Key Stats for Amazon Stock

- Current Price: $238.55 (June 12, 2026 close)

- Target Price (Mid): ~$607

- Street Target: ~$313

- Potential Total Return: ~155% (to year-end 2030)

- Annualized IRR: ~23% / year

- Earnings Reaction: +0.77% (April 29, 2026)

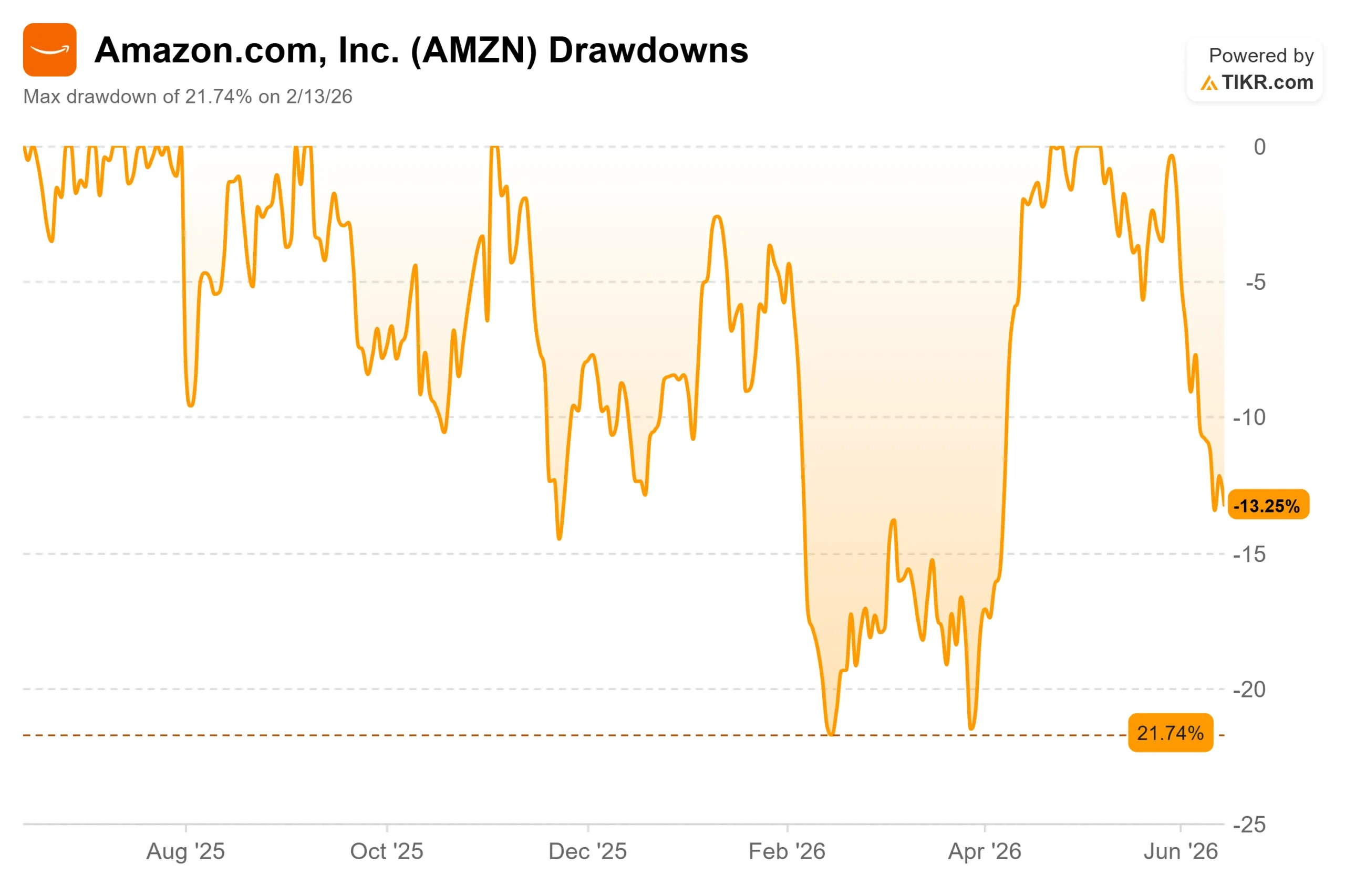

- Max Drawdown: 21.74% (February 13, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amazon (AMZN) just told investors its cloud business is growing faster than it has in nearly four years, and the market sold the stock anyway. Shares closed at $238.55 on June 12, down about 13% from the $278.56 high set in May and off roughly 6% in the past week. For the largest cloud provider on earth, that is a strange reaction to good news.

So here is the question investors are asking about Amazon stock in 2026: Is this weakness a warning or a window? The fundamentals are accelerating. The price is falling. Both cannot stay true forever.

The bull case is short. Amazon Web Services (AWS), the company’s cloud arm, grew 28% year over year last quarter, its fastest pace in 15 quarters, and its operating margin hit a record. The bear case is just as short: the company plans to spend around $200 billion this year, and the cash is increasingly coming from borrowing rather than profit.

The Selloff Is About One Number

Amazon is not falling because its business is weak. It is falling because investors are nervous about how it is paying for growth.

That nervousness got a fresh trigger this month. On June 8, Amazon secured a $17.5 billion term loan led by Citibank, per an SEC filing, days after selling C$14 billion (about $10 billion) in Canadian-dollar bonds, the largest corporate bond sale ever in that currency. The stock fell 1.2% on June 12 as the debt headlines stacked up.

For a company that has long funded itself from its own cash flow, leaning on debt reads as a signal. The $200 billion capital expenditure plan, meaning money spent on data centers, chips, and infrastructure, is now too large for operating cash alone to cover, and trailing free cash flow has compressed sharply.

CEO Andy Jassy has met the worry head-on. “We’ve been through this cycle with the first big AWS growth wave and like the results,” he told analysts, framing the spend as the same playbook that built AWS into what he called a $150 billion annual run-rate business.

See historical and forward estimates for Amazon stock (It’s free!) >>>

Why the Fundamentals Argue the Other Way

The first quarter is what the fear is fighting against. AWS revenue reached $37.6 billion, up 28% year over year. Total revenue was $181.5 billion, and the operating income of $23.9 billion delivered a record 13.1% margin. Adjusted earnings of $2.78 per share beat consensus by about 69%, the cleanest read on the quarter’s profitability.

The strength was broad. Advertising rose 22% to $17.2 billion, and units sold across the stores business grew 15%, the most since the tail end of the pandemic. The cash-generating segments are funding the one that needs it.

The chip business may be the most underrated piece. Amazon’s custom silicon now runs at over a $20 billion annual rate, growing triple digits year over year. Jassy said Trainium2, Amazon’s AI training chip, offers about 30% better price performance than comparable GPUs (the standard chips for AI work) and is largely sold out. “We now have over $225 billion in revenue commitments for Trainium,” he said. A backlog that size is hard to square with the idea that the AI spend is speculative.

Cheaper Than Its Own Recent Past

There is no clean public peer for a company that is at once a top US grocer, the largest cloud provider, and a top-three data center chip designer. So the fairer test is Amazon against its own history.

The stock trades at about 12 times forward EV/EBITDA, a measure of value against expected operating profit. That sits below the 12 to 14 times range it held across 2025. The market is paying less for each dollar of forward earnings power than it did a year ago, even as growth accelerated. That gap is the crux of the valuation question.

The risk runs the other way, too. If AI demand monetizes slower than management assumes, the capex weighs on free cash flow for longer, and the multiple never re-rates. Regulatory overhangs add to it, including a European Union cloud-procurement review and a US Federal Trade Commission antitrust trial set for October 2026.

See how Amazon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $238.55

- Target Price (Mid): ~$607

- Potential Total Return: ~155%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for Amazon stock (It’s free!) >>>

The TIKR Valuation Model’s mid case, realized at year-end 2030, puts AMZN around $607, an implied total return near 155%, and an annualized IRR (the yearly return from today’s price to the target) of about 23%. The mid case fits here because it sits between a Street that already expects upside and assumptions that do not require heroics.

Two revenue CAGR drivers carry the forecast: AWS expansion as the Trainium backlog converts to billed revenue, and advertising layered on the retail base. The margin driver is operating leverage, with net income margin widening toward 16% by 2030 from single digits historically, helped by fulfillment automation and cheaper in-house chips. The primary risk is the capex cycle itself.

The upside: Amazon compounds revenue in the low teens, margins expand, and the stock roughly doubles by 2030. The downside: the $200 billion spend keeps outrunning revenue, free cash flow stays thin, and the multiple stays marked down.

Conclusion

The next real test is Amazon’s Q2 earnings on July 30. Watch AWS growth above all: hold at or above 28%, and the reacceleration is a trend, not a blip. Slip toward the low 20s while spending climbs, and the bears were early but right. Watch free cash flow too. Management has set no floor, so the first sign that trailing free cash flow has stopped shrinking would be the clearest proof the spending is turning into returns. Until then, the stock is a wager on Jassy’s record against the market’s patience.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amazon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amazon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!