalizes them for the spending ahead.

See historical and forward estimates for META stock (It’s free!) >>>

What $130 Billion in AI Capex Is Actually Buying

Meta’s AI strategy is different from most of what gets discussed under that umbrella. The company is not building a cloud business or selling AI services to enterprises. It is using AI to make its own advertising products better, reach more people more effectively, and retain users across a family of apps that already touch 3.56 billion people daily.

The Advantage+ ad suite, which uses machine learning to automate targeting and creative optimization, is already driving measurable revenue growth. Ad impressions delivered grew 19% year over year globally in Q1, and average price per ad grew 12%, meaning Meta is getting both more volume and more pricing from the same underlying user base. That combination is what a healthy advertising business looks like.

The capex is also funding Llama, Meta’s open-source AI model, and the compute infrastructure needed to run AI features at scale across WhatsApp, Instagram, and Messenger.

Mark Zuckerberg has been direct about the ambition: Meta AI is already being used by more than a billion people, and the goal is to make it the most widely used AI assistant in the world. Whether that translates into meaningful standalone revenue is still an open question, but the advertising flywheel it is already reinforcing is not.

Reality Labs continues to operate at a loss, $4 billion in Q1 alone, and remains the segment that skeptics point to as capital being deployed without a visible return timeline. That criticism is fair. It has been fair for several years.

Analyze Meta Platforms stock on TIKR Free→

What the TIKR Model Says About Meta’s Valuation

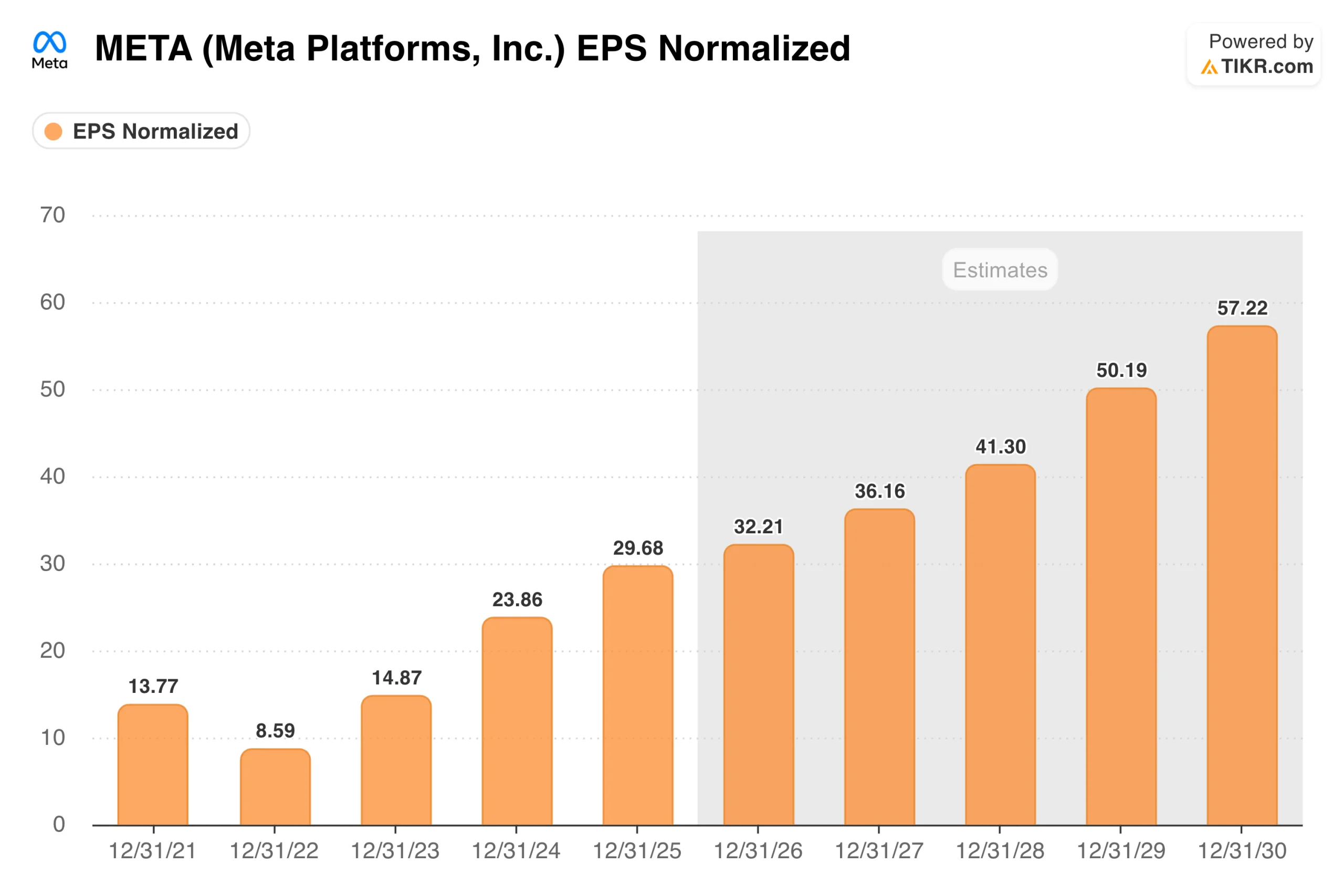

The EPS chart shows what consensus is underwriting. Normalized EPS grew from $8.59 in 2022 to $29.68 in 2025, and analysts expect it to reach around $32 in 2026, accelerating toward $57 by 2030 as AI investment matures and operating leverage kicks in.

At a current price near $571, Meta trades at roughly 18 times next year’s earnings estimate, which is a relatively modest multiple for a business growing revenue at 33% with 41% operating margins.

TIKR’s valuation model targets around $1,180 for Meta stock, with a mid-case annualized return of about 17% through 2030. The model assumes revenue growing at around 16% annually, with net income margins of around 33%, reflecting some compression from heavy AI infrastructure spending before operating leverage reasserts itself.

The scenario range skews meaningfully to the upside, with the high case implying a stock price approaching $2,700 by 2035 if advertising growth stays strong and AI monetization develops on schedule.

The bull and bear cases here are less about the advertising business, which is durable and growing, and more about whether the capex creates a lasting competitive advantage or simply inflates the cost structure.

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Bulls Are Betting On

- The advertising machine keeps compounding. Revenue grew 33% in Q1 with 41% operating margins while spending at an extraordinary rate. That combination is rare and suggests the core business has greater pricing power and efficiency than the capex narrative implies.

- AI is already working. Ad impression growth of 19% and average price per ad growth of 12% in the same quarter are not coincidences. Advantage+ and Meta’s broader AI ad tooling are showing up in the numbers now, not in some future period.

- The multiple is reasonable for the quality. At around 18 times forward earnings, Meta is not priced for perfection. The Street’s mean target of around $829 implies roughly 45% upside from current levels, and that is before any AI monetization beyond advertising.

- 3.56 billion daily users is a moat. No advertising platform on earth reaches this many people. That distribution advantage makes Meta’s AI investments structurally different from those of a company building from scratch.

What the Bears Are Watching

- $ 130+ billion in annual capex is an enormous amount. Even for a business generating Meta’s level of cash flow, sustaining this level of investment while expanding margins is a challenge. Any sign of revenue deceleration would quickly change the calculus.

- The equity offering overhang is real. Reports that Meta is considering a multibillion-dollar equity offering to fund AI infrastructure have added dilution concerns to an already unsettled stock. Until there is clarity on financing, that uncertainty does not go away.

- Reality Labs keeps burning cash with no clear payoff. The segment has cumulatively lost tens of billions of dollars, and there is still no product that demonstrates a path to profitability. At some point, investors’ patience wears thin.

- Regulatory pressure is building on multiple fronts. EU enforcement of the Digital Markets Act, ongoing US antitrust scrutiny, and youth safety litigation all represent headline risks that can move the stock independently of fundamentals.

See what analysts think about META stock right now (Free with TIKR) >>>

Should You Invest in META?

The honest framing for Meta right now is this: the business is as good as it has ever been, and the stock is cheaper than it has been in years relative to earnings.

What you are being asked to underwrite is whether spending at a scale that would have seemed impossible five years ago produces the AI infrastructure advantage that Zuckerberg says it will.

Put Meta through TIKR, and you can see the full earnings history, what analysts expect in the quarters ahead, and whether the current price reflects the business or the anxiety around spending. The numbers are worth looking at before you decide.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!