Key Stats for Arm Holdings Stock

- Today’s Performance: 11%

- 52-Week Range: $100 to $428

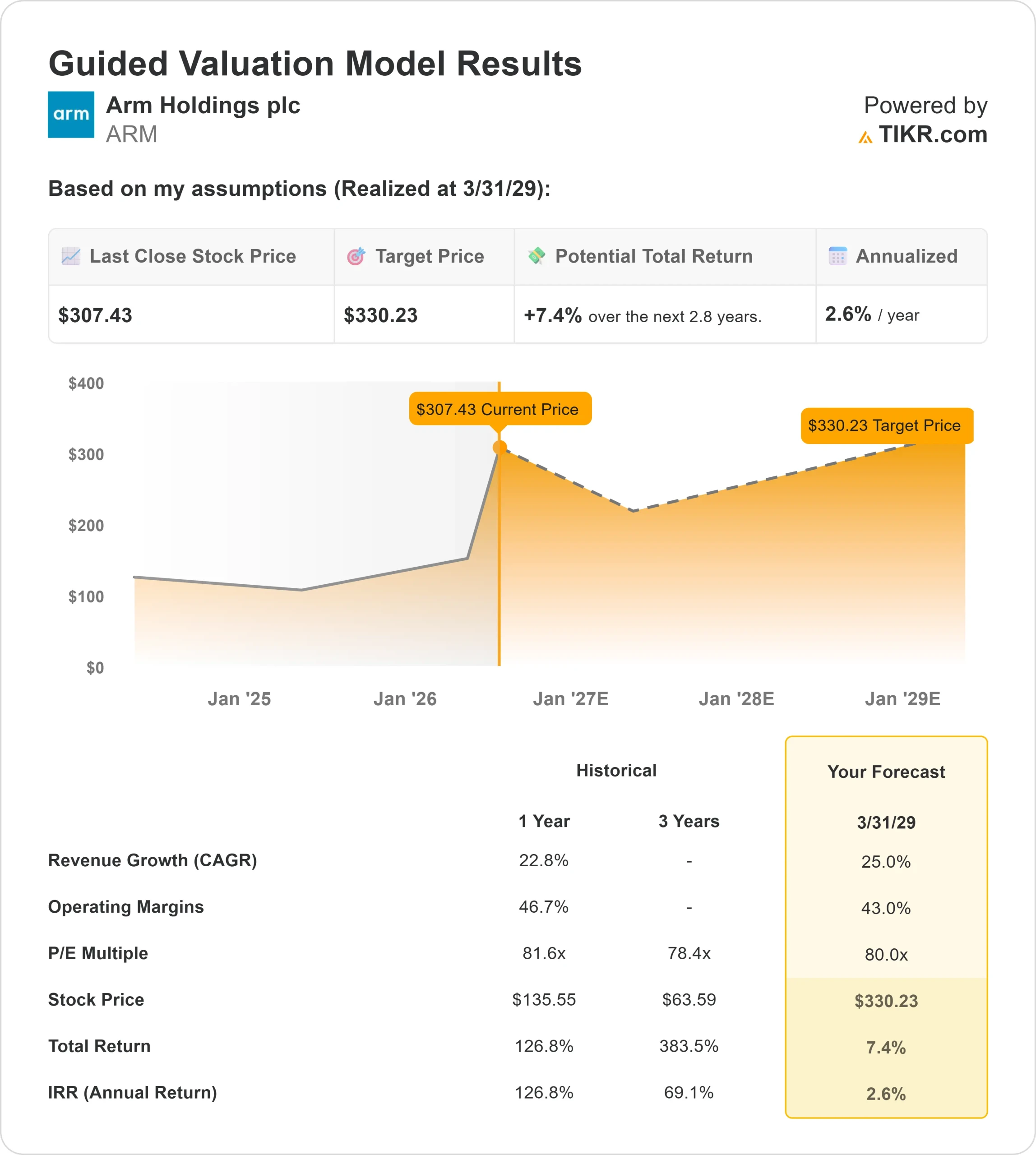

- Valuation Model Target Price: $330

- Implied Upside: 4%

Analyze your favorite stocks like Arm Holdings with TIKR (It’s free) >>>

What Happened?

Arm Holdings plc stock rose about 11% today, recently trading near $342 per share as investors moved back into one of the market’s most debated AI chip names. The rally came after Bank of America raised its price target, reinforcing the view that Arm could benefit from agentic AI, custom chips, and rising data center CPU demand.

The stock moved higher today because Bank of America raised its price target on Arm to $335 from $245 while keeping a Neutral rating, giving investors a clear reason to reprice the company’s AI opportunity. The firm’s call focused on stronger long-term server CPU demand and chiplet potential, which matters because chiplets are smaller chip components that can be combined into larger, more powerful processors. That is important for Arm because it earns licensing and royalty revenue when companies build chips using its architecture, giving it exposure to AI growth without needing to manufacture chips itself.

That makes Arm different from key semiconductor peers such as Nvidia, AMD, Intel, Broadcom, and Marvell. Nvidia and AMD compete directly in AI accelerators and server chips, Intel remains the main x86 CPU rival, while Broadcom and Marvell are major players in custom AI silicon and networking chips. The broader AI chip market still looks strong, with Nvidia’s latest quarterly revenue up 85% and AMD’s data center revenue up 57%, which helps explain why investors are willing to pay a premium for companies tied to AI infrastructure.

The recent move also followed Arm’s record Q4 fiscal 2026 earnings call, where revenue rose 20% year over year to $1.49 billion, licensing revenue grew 29% to $819 million, royalty revenue increased 11% to $671 million, and data center royalties more than doubled as Cloud AI demand accelerated. Full-year revenue reached a record $4.92 billion, up 23%, while non-GAAP EPS hit $1.77, and CEO Rene Haas said, “Customers want Arm at the center of the AI data center.”

Analyst updates added more momentum to the move. Mizuho recently lifted its target to $425 from $360, Barclays raised its target to $360 from $250, KeyBanc raised its target to $300 from $170, and Bank of America’s new $335 target moved much closer to the stock’s current price. Recent filings also showed institutional support, with Franklin Resources adding 10,385 shares to bring its ARM stake to about 1.5 million shares worth roughly $160 million, even as the stock’s high valuation keeps the debate intense.

Value Arm Holdings instantly (Free with TIKR) >>>

Is Arm Holdings Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 25%

- Operating Margins: around 43%

- Exit P/E Multiple: around 80x

Arm’s model already assumes very strong execution, with revenue compounding at 25% and operating margins staying above 40%, which leaves little room for disappointment after the sharp rally.

Based on these inputs, the model estimates a target price of around $330, which is slightly below the recent share price near $342. That suggests Arm looks slightly overvalued at current levels, even though its AI data center momentum remains strong.

The biggest upside driver is Arm’s push deeper into AI data centers through its AGI CPU, a new Arm-based processor designed to coordinate AI workloads more efficiently inside data centers.

See analysts’ growth forecasts and price targets for Arm Holdings (It’s free) >>>

Royalty growth also matters because higher Armv9 adoption, Compute Subsystems, and more Arm-based chips across cloud servers, networking, premium smartphones, and AI devices can raise revenue per chip without needing unit growth to surge.

At current levels, Arm’s future performance depends on proving that AI infrastructure demand can scale fast enough to justify one of the highest valuations in semiconductors, with data center royalties, AGI CPU progress, and premium royalty rates likely driving the next major move.

How Much Upside Does Arm Holdings Stock Have From Here?

Investors can estimate Arm Holdings’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Arm Holdings in under 60 seconds with TIKR (It’s free) >>>