Key Stats for Dell Technologies Inc.

- 52-Week Range: $110.22 – $469.47

- Current Price: $395.57

- Street Mean Target: ~$484

- Market Cap: ~$256 billion

- LTM Net Debt: ~$20 billion

- LTM Gross Margin: 19.2%

- Fwd 2-Yr Revenue CAGR: ~29%

- Fwd 2-Yr EPS CAGR: ~43%

- Dividend Yield: 0.6%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Dell Has Essentially Become an AI Infrastructure Company

Not long ago, Dell (DELL) was a reliable but unexciting business, a mature PC and server vendor grinding out modest revenue in a commoditized industry. The AI infrastructure wave has changed that entirely.

In the first quarter of fiscal 2027 (ended May 1, 2026), Dell reported $43.8 billion in revenue, up 88% year over year. The driver was not the PC business or conventional servers, it was AI-optimized servers, a category that barely existed in Dell’s revenue mix two years ago. That segment generated $16.1 billion in a single quarter, a 757% increase year over year, and the company booked $24.4 billion in new AI orders on top of that. The backlog for AI servers alone now stands at $51.3 billion.

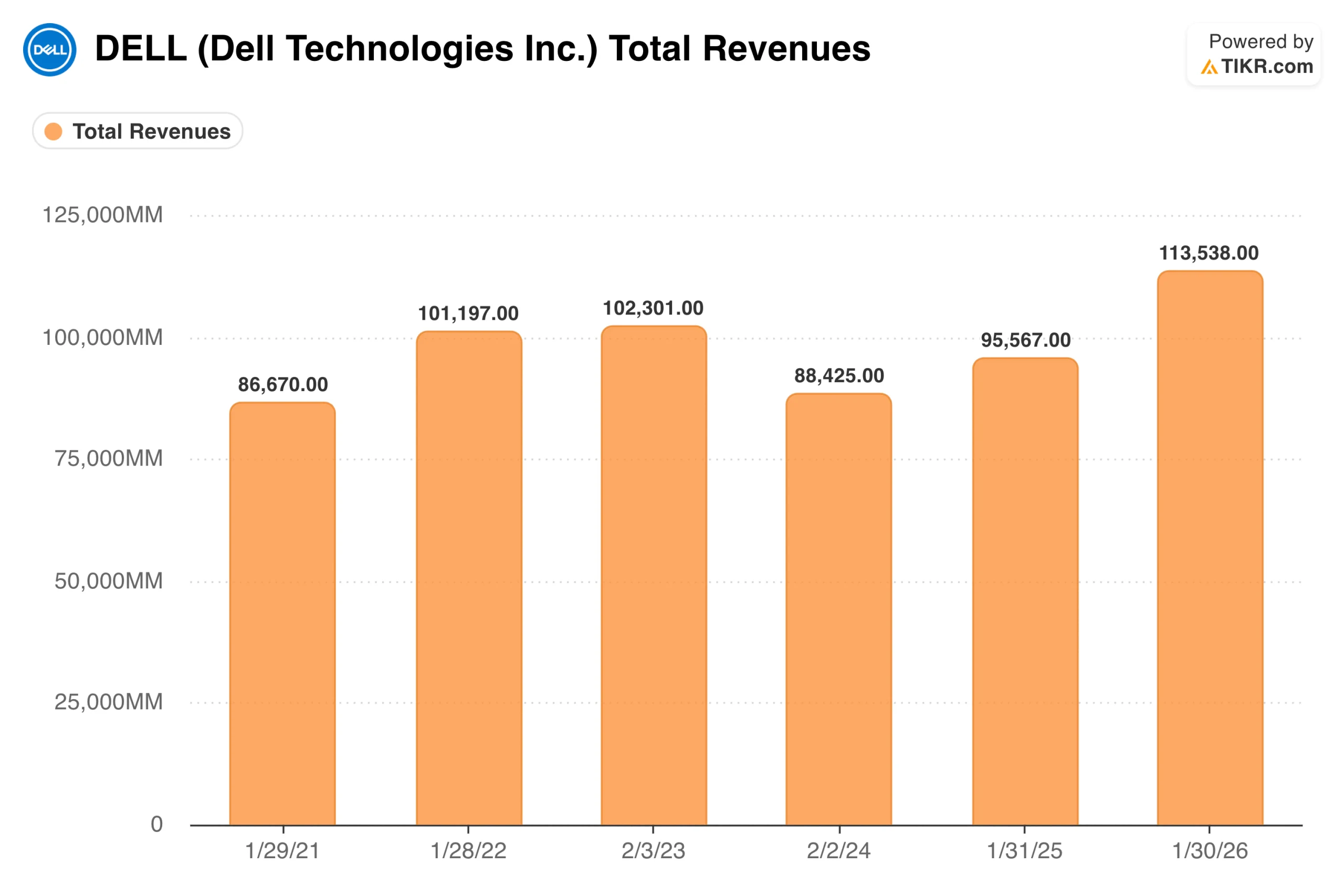

The revenue chart through fiscal 2026 tells the story of a company that spent years going nowhere, with revenues oscillating between roughly $88 billion and $113 billion with no clear direction.

What it doesn’t show yet is where the business is heading: management raised full-year FY27 guidance to a midpoint of $167 billion, meaning the bar on that chart nearly doubles in a single year. COO Jeff Clarke put it plainly on the earnings call: “The AI opportunity shows no signs of slowing.”

The traditional businesses are contributing too. Conventional server and networking revenue grew 92% as enterprises refresh aging fleets, commercial PC revenue grew 18% for its seventh consecutive quarter of growth, and storage grew 8%. This is broad-based acceleration, not a single product line carrying everything else.

Value Dell Technologies instantly (Free with TIKR) >>>

Earnings Are Soaring, But the Margin Story Is More Complicated

The earnings transformation is striking. Normalized EPS sat between $6 and $8 for most of the prior decade. Consensus now puts it at around $18 for the current fiscal year, with estimates extending to nearly $40 by fiscal 2031.

The complication is that AI servers are high-volume, lower-margin products compared to traditional servers or storage. Gross margin fell from 21% to 18% year over year as the AI mix dominated the quarter, and the trend is not changing as long as AI servers continue to grow as a share of revenue.

Dell’s Infrastructure Solutions Group operates at around a 10.5% operating margin, which is respectable for a hardware business but well below what investors in high-multiple tech companies typically expect.

The reason EPS can grow so dramatically despite margin compression is scale. When revenue nearly doubles, earnings grow even if percentage margins shrink, because fixed costs are absorbed over a much larger base.

Dell also generated $4.1 billion in operating cash flow in the quarter and returned $2.1 billion to shareholders through buybacks and dividends. The earnings power is real, it just lives inside a different kind of business than many of the other AI names investors have been reaching for.

See analysts’ growth forecasts and price targets for Dell Technologies (It’s free) >>>

What TIKR’s Model Says About the Stock at $395

The valuation model clearly frames the return scenario. At current prices, the mid-case target is around $530, implying roughly a 34% total return over the next four and a half years, or about 7% annualized. The bull case points toward around $750 at just under 8% per year. The bear case lands near $460, implying less than 2% annually.

The mid-case return is driven by a combination of earnings growth and modest multiple expansion rather than earnings alone, which means the scenario depends on the P/E holding up as earnings scale, not just the fundamentals improving.

The mid-case assumptions themselves are not heroic: around 10% annual revenue growth and roughly 13% annual EPS growth from here. Given Dell just grew revenue 88% in a single quarter, the model is pricing in significant deceleration from current levels, which is a reasonable base case as the AI server cycle matures. The scenario range skews clearly to the upside, the distance from the current price to the bull case is nearly double the distance to the bear case.

What the 7% annualized mid-case return tells you is that the stock has already absorbed a substantial amount of the good news. Up 209% year-to-date, with the street at a mean target of around $484, this is a situation the market hasn’t noticed at Dell.

What the Bulls Are Betting On

- The AI infrastructure cycle has years of runway left. Enterprise customers are still in early stages of AI deployment, and management described its pipeline as multiple backlogs across every vertical, with visibility extending well beyond the current fiscal year.

- Consensus estimates may prove too conservative. Dell beat Q1 estimates by a wide margin and raised guidance by $27 billion ninety days after issuing it. If demand holds, the EPS trajectory on the chart could look understated in hindsight.

- Traditional businesses provide a durable floor. A server refresh cycle in early innings and seven consecutive quarters of commercial PC growth suggest the AI server business is genuinely additive.

- The balance sheet supports continued capital returns. Dell returned $2.1 billion to shareholders in a single quarter and carries manageable leverage at around 1.4x net debt to EBITDA.

What the Bears Are Watching

- Margin compression has room to run. As AI servers grow from roughly 37% of infrastructure revenue to an even larger share, the overall margin profile continues to drift lower. The question is whether volume can permanently outpace the decline in margins.

- Most of the easy returns have already been captured. Up 209% year-to-date, the TIKR model’s mid-case of around 7% annualized is not the kind of return that tends to attract aggressive new capital.

- Supply constraints create execution risk. Management expects to exit the year with a meaningful AI backlog on the books because demand is outpacing component availability, particularly memory. Any supply disruption could delay revenue recognition.

- Hardware cycles eventually turn. Dell’s own history includes sharp revenue compression, revenues fell from $101 billion to $88 billion between fiscal 2022 and 2024. When enterprise AI spending moderates, Dell will feel it quickly.

See analysts’ growth forecasts and price targets for Dell stock (It’s free!) >>>

Should You Invest in Dell Technologies

The business is performing at a level genuinely unusual for a company of this size and maturity. The demand signals are strong, and the earnings power is growing meaningfully.

But the TIKR model points to mid-single-digit annualized returns in the base case, and the stock has already reflected most of the transformation. This is a name where the business is easier to admire than the entry point.

Use TIKR to track Dell’s revenue, margins, and EPS trajectory every quarter alongside every other stock on your radar. No credit card required.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!