Key Stats for RTX Stock

- Current Price: $183.53 (June 12, 2026 close)

- Target Price (Mid, Dec. 2030): ~$218

- Street Target: ~$216

- Potential Total Return: ~19% (through Dec. 2030)

- Annualized IRR: ~4% / year

- Max Drawdown: 19.32% on May 15, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

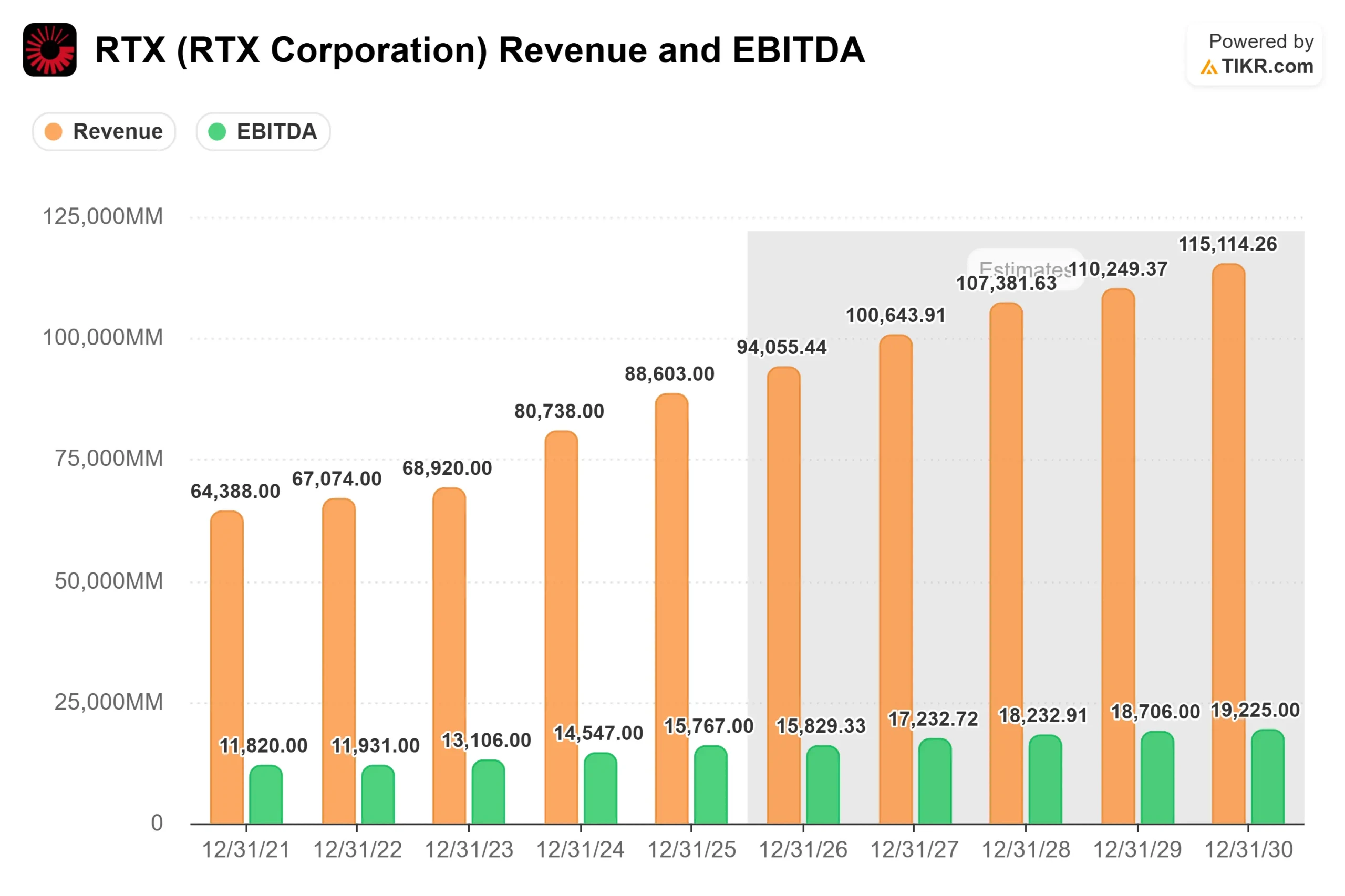

RTX Corporation (RTX) is a strange kind of cheap. The company behind Pratt & Whitney engines, Collins Aerospace systems, and Raytheon missiles and radars closed at $183.53 on June 12, around 14% below its 52-week high of $214.50, yet it holds the largest order book in its history. Demand has rarely looked stronger, but the market is pricing execution risk, not demand risk.

At the Bernstein Strategic Decisions Conference on May 29, CEO Chris Calio kept returning to one word. “Our focus continues to be on execution,” he said, framing a record $271 billion backlog as a promise the company still has to deliver on. That is the shift for RTX stock: the bull case no longer hinges on winning work. It hinges on building it.

Proof of the ramp arrived days later. On June 3, Raytheon won a $515 million follow-on U.S. Navy contract for its SPY-6 family of radars, the Navy’s most advanced maritime sensor. Naval Power president Barbara Borgonovi said an $800 million facility investment would let RTX “double SPY-6 output by 2028.” The stock has since firmed, rising around 4% on June 11 as a run of contract wins and an analyst upgrade reminded investors what the backlog is made of.

Why a Record Backlog Is Also a Production Test

The number investors cite is $271 billion. What gets missed is that it understates committed demand. Calio was explicit that the five framework agreements with the Department of War, covering Tomahawk, AMRAAM, and the Standard Missile family, sit outside it. “Those aren’t even in the $271 billion backlog,” he said. “That’s on the top.”

That is bullish and a warning at once. The agreements rest on seven-year firm demand and imply production rates Calio pegged at “anywhere from 2 to 4x the rates that we’re at today.” Quadrupling output is a manufacturing problem, and RTX has been candid that its supply chain is the constraint. Calio named the choke points directly: rocket motors, castings, and microelectronics. He called rocket motors “a constrained value stream” and said RTX is bringing in players like Avio and Nammo to expand domestic capacity.

This is the part the headline numbers gloss over. Management is not worried about orders. It is worried about whether the industrial base can scale to fill them, which is why RTX is spending roughly $10 billion this year on R&D and capital expenditure, much of it on automation and capacity.

See historical and forward estimates for RTX stock (It’s free!) >>>

The GTF Recovery Is Turning a Liability Into a Tailwind

The other execution story sits inside Pratt & Whitney. The geared turbofan (GTF), Pratt’s narrow-body engine, triggered a costly inspection program after a 2023 powder-metal defect, and the aircraft-on-ground (AOG) count, meaning jets parked waiting for engines, became the biggest overhang on the stock. At Bernstein, Calio said it is lifting. AOGs fell 15% in the first quarter from the end of 2025, on maintenance, repair, and overhaul (MRO) output up 23% year over year, with turnaround time down 20% on heavier workloads.

That recovery pays off in margin. Pratt’s commercial aftermarket grew 19% year over year in Q1, and the older but highly profitable V2500 engine is seeing extended demand as GTF jets cycle through shops. The aftermarket is the high-margin half of the engine business, so every AOG returning to service is both a customer win and a profit lever.

The risk is real, though. High jet fuel prices tied to the Iran conflict have squeezed airline cash flows. Calio said RTX has “not seen any change in buying patterns” yet, but flagged that discretionary work at Collins, like avionics upgrades and cabin interiors, would slip first if airline stress deepens.

Where RTX Trades Against Its Peers

On a forward EV/EBITDA basis, RTX trades at around 17.6x. That sits below diversified industrial GE near 29.7x and aerospace supplier Howmet around 33.4x, but above pure defense primes like Lockheed Martin near 12.4x and General Dynamics around 15.2x. The split fits the business: RTX is half commercial aerospace and half defense, so it earns a premium to the slower-growing primes and a discount to the highest-growth suppliers. Whether that premium holds depends on the same execution question the backlog raises.

See how RTX performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $183.53

- Target Price (Mid): ~$218

- Potential Total Return: ~19%

- Annualized IRR: ~4% / year

See analysts’ growth forecasts and price targets for RTX stock (It’s free!) >>>

TIKR’s mid-case, realized on December 31, 2030, values RTX at around $218, around 19% above today’s price, or roughly 4% annualized. Two revenue drivers anchor it: defense, where Calio said Raytheon’s trailing book-to-bill ran 1.5x and 48% of its backlog is higher-margin international work, and commercial aftermarket, where the GTF recovery and V2500 fleet feed Pratt’s most profitable revenue. The margin driver is Raytheon’s shift toward mature, high-volume radar and effector production, which Calio called “ripe for continued increases in productivity.” The primary risk is supply-chain throughput: if rocket motors, castings, or microelectronics cannot scale to the framework-agreement rates, the revenue ramp slips and margins stall. Upside comes if the GTF fleet plan finishes on schedule and Raytheon margins keep climbing past the roughly 12% Calio cited last quarter. The downside is slower margin expansion, plus a commercial aftermarket dragged by airline stress.

Conclusion

Watch RTX’s Q2 2026 earnings, expected in late July. The line that matters most is the GTF AOG count. Calio said the decline continued into Q2, so another double-digit drop plus 20%-plus MRO growth would confirm the execution thesis. A flattening AOG curve, or any sign supply-chain constraints are capping output, would be the warning: it would mean the $271 billion backlog is converting to revenue slower than the valuation assumes. The order book is no longer the question. The factory is.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in RTX?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up RTX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track RTX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!