Key Stats for Comcast Stock

- Current Price: $24.50

- Target Price (Mid): ~$42

- Street Target: ~$32

- Potential Total Return: ~71%

- Annualized IRR: ~13% / year

- Earnings Reaction: -12.90% (Q1 2026, reported April 23, 2026)

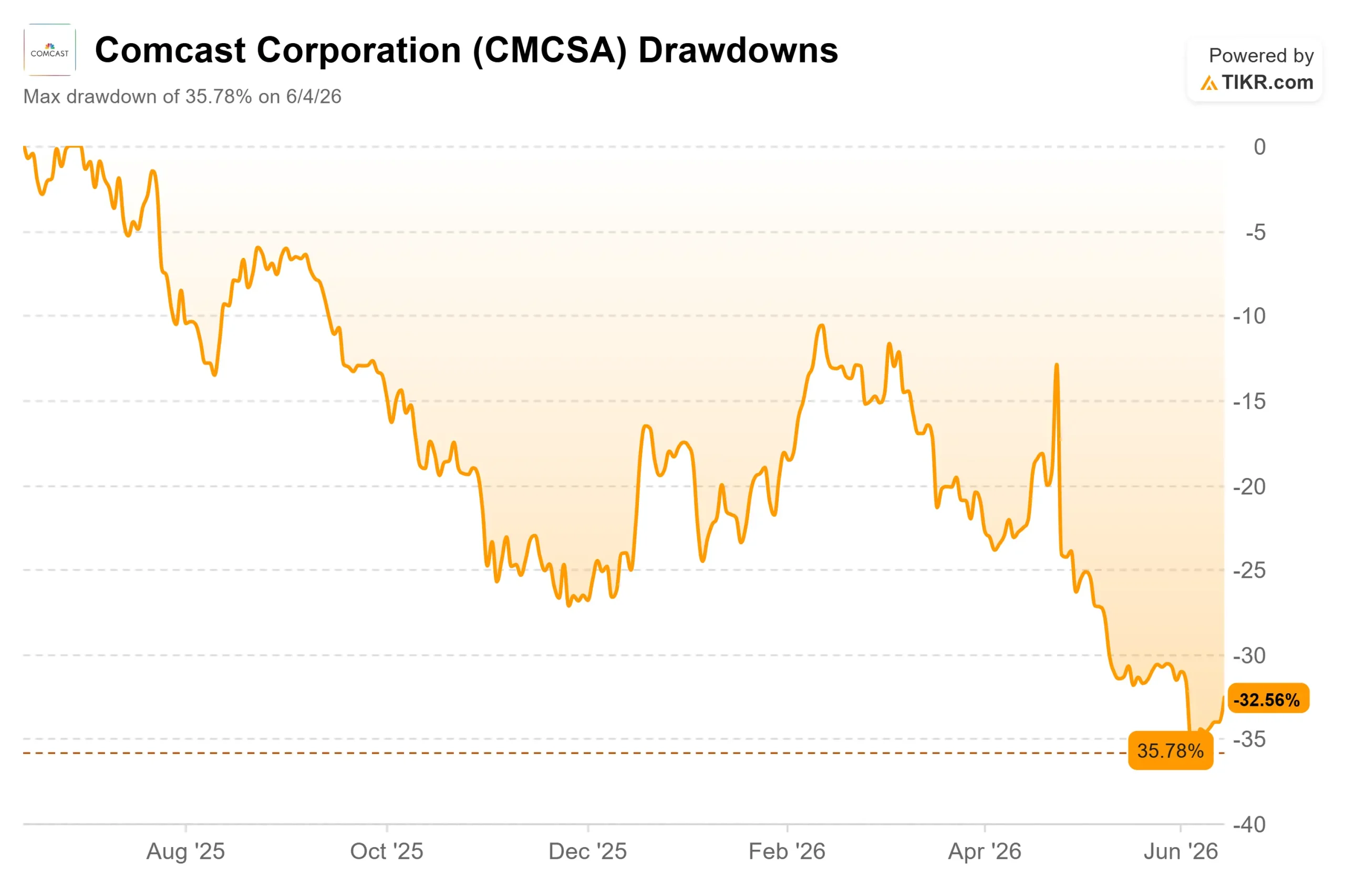

- Max Drawdown: -35.78% (June 4, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Comcast Corporation (CMCSA) trades like a business the market has written off. The stock sits at $24.50, down about 33% from its 52-week high of $36.66 and just above its low of $23.13. The fear is real: broadband subscribers keep leaving, and Peacock has lost money since it launched.

So when the executive who runs NBCUniversal’s media group said Peacock will turn its first profit this quarter, it cut against everything the share price implies. That is the tension. Bears see a shrinking cable business funding a money-losing streamer. Bulls see a company close to proving the opposite. The market cannot yet tell which is true.

The Most Definitive Thing Comcast Has Said About Peacock Yet

At the 2026 Evercore Global TMT Conference on June 2, Matt Strauss, Chairman of NBCUniversal Media Group, did not hedge. “I’m proud to share we will be profitable in Q2,” he said, calling it “a beginning to a validation of the strategy.”

That matters because of the shift in tone. On the Q1 call in April, management only said Peacock was expected to “approach profitability.” Moving from “approach” to “will be” is the most relevant data point of the quarter for a stock priced for permanent losses.

The market gave it little credit. CMCSA fell 5.41% on June 3, the day after the conference, trading near its low rather than rallying. Investors want the print, not the promise.

See historical and forward estimates for Comcast stock (It’s free!) >>>

Why The Q1 Loss Was Misleading

Peacock lost $432 million in EBITDA in Q1, a wider loss than a year earlier. The cause was timing, not a worsening business: Comcast straight-lines its new NBA rights cost, and roughly half of Peacock’s NBA games fell in the January-to-March window. That load eases sharply from here, which underpins the Q2 call. Peacock revenue still reached about $2 billion in Q1, up around 71% year-over-year, lifted by what NBCUniversal branded “Legendary February”: the Winter Olympics, the Super Bowl, and the NBA All-Star Game within a 17-day window that Strauss said drew over 225 million viewers.

The Engagement Pivot Bears Are Underrating

The most important part of Strauss’s appearance got the least coverage. NBCUniversal is rebuilding Peacock from a streaming service into what he calls a participatory entertainment platform, and the engagement data is concrete.

Bravo viewers on Peacock have around 33% lower churn and watch roughly 75 episodes a month, Strauss said, calling them “content carnivores.” Since churn is the weak point of any subscription business, a fandom that is loyal is a margin asset. The company is also adding vertical video, in-app games, and interactive NBA features. During the Winter Olympics, 20% of viewers who used vertical video went on to watch long-form content or live; for the NBA, that figure was 25%.

There is a connectivity tie-in, too. Strauss said Peacock’s 46 million subscribers equal roughly 100 million monthly active users, and Comcast can now identify which sit inside its broadband footprint and target them directly. That links the media turnaround to the broadband problem, driving the stock down.

Where The Real Pressure Still Sits

None of these fixes the core issue overnight. Comcast lost 65,000 broadband subscribers in Q1, though net losses improved by more than 100,000 year-over-year, the first such improvement since 2020. The stock’s 12.90% drop after a Q1 report that beat on revenue, EPS, and EBITDA shows the market is trading the broadband story, not the headline numbers.

Analysts stay cautious: 6 Buys, 1 Outperform, 17 Holds, 1 Underperform, and 2 Sells, with a Street target around $32. The valuation gap to peers is stark. Comcast trades at an NTM EV/EBITDA near 5.2x and a forward P/E around 7x, against a telecom peer median P/E near 11x, with Verizon and AT&T both around 10x. That discount prices in cable’s decline but give almost no credit for the media portfolio, wireless growth, or a 5.5% dividend yield. Whether it is justified hinges on one question: does broadband stabilize before the multiple has to re-rate?

See how Comcast performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $24.50

- Target Price (Mid): ~$42

- Potential Total Return: ~71%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Comcast stock (It’s free!) >>>

Using TIKR’s mid-case scenario, realized at the end of 2030, the model points to a target of around $42, a total return near 71%, and an annualized return of around 13% over the next 4.5 years. The mid case assumes stabilization, not a heroic recovery, which fits a stock priced for decline.

The two revenue drivers are modest broadband and wireless growth, offsetting cable video erosion, and continued advertising and subscription scaling at Peacock. The margin driver is Peacock moving into the black, which removes a large quarterly drag on free cash flow. The primary risk is broadband: if fixed-wireless and fiber overbuild speed up subscriber losses, no streaming win offsets it.

The upside: broadband losses keep narrowing while Peacock profitability compounds, and the compressed forward multiple re-rates higher. The downside: cable attrition accelerates, pricing resets pressure revenue, and the multiple stays low.

Conclusion

The thesis lives or dies on one number. Watch Comcast’s Q2 2026 earnings, due in late July, for Peacock segment EBITDA. Management says it will be positive. A profit, even a thin one, would convert a six-year liability into a contributor and give the case for a cheap multiple real teeth. A slip back into the red after such a definitive call would vindicate the skeptics and likely retest the lows. Good looks like Peacock in the black with broadband losses still narrowing; bad looks like a streaming miss paired with worse attrition. Late July tells you which one you are holding.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Comcast?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Comcast, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Comcast alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Comcast on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!