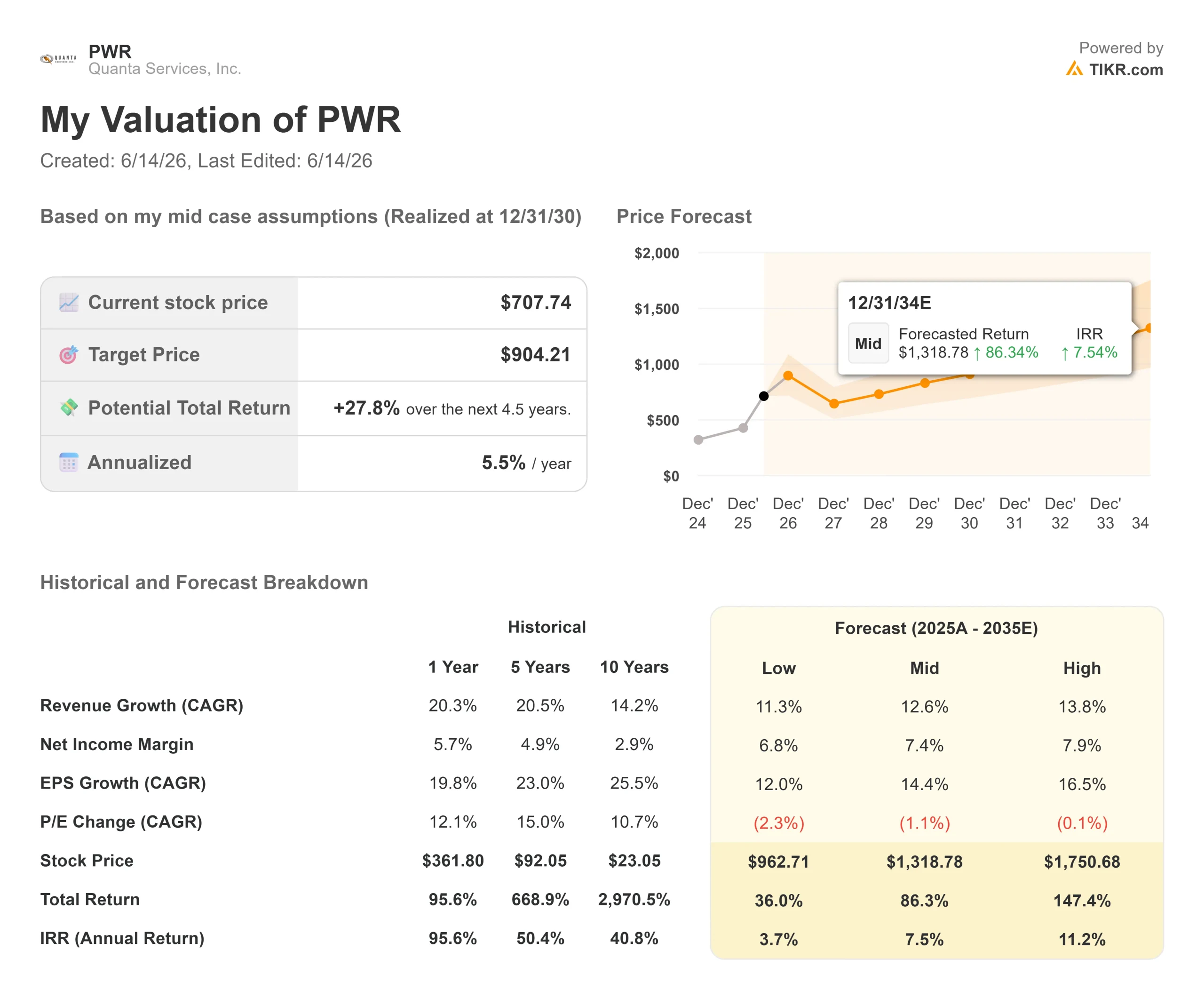

Key Stats for Quanta Services Stock

- Current Price: $707.74

- Target Price (Mid): ~$900

- Street Target: ~$760

- Potential Total Return: ~28%

- Annualized IRR: ~6% / year

- Earnings Reaction: +1.98% (April 30, 2026)

- Max Drawdown (1-yr): 17.11% (June 10, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Quanta Services (PWR) is the rare stock where nearly everyone agrees the demand is real, and no one agrees on the price. Shares closed at $707.74 on June 12, up 3.58% on the day, yet still roughly 10% below the 52-week high of $788.75. In between, the company posted a record backlog, the CEO sold stock near the top, and the multiple stayed close to 49 times forward earnings. That is the tension right now: a business compounding faster than ever, priced as if the market has already seen the next decade.

What changed the conversation was not the quarter. It was what CEO Earl “Duke” Austin said about time.

Management Reframed the Timeline

At the Bernstein Strategic Decisions Conference on May 28, Austin pushed back on the idea that this cycle peaks at the end of the decade. “I don’t know why we put 2030 as the time frame, everything stops in 2030, the world is going to end,” he said, before adding the buildout is “still moving forward, like well past 2030.” His point was mechanical. Order a combined-cycle gas plant today, and the turbine alone takes over 30 months, with the full build pushing about five years out. Orders booked next quarter are 2031 revenue and beyond.

That matters because the bear case leans on duration. Pay a premium multiple, and you need the growth to last longer than the market prices. Austin’s argument is that the contracted work has barely started to flow. He said the company has “not seen the big project stack on it yet,” and expects larger transmission programs to begin construction in 2027 with five to seven-year build cycles.

CFO Jayshree Desai added the capital signal. She said utility multiyear budgets that grew 8% to 9% annually not long ago are now being revised up more than 20%, with the customer question shifting from “if” to “when.” Because Quanta self-performs about 85% of its work, that budget acceleration converts fairly directly into revenue.

The Numbers Underneath the Story

The fundamentals back the urgency. Per TIKR data, Q1 2026 revenue was $7,874.79 million, up 26.3% year over year, with adjusted EPS of $2.68, beating consensus by about 32%. The company reported a record backlog of $48.5 billion, up from $44 billion at year-end 2025, and raised full-year 2026 guidance to revenue of $34.7 billion to $35.2 billion and adjusted EPS of $13.55 to $14.25.

The catch sits between the top and bottom lines. Gross margin held around 15% while EBIT margin ran at 5.6%, a gap shaped by the construction model and the costs that come with steady acquisitions. Margin expansion is the lever bulls want, and the one management is most measured about. Asked directly, Austin said Quanta would “increase margins a little bit,” but framed the real engine as compounding earnings over time.

There is also a signal investors cannot ignore. In early May, near the 52-week high, Austin sold 130,000 shares at an average of $770.65, part of a larger disposal that week. Insider sales are not always bearish, and Austin still directly owns more than half a million shares. But selling into strength ahead of a pullback feeds the “priced for perfection” worry.

That worry shows up in the multiple. PWR trades at an NTM EV/EBITDA of 30.55x versus a peer mean near 16x. Comfort Systems (FIX) and Sterling Infrastructure (STRL) sit near 30x too, but EMCOR (EME) at 18x and MasTec (MTZ) at 20x show the premium is real. Austin’s defense is that scale and craft labor build a competitive moat that rivals cannot buy quickly, noting Quanta has invested heavily in training journeymen since 2009. Whether that justifies nearly double the peer multiple is the unresolved question.

See historical and forward estimates for Quanta Services stock (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $707.74

- Target Price (Mid): ~$900

- Potential Total Return: ~28%

- Annualized IRR: ~6% / year

See analysts’ growth forecasts and price targets for Quanta Services stock (It’s free!) >>>

The TIKR mid-case points to a target of around $900 realized at year-end 2030, an implied total return near 28% and about 6% annualized. The two revenue drivers are utility transmission and distribution spending, where budgets are accelerating past 20%, and large-load demand from data centers and reshoring that has barely begun converting. The margin driver is mixed, as higher-value transmission and the transformer supply chain lift the project profile.

The case assumes around 13% revenue CAGR and a net margin near 7%. Upside: if the 765kV transmission backbone and gas generation stack on as management expects, growth runs longer and margins inch higher. Downside: the multiple already prices much of this in, so any margin slip or slower order pace could compress the valuation faster than earnings can catch up.

Conclusion

Watch whether contracted demand shows up as margin, not just revenue. Austin says the biggest transmission and gas programs begin construction in 2027, but the operating margin line decides whether PWR grows into its multiple or stalls. The next read is Q2 2026 earnings on July 30. “Good” looks like double-digit revenue growth with operating margin pushing back toward the 7% level seen in late 2025; “bad” is revenue strength paired with flat or compressing margins, which would validate the bears. Watch the margin line, not the backlog headline.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Quanta Services?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Quanta Services, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Quanta Services alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Quanta Services on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!