Key Takeaways for Arista Networks Stock

- Arista Network’s revenue reached $2.71 billion in Q1 2026, up 35% year-over-year and above the company’s own guidance of $2.6 billion.

- Operating income hit $1.16 billion at a 43% operating margin, with operating income up 35% from the same quarter a year ago.

- Arista raised its full-year 2026 revenue outlook to $11.5 billion and lifted its AI networking revenue target to $3.5 billion.

The income statement tells a story the market is still debating: Arista Networks operates at nearly 43% operating margins while growing revenue at 35% annually, and the market appears to be discounting the durability of that combination. Explore Arista Networks Stock and its full income statement history free on TIKR →

Arista Networks Raises AI Revenue Target to $3.5 Billion After a 35% Revenue Beat in Q1 2026

Arista Networks (ANET) delivered first-quarter 2026 revenue of $2.71 billion, a 35% year-over-year increase that topped the company’s own guidance by more than $100 million, cementing its position as the dominant Ethernet networking vendor for AI infrastructure buildouts.

The quarter’s results were driven by AI and specialty cloud provider customers, with CEO Jayshree Ullal characterizing the current demand as “the best I’ve ever seen in my Arista tenure.”

Arista now categorizes AI networking into three use cases: scale-up (networking within a single rack), scale-out (connecting racks across a data center), and scale-across (interconnecting geographically distributed AI clusters), each representing a distinct revenue layer.

Scale-out remains the largest contributor, but Ullal told analysts that scale-across is expected to represent at least one-third of the company’s $3.5 billion AI revenue target in 2026, a segment that was “virtually nonexistent” just a year earlier.

On the enterprise side, Co-Presidents Ken Duda and Todd Nightingale highlighted wins across neocloud AI networks, service providers, insurance, and manufacturing, all unified by Arista’s single EOS operating system, which the company notes carries the fewest security vulnerabilities in the networking industry.

The company also unveiled its Extended Pluggable Optics (XPO) form factor at the Optical Fiber Conference, a next-generation connector now endorsed by more than 100 vendors, designed to deliver rack density improvements that management compared in significance to OSFP a decade ago.

One counterweight shaped the narrative: supply constraints spanning wafers, silicon, CPUs, optics, and memory are expected to persist for one to two years, pressuring gross margins as Arista absorbs elevated component costs rather than passing them fully to customers.

Chantelle Breithaupt, Arista’s CFO, also confirmed the company maintained its full-year gross margin guidance range at 62% to 64%, absorbing higher supply chain costs while raising the full-year revenue growth target from 25% to 28%.

EPS for the quarter came in at $0.87, up 32% from the prior year on a diluted share count of 1.27 billion.

ANET’s AI networking momentum just accelerated — see how the revenue trajectory compares against Wall Street’s forward estimates, free on TIKR. Analyze Arista Networks Stock and its full revenue and analyst estimate history on TIKR for free →

Gross Margin Under Pressure, Operating Leverage Holding: Inside Arista’s Q1 Income Statement

Revenue of $2.71 billion grew 35% year-over-year, accelerating from the 29% growth rate recorded in the prior quarter.

Gross profit reached $1.68 billion, up 31% from the same period last year, though the rate of gross profit growth trailed revenue growth for the first time in four quarters.

Gross margin compressed to 62% in Q1, down from 65% a year earlier, as large AI and cloud customers, who carry lower margin profiles than enterprise accounts, dominated the revenue mix.

The critical offset: total operating expenses held at $520 million, nearly flat sequentially despite a 9% quarter-over-quarter revenue increase, producing meaningful operating leverage as the business scaled.

Operating income of $1.16 billion carried a 43% operating margin, essentially matching the 43% level recorded a year ago despite the gross margin headwind from both customer mix and elevated supply chain costs.

R&D spending came in at $340 million, or 13% of revenue, reflecting Arista’s commitment to its product road map even as it absorbed component cost pressure at the gross profit line.

SG&A held at $180 million, or 7% of revenue, consistent with the prior quarter, indicating that go-to-market costs are scaling at a fraction of the pace of revenue growth.

The gross-to-operating margin gap has narrowed: in Q2 2024, gross margin ran at 65% while operating margin sat at 45%, a 20-point spread; in Q1 2026, gross margin fell to 62% while operating margin held at 43%, a 19-point spread, confirming that opex discipline is absorbing the gross margin pressure rather than amplifying it.

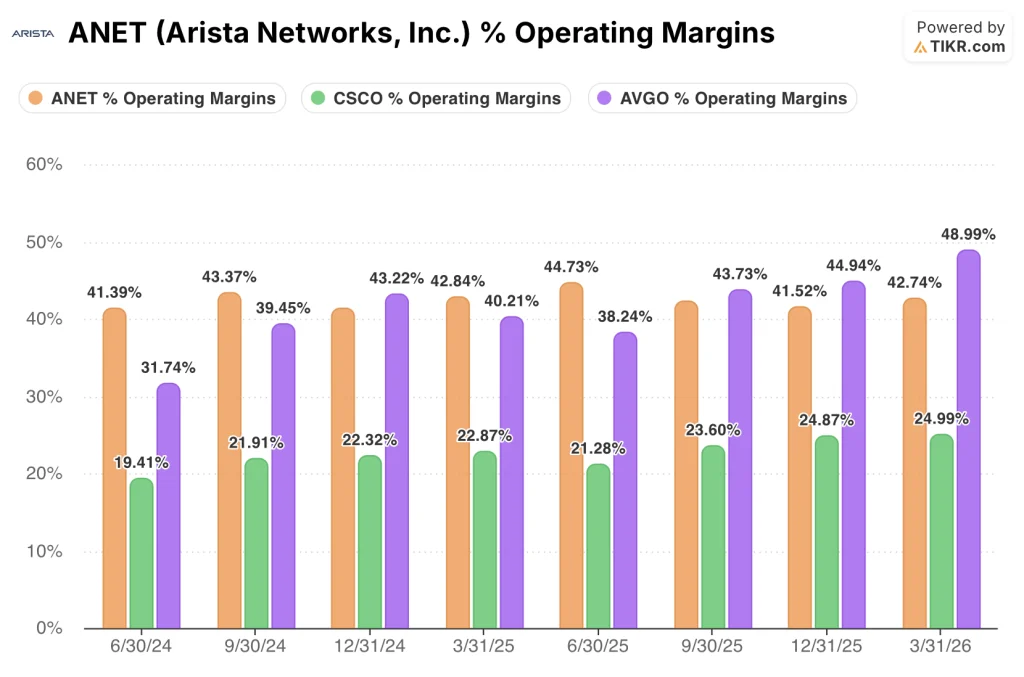

Arista Holds 43% Operating Margins as Broadcom Pulls Ahead and Cisco Stays Far Behind

Arista’s 43% operating margin in Q1 2026 has held in a tight band between 41% and 45% for eight consecutive quarters, a consistency no pure-play networking competitor can match at comparable growth rates.

Cisco (CSCO) ran a 25% operating margin in the most recent quarter, a level that has been essentially flat since 6/30/24, when it registered 19%, reflecting a business absorbing significant restructuring costs and a hardware-to-software transition that has yet to produce the margin profile Arista already operates at scale.

Broadcom (AVGO) reached 49% in Q1 2026, the highest reading across all three companies in the eight-quarter window, driven by a mix of semiconductor and infrastructure software revenue that carries structurally higher margins than Arista’s hardware-intensive networking business.

The more important comparison is directional: Broadcom’s operating margin has expanded from 32% in Q2 2024 to 49% in Q1 2026, a 17-point improvement over eight quarters, while Arista’s has stayed anchored near 43%, neither compressing nor expanding materially despite gross margin pressure from supply costs and customer mix.

Arista’s margin stability under cost pressure is the competitive signal the income statement is sending, and it is a different argument than Broadcom’s expansion or Cisco’s recovery.

TIKR’s $334 Target on Arista Networks Stock Requires Operating Leverage to Hold Through the Supply Cycle

TIKR’s model values Arista at approximately $334 by December 2030, implying around 105% total return from the current price of $163, or roughly 17% per year annualized.

That target is credible only if Arista sustains the operating leverage visible in Q1: total opex held flat sequentially while revenue grew, keeping operating margins at 43% despite gross margin compression, and the model’s durability depends on that discipline holding as supply costs normalize.

TIKR’s model shows the path to $334 — explore the full scenario breakdown and historical margin data on TIKR for free. Explore Arista Networks Stock’s Valuation Model and Historical Financials on TIKR for Free →

Should You Invest in Arista Networks, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Arista Networks stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arista Networks alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ANET stock on TIKR for Free →

What did Arista say about supply chain constraints in 2026?

Ullal told analysts that demand is outstripping supply across wafers, silicon, CPUs, optics, and memory, and called the shortage a “one or two year industry problem” that will weigh on gross margins as Arista absorbs elevated component costs.