Key Stats for Alphabet Stock

- Current Price: $359.68

- Target Price (Mid): ~$635

- Street Target: ~$433

- Potential Total Return: ~77%

- Annualized IRR: ~13% / year

- Earnings Reaction: +9.96% (April 29, 2026)

- Max Drawdown: 20.42% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet Inc. (GOOGL) does not ask investors for money. For most of the last decade, the cash flowed the other way through buybacks. So when the company priced an $84.75 billion equity raise in early June, the market did a double-take. The stock fell roughly 5.5% on the week, closing near $359 on June 3, down from about $380 before the news.

The size is the headline: the largest equity capital raise in U.S. corporate history. But the name anchoring it matters more, as Berkshire Hathaway committed $10 billion to the deal. One of the most buyback-friendly companies on the planet is issuing stock, and one of the most famously tech-averse investors is buying it.

That is the tension. Bears see real dilution on top of a capital plan already squeezing free cash flow. Bulls see a company that would only raise this much equity if demand were running well ahead of supply. The unanswered question is whether the AI infrastructure being funded earns a return that makes the dilution a rounding error or a costly mistake.

What Alphabet Raised, and Why

The raise comes in three pieces. A $30 billion underwritten public offering covers roughly $18 billion in stock plus mandatory convertible preferred shares. A $40 billion at-the-market program will sell shares into the market over time, starting in Q3. And Berkshire’s $10 billion came through a private placement priced just below the public offering. The package was first announced at $80 billion, then upsized a day later after demand overran the original terms.

One detail reshapes the dilution story. The $40 billion at-the-market program, the largest piece, is earmarked mostly for covering taxes tied to employee stock awards, not the AI buildout. The money actually pointed at AI is the underwritten tranche plus Berkshire’s check.

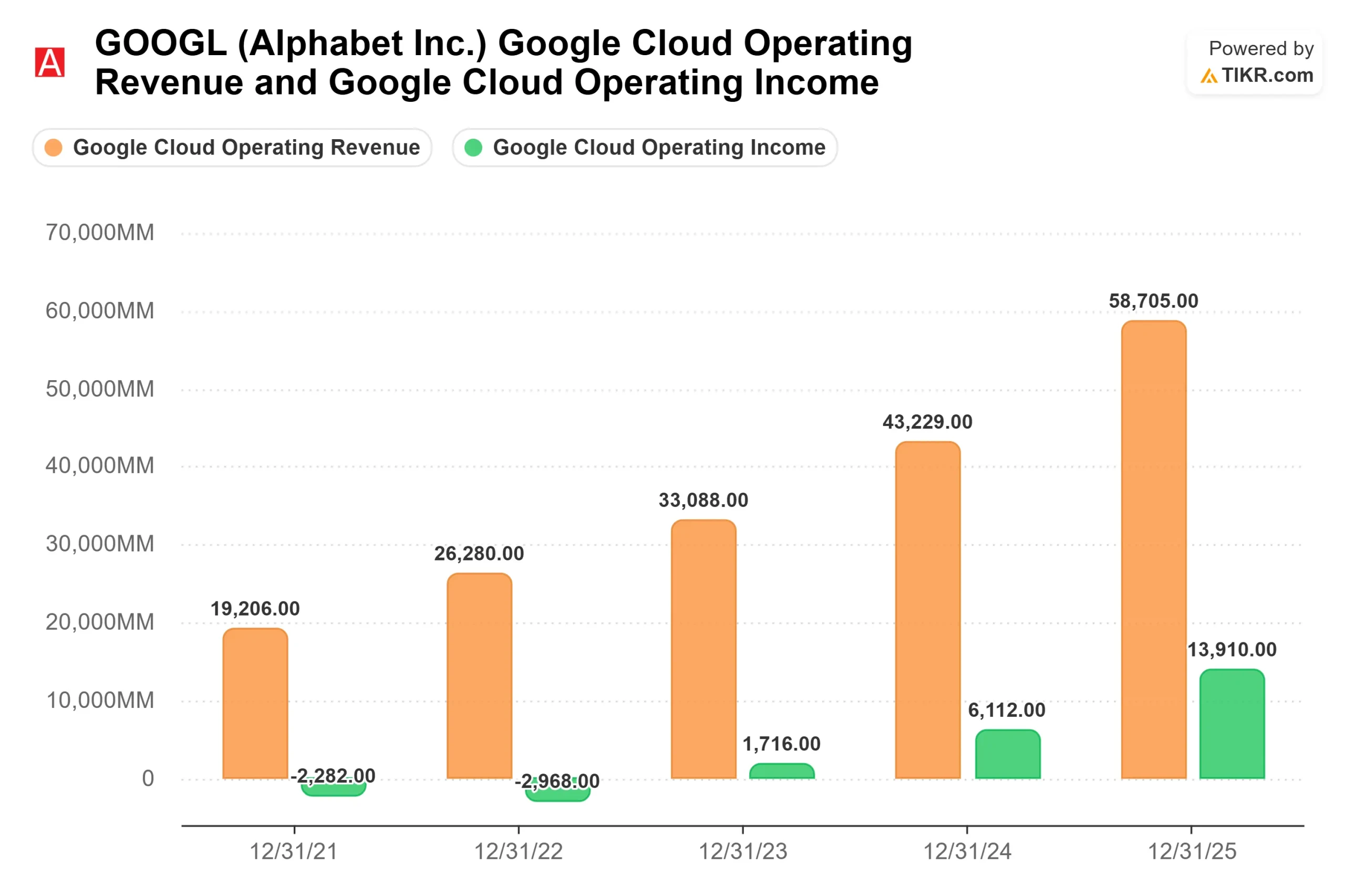

The spending traces to the earnings surprise Alphabet posted in Q1, when the stock jumped 9.96% the next session on $109.9 billion in revenue, up 22% year over year, with Google Cloud up 63%. On that call, CEO Sundar Pichai said the company is “compute constrained in the near term,” noting Cloud revenue “would have been higher if we were able to meet the demand.” Management then lifted 2026 capital spending guidance to $180 billion to $190 billion.

The Demand Signal Behind the Spend

At a June 3 special call, Pichai sharpened the point, saying demand for Alphabet’s AI products is “meaningfully exceeding our available supply.” A company does not raise record equity to chase demand it hopes to find. It raises it to serve the demand it has already booked.

The proof is the Cloud backlog, which Pichai said “nearly doubled quarter-on-quarter to over $460 billion,” with just over half expected to convert to revenue within 24 months. A cloud backlog is contracted customer commitments not yet booked as revenue. When it doubles in a quarter, customers are committing faster than the company can build to serve them. CFO Anat Ashkenazi tied the financing to “our relentless focus on ROIC,” the language of a company spending against contracted demand, not faith.

See historical and forward estimates for Alphabet stock (It’s free!) >>>

Is the Dilution Actually a Problem?

The bears have a fair point. Alphabet investors bought a capital-light cash machine with a clean balance sheet. The plan adds equity dilution on top of more than $100 billion in debt raised over the past year, and the free cash flow picture tightens fast. TIKR’s estimates show free cash flow margin falling to around 5% in 2026 from about 18% in 2025 as the spending lands. That compression is the real cost of the strategy.

The counterweight is that Alphabet is not raising this money out of need. It ended Q1 with $127 billion in cash and marketable securities and could fund much of the buildout internally. The equity raise accelerates the timeline rather than rescuing the balance sheet. And Berkshire is the tell. An investor known for avoiding capital-heavy tech bets does not write a $10 billion check into a dilution it expects to regret.

Valuation frames the rest. At $359.68, GOOGL trades at around 18x NTM EV/EBITDA and around 29x forward earnings. On TIKR’s Competitors page, Meta sits near 9.5x NTM EV/EBITDA and Reddit near 19x. Alphabet carries the premium because no peer pairs a dominant search franchise with a cloud business growing 63% and a $460-plus billion backlog. The premium is defensible, but it leaves little room for the AI returns to disappoint.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $359.68

- Target Price (Mid): ~$635

- Potential Total Return: ~77%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

TIKR’s mid-case scenario, realized at the end of 2030, points to a target of around $635, implying roughly 77% total return and an IRR near 13% per year. The mid case fits a stock whose central question is execution, not direction.

Two drivers carry the forecast. The first is Google Cloud, where the $460-plus billion backlog gives a compounding, contracted revenue base. The second is Google Services, where AI Overviews and AI Mode expand Search monetization, with the model assuming a forward revenue CAGR of around 16%. The margin driver is Cloud operating leverage, where Ashkenazi noted margins reached 33% as the segment tripled operating income to $7 billion, supporting a net income margin near 34% in the model.

The primary risk is the inverse of that leverage: if the $180-plus billion in annual spending fails to earn the ROIC management promises, free cash flow stays compressed, and the dilution permanently lowers per-share value. The upside is contracted demand converting on schedule and AI lifting Search. The downside is AI returns arriving late or thin, leaving shareholders with more shares against softer cash flow.

Conclusion

The raise is done. The verdict now rests on conversion. Watch whether the $460-plus billion Cloud backlog converts at the pace Pichai promised, recognizing just over half within 24 months of the Q1 2026 report. The threshold is clean: Cloud growth holding above 50% with steady or expanding margins means the spend is working and the dilution fades. Cloud decelerating toward the 30s while free cash flow stays compressed validates the bears. The July 23, 2026 earnings report is the first checkpoint, but the real answer comes over the following year as new capacity comes online.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!