Key Stats for NVIDIA Stock

- Current Price: $205.19 (June 12, 2026 close)

- Target Price (Mid): ~$530

- Street Target: ~$299

- Potential Total Return: ~158%

- Annualized IRR: ~23% / year

- Earnings Reaction: -5.46% (February 25, 2026)

- Max Drawdown: -20.22% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

NVIDIA (NVDA) just did something a company growing revenue 85% a year almost never does. Alongside its May 20 earnings, the board raised the quarterly dividend from $0.01 to $0.25 a share, a 25-fold increase, and authorized an additional $80 billion in share repurchases with no expiration date, according to NVIDIA’s investor relations materials.

Here is the tension. Hypergrowth companies hoard cash because reinvestment compounds faster than any dividend. Mature companies return cash because they have run out of better ideas. NVIDIA is doing both at once, and the market cannot decide what to make of it. The stock closed at $205.19, still about 13% below its 52-week high of $236.54, even as the business prints records.

The real question is what management is telling you when a business this fast-growing starts writing checks to shareholders.

A record quarter, the market shrugged at

The capital return did not come from a soft patch. NVIDIA reported fiscal Q1 2027 revenue of $81.6 billion, up 85% year over year, with data center revenue of $75.2 billion, up 92%, per its earnings release. Adjusted EPS of $1.87 beat the Street’s $1.77 by 5.54%, extending an unbroken streak of beats. Management guided Q2 revenue to around $91 billion, above the roughly $87 billion consensus.

The reaction to the prior quarter tells the story. After the February 25 report, NVDA fell 5.46% the next session despite beating. That gap between operational fireworks and a flat stock has defined the NVDA trade. When shares are priced for near-perfection, a beat is the cost of admission.

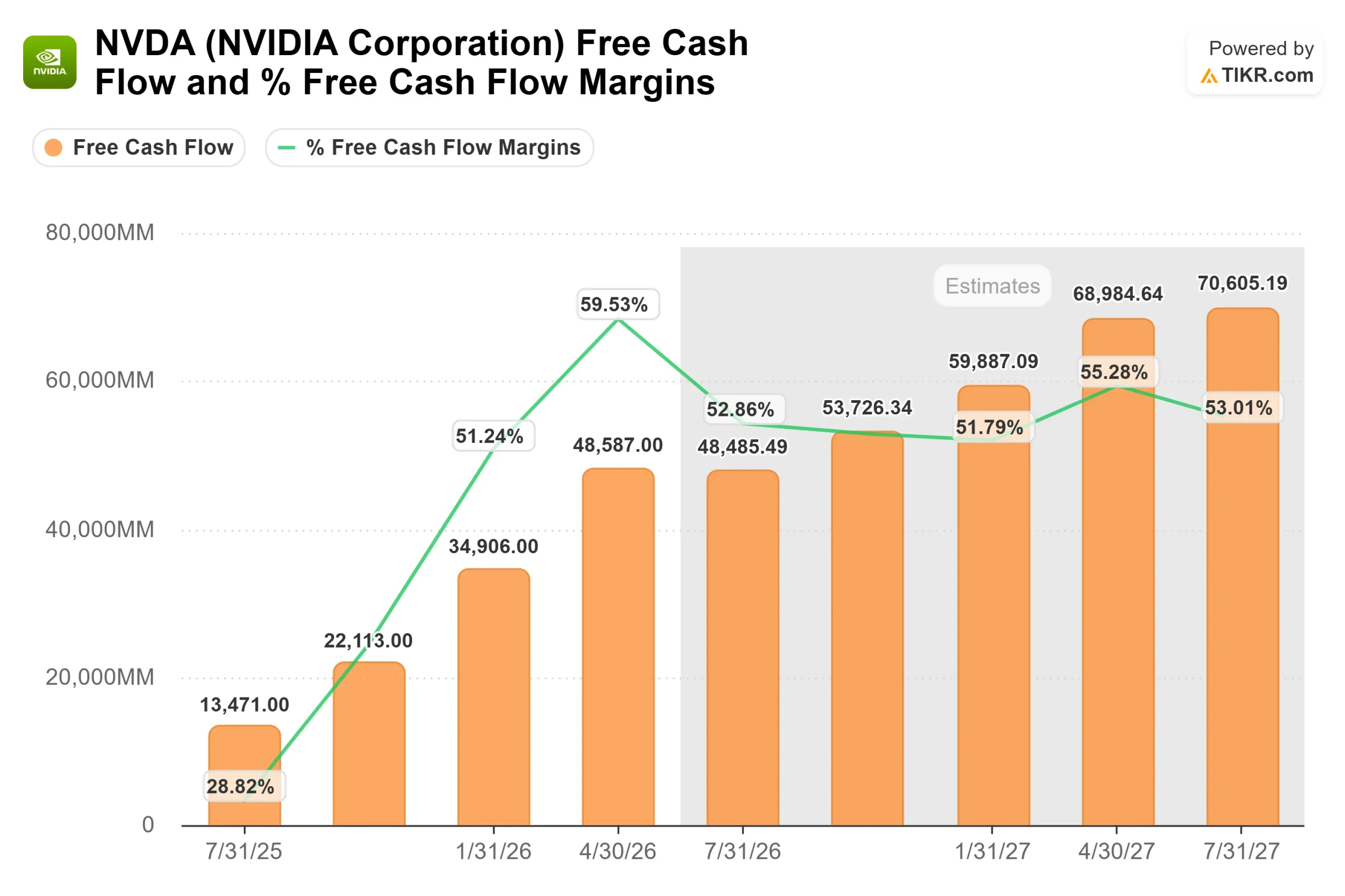

That backdrop is what the capital program speaks to. NVIDIA generated free cash flow of $96.7 billion in fiscal 2026, and Q1 alone produced $48.6 billion, nearly double the year-ago figure. CFO Colette Kress said the company intends to return at least half of that to shareholders, framing it as durable: the ability to return “50% or more absolutely is a key focus of ours, not just for today, not just for tomorrow, but for the long term.”

See historical and forward estimates for NVIDIA stock (It’s free!) >>>

Why the buyback signals more than the dividend

The yield is still small at around 0.5%, so the income is not the point. What matters is what the buyback implies about valuation in management’s own eyes. The new $80 billion stacks on roughly $38.5 billion already remaining, giving NVIDIA about $118 billion of repurchasing power. Companies do not commit that much to their own stock unless they think it is worth more than the market is paying.

That confidence rests on a demand base that has broadened. Kress pointed to what NVIDIA calls ACIE (AI Cloud Infrastructure and Enterprises, the newly built AI clouds and national AI factories, rather than repurposed general-purpose clouds) as likely the fastest-growing part of the data center business. On the bear case that custom chips erode NVIDIA’s share, her answer was about software, not specs: a fixed chip “was determined at the point that they went and designed it… It doesn’t have the ability to change over that,” while NVIDIA’s platform evolves with each workload.

The Vera Rubin catalyst sitting in Q3

This is not a maturing business out of the runway. At GTC Taipei, NVIDIA confirmed its Vera Rubin platform had entered full production, and Kress made the timeline explicit: “it is coming soon. It’s ready for Q3.” That puts the ramp in the quarter ending October 2026, earlier than many investors expected. The new Vera CPU opens a fresh content line, built on NVIDIA’s own cores, running roughly 2x the performance of x86 alternatives by management’s account, and is sellable standalone.

NVIDIA’s premium is narrower than its reputation suggests. It trades at 16.43x NTM EV/EBITDA versus Broadcom at 19.53x, and at 20.65x forward earnings against AMD’s 58.68x. For the fastest grower in the group, with a 74.1% current gross margin and an LTM return on invested capital of 77.2%, the discount to slower peers reads more as relative value than warning.

The Street has moved with the fundamentals. The mean target rose from $268.61 in April to $298.93 in June, implying roughly 46% upside, with 49 Buys, 10 Outperforms, 2 Holds, and a single Sell. The risk over all of it is multiple compressions: NVDA carries the world’s largest market cap, and any wobble in hyperscaler spending or a prolonged China closure could reprice it fast.

See how NVIDIA performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

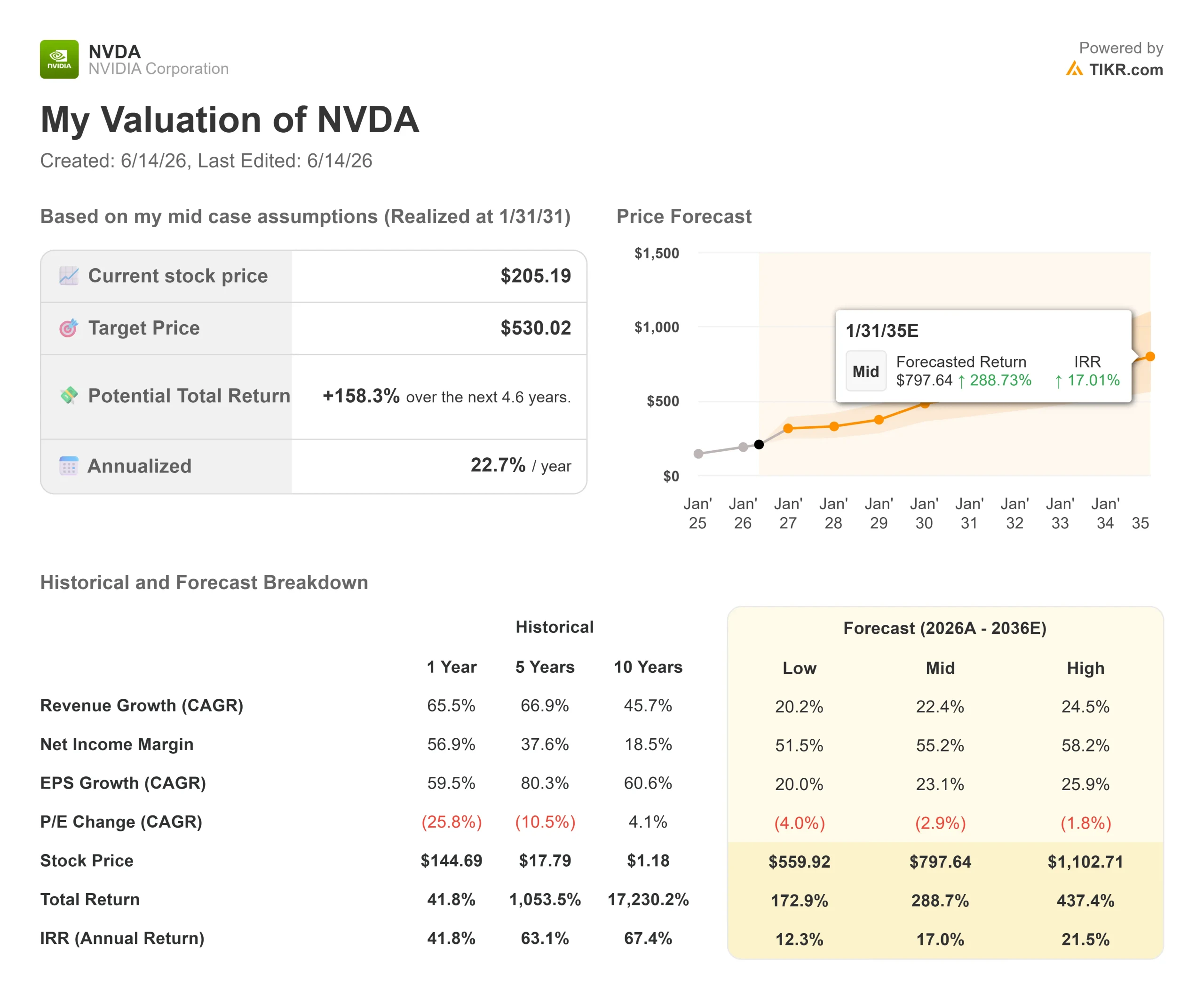

- Current Price: $205.19

- Target Price (Mid): ~$530

- Potential Total Return: ~158%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for NVIDIA stock (It’s free!) >>>

The TIKR mid-case, realized on January 31, 2031, values NVDA at around $530, a roughly 158% total return over 4.6 years and an annualized IRR of around 23%. The two revenue CAGR drivers are continued hyperscaler capital spending and the Vera Rubin ramp reaching enterprise, sovereign, and ACIE customers, supporting a mid-case revenue growth rate of around 22%. The margin driver is a data center operating leverage holding a net income margin of around 55%. The primary risk is multiple compressions, since the premium leaves little room for any growth disappointment.

The upside case: agentic compute demand stays vertical, and Vera Rubin ramps on schedule, pushing growth and margins to the high end. The downside case: hyperscaler spending normalizes, or custom silicon takes share faster than expected, compressing both the multiple and the growth rate.

Conclusion

Watch data center revenue in NVIDIA’s fiscal Q2 2027 report, expected in late August 2026. Management guided total revenue to around $91 billion. Hitting that, with data center comfortably above the $75.2 billion it just printed, confirms the demand Kress called “vertical” and that Vera Rubin is pulling forward. A miss, or any sign hyperscaler orders are cooling, hands the bears their first real evidence, and puts the premium at risk. The capital-return program tells you what management believes. August tells you whether the cash flow funding it keeps compounding.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!