Key Stats for Meta Platforms Stock

- Current Price: $605.06

- Street Target (Mean): ~$827

- TIKR Model Target Price (Mid): ~$1,289

- Potential Total Return (Mid): ~113%

- Annualized IRR: ~18% / year

- Earnings Reaction: -8.55% (April 29, 2026)

- Max Drawdown: -33.45% (March 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Meta Platforms (META) began notifying roughly 8,000 employees today that their jobs are gone.

The cuts represent 10% of the global workforce and touch every major business unit: Reality Labs, Facebook’s social division, recruiting, sales, and global operations. A second round is reportedly planned for the second half of 2026. The stock is also down 24% from its 52-week high of $796.25, and the post-earnings selloff on April 29 knocked another 8.55% off in a single session.

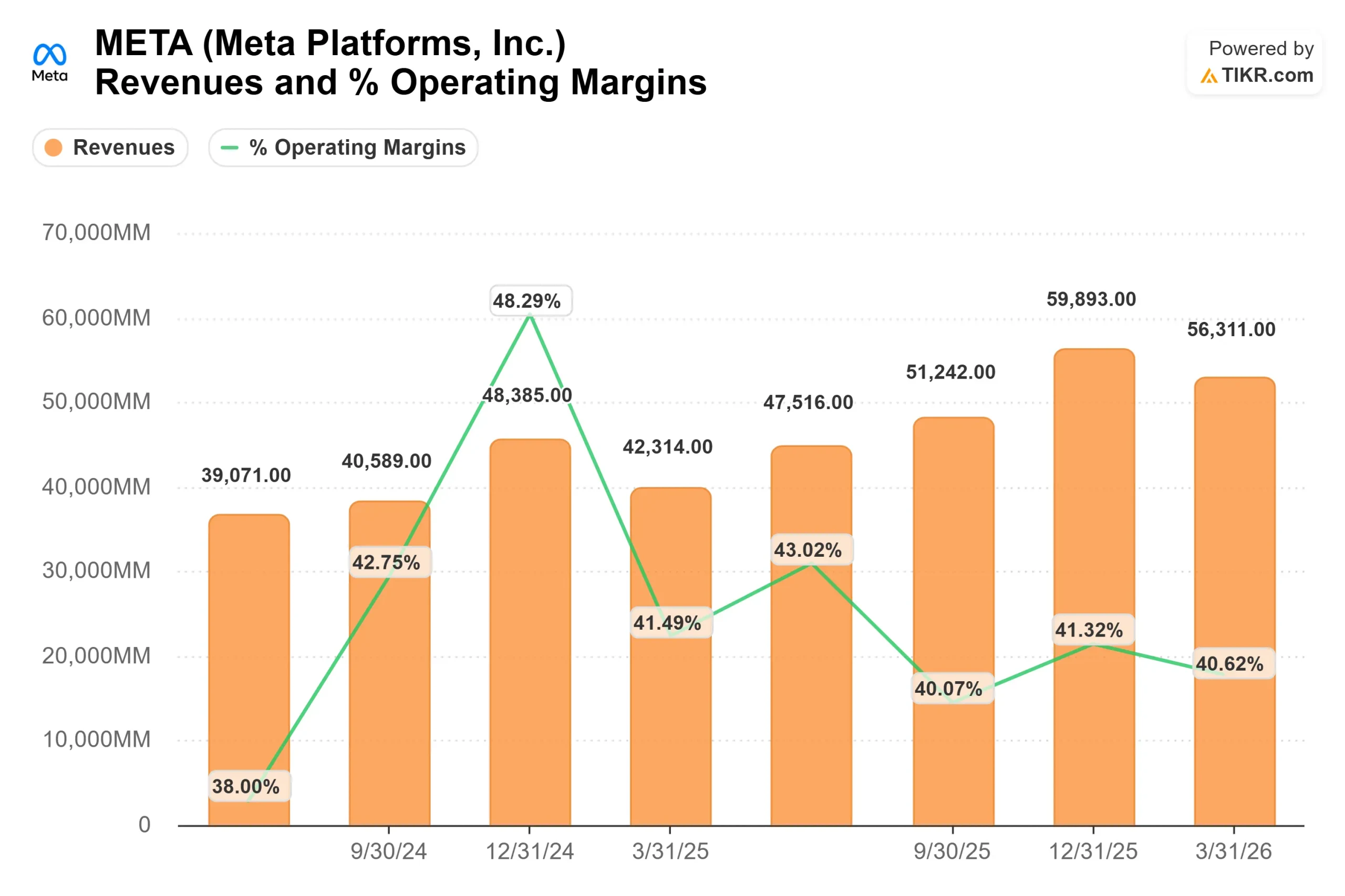

But bulls and bears are not fighting about whether Meta’s business is broken. Revenue is growing at 33% annually, and the company generated $56.3 billion in a single quarter. The real question is whether the infrastructure spending required to stay at the AI frontier will compress returns long enough to matter.

The Layoffs Are a Reallocation, Not a Retreat

CFO Susan Li explained on the Q1 2026 earnings call: “We believe a leaner operating model will allow us to move more quickly while also helping to offset the substantial investments we’re making.”

Meta is cutting labor costs to fund data centers, custom silicon built with Broadcom, AMD chips, and new NVIDIA systems. CEO Mark Zuckerberg described the underlying logic: “We are seeing more and more examples where one or two people are building something in a week that would have previously taken dozens of people months.”

Meta ended Q1 2026 with 77,900 employees, already down 1% from Q4 through earlier efficiency efforts. Capital expenditure guidance for 2026 has been raised to $125 to $145 billion, up from $69.7 billion in 2025. The trade is straightforward: fewer people, significantly more compute.

The Ad Engine Is Already Paying for the Bet

The most underappreciated fact from the Q1 2026 call is how much AI is already working inside Meta’s ad business, before Muse Spark’s capabilities are fully deployed.

Ad impressions across Meta’s services grew 19% in Q1, and the average price per ad rose 12% year-over-year. Those two levers drove Family of Apps revenue to $55 billion, up 33% from a year earlier. On Instagram, ranking improvements drove a 10% lift in Reels time spent. On Facebook, video time increased more than 8% globally, the largest quarter-over-quarter gain in four years.

Meta’s adaptive ranking model (an LLM-scale ads recommender) expanded in Q1 to support off-site conversions, driving a 1.6% increase in conversion rates across Facebook and Instagram. At Meta’s scale of over 3.5 billion daily users, that compounds into a material revenue impact. The value optimization suite, which prioritizes high-value conversions for advertisers, crossed $20 billion in annual revenue run rate in Q1, more than doubling year-over-year. Partnership ads hit a $10 billion revenue run rate, also more than doubling.

According to Emarketer’s April 2026 forecast, Meta is on track to reach $243.46 billion in net worldwide ad revenue in 2026, which would surpass Google’s projected $239.54 billion for the first time ever. Meta’s ad revenue growth rate of 24.1% is running roughly double Google’s projected 11.9%.

The Q1 numbers, a 41% operating margin on $56.3 billion in revenue, show that margin compression from infrastructure spending is real but not catastrophic.

See historical and forward estimates for Meta Platforms stock (It’s free!) >>>

Muse Spark and What the Market Missed

Before April 8, the market had a specific concern: that Meta’s heavy investment in building Meta Superintelligence Labs (MSL) was producing nothing. Llama 4 had disappointed, and reports of model delays circulated.

Then Muse Spark launched on April 8, and the stock rose around 7 to 9% in the following sessions, per analyst notes and news coverage at the time.

Muse Spark is MSL’s first model and now powers Meta AI across WhatsApp, Instagram, Facebook, Messenger, and the standalone Meta AI app. The engagement data from the Q1 call is where investors appear to have left evidence on the table. Li reported double-digit percentage increases in Meta AI sessions per user since the Muse Spark rollout. The Meta AI app has “consistently been near the top of the app stores,” per Zuckerberg. Business AI conversations on WhatsApp grew 10x since the start of 2026, reaching more than 10 million weekly conversations.

Zuckerberg was asked directly about the return on invested capital on all this spending. His answer: “The formula for our company has always been build experiences that can get to billions of people and focus on monetizing them once you get to scale.” On model quality and product scale, the first two milestones he tracks, he said: “I’m quite comfortable.”

Where Meta Trades vs. Peers

At 10.18x NTM EV/EBITDA and 18.43x NTM P/E, per TIKR, Meta commands only a modest premium to peers given the gap in scale. Tencent trades at 9.94x NTM EV/EBITDA, Pinterest at 7.29x, and Reddit at 16.74x. On NTM P/E, Tencent is at 13.05x, Pinterest is at 9.96x, and Reddit is at 20.07x.

Meta’s trailing twelve months revenue is $214.96 billion. Reddit’s entire market cap is $28.24 billion. The fact that both companies trade within a few turns of each other on EV/EBITDA reflects how heavily the CapEx cycle has discounted Meta, not a genuine equivalence in business quality.

See how Meta Platforms performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $605.06

- TIKR Model Target Price (Mid): ~$1,289

- Potential Total Return (Mid): ~113%

- Annualized IRR: ~18% / year

See analysts’ growth forecasts and price targets for Meta Platforms stock (It’s free!) >>>

The mid-case uses a 16% revenue CAGR through 2030. The two primary growth drivers are AI-powered advertising (impressions, pricing, and conversion rates compounding) and the gradual monetization of new surfaces such as WhatsApp messaging ads, business AI, and consumer agent products. Q1 2026 showed each of these already generating real revenue.

On free cash flow: LTM FCF is $25.06 billion, but near-term forward FCF is expected to be negative as CapEx peaks. The model projects FCF margins recovering to around 17% by 2030 as the infrastructure buildout matures, per TIKR estimates. The mid-case net income margin of 34.6% means Meta does not need multiple expansions to reach the target price. That is an important distinction.

The downside is real. If CapEx stays elevated beyond 2027 or regulatory action constrains ad targeting in the EU or U.S., the IRR compresses. Li flagged on the Q1 call that youth-related trials scheduled for 2026 “may ultimately result in a material loss.” That tail risk deserves weight.

The upside is equally specific. If Muse Spark enables a consumer AI subscription tier at even a fraction of Meta’s 3.5 billion daily users, the revenue base expands well beyond what the ad model currently prices in. Zuckerberg was direct about this: “people are going to also be willing to pay a lot of money to have premium or high compute versions of it.”

Conclusion

The layoffs this week are not the story for investors. They are the setup. Meta enters the second half of 2026 as a leaner company with more compute, a proven AI model, and an ad engine already generating measurable returns.

The catalyst to watch is Q3 2026 earnings, expected around late October. Beyond whether Meta delivers revenue in line with Q2 guidance of $58 to $61 billion, the key signal will be any concrete monetization tied to Meta AI: a subscription tier, structured business AI pricing, or commerce data from WhatsApp. That is what turns this from a valuation argument into a confirmed earnings story.

The TIKR mid-case model projects the stock at roughly double today’s price by the end of 2030, without requiring multiple expansions. The Street’s mean target of ~$827 implies around 37% upside on a 12-month basis alone. The layoffs are painful for the people involved. For the business, they are a calculated step toward the company Meta is trying to become.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Meta Platforms?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Meta Platforms, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Meta Platforms alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Meta Platforms on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!