Key Stats for Shopify Stock

- 52-Week Range: $94 to $182

- Current Price: $101

- Street Mean Target: $152

- Street High Target: $200

- Analyst Consensus: 28 Buys / 10 Outperforms / 12 Holds / 1 Sell

- TIKR Model Target (Dec. 2030): $257

Shopify Stock Drops 15% After Q1 Beat as AI Cost Fears Overshadow Record GMV

Shopify Inc. (SHOP), the Canadian e-commerce infrastructure company powering over a million merchants worldwide, fell 16% on the Toronto Stock Exchange on May 5 following Q1 2026 earnings that delivered a revenue beat and record GMV while guiding for decelerating growth and sharply higher operating expenses.

The headline numbers were unambiguously strong: Q1 revenue rose 34% year-over-year to $3.17 billion, clearing analyst estimates of $3.08 billion, while gross merchandise volume hit $101 billion for the second consecutive quarter at over $100 billion.

What rattled investors was not the quarter itself, but what management said about the cost to sustain it.

Operating expenses surged over 20% in Q1, driven by investments in AI infrastructure, Sidekick usage costs tied to growing LLM consumption, and internal AI tooling buildout, pulling operating expenses to 37% of revenue even as the company delivered gross profit growth of 32%.

The Q2 outlook landed broadly in line with consensus: revenue guided to grow at a “high-twenties” percentage rate, against an analyst estimate of around 27%, while gross profit is expected to grow at a “mid-twenties” pace.

Thrive Capital, the venture fund led by Joshua Kushner, disclosed a $100 million investment in Shopify on May 14, a notable vote of confidence from a high-profile growth investor even as the broader software sector grappled with AI disruption fears.

Separately, a minor antitrust development surfaced on May 12 when a court allowed Sezzle’s core antitrust claims against Shopify to proceed, though Shopify’s motion to dismiss was partially granted, limiting the scope of the case.

The stock traded at $101 as of May 19, sitting 45% below its 52-week high of $182 and just 8% above its 52-week low of $94, placing Shopify stock near the bottom of its range as the market weighs the cost curve of AI-native commerce against one of the most consistent growth records in technology.

Wall Street Holds Conviction on Shopify Stock Despite Post-Earnings Selloff

The Q1 beat that sent SHOP down 15% is the kind of contradiction Wall Street’s coverage table makes easier to read: 28 Buy ratings, 10 Outperforms, 12 Holds, and just 1 Sell, with a mean price target of $152, implying around 50% upside from Shopify stock’s current price of $101.

The Street’s conviction is anchored in revenue, not because the earnings-per-share story is uninteresting, but because Shopify’s investment case has always been about the pace at which it is capturing a larger share of global commerce infrastructure.

Consensus revenue for the June quarter sits at around $3.44 billion, reflecting around 28% year-over-year growth, with full-year 2026 revenue tracked at approximately $13.9 billion, sustaining a multi-year run of 30%-plus compounding that very few platforms at this scale have maintained.

The bull thesis is structural: Shopify is not just an e-commerce platform anymore; it is the operating system for agentic commerce, the only platform currently powering merchant selling inside ChatGPT, Microsoft Copilot, and Google simultaneously from one system of record, a position President Harley Finkelstein described on the Q1 earnings call as putting Shopify “at the epicenter” of the AI commerce era.

The bear concern is more immediate: operating expense growth running at 20%-plus while revenue growth decelerates from 34% to a guided high-twenties pace creates compression risk, and the Street’s 12 Hold ratings reflect exactly that tension, investors who believe the story but want proof that the cost curve bends before re-rating the multiple higher.

What has not changed is the cohort math that CFO Jeff Hoffmeister highlighted on the call: almost 90% of Q1 revenue came from merchants who had been on the platform for more than a year, a retention signal that validates the stickiness of Shopify’s commerce stack even as critics question whether AI agents will disintermediate traditional storefronts.

The Thrive Capital $100 million stake announced on May 14 adds a secondary data point: growth-stage investors with long time horizons are buying the selloff, not selling it, which tends to matter when a stock is sitting 45% off its highs.

At $101 with a mean Street target of $152 and 38 Buy or Outperform ratings out of 51 covering analysts, Shopify stock appears undervalued relative to the breadth and durability of the revenue compounding engine the data reveals.

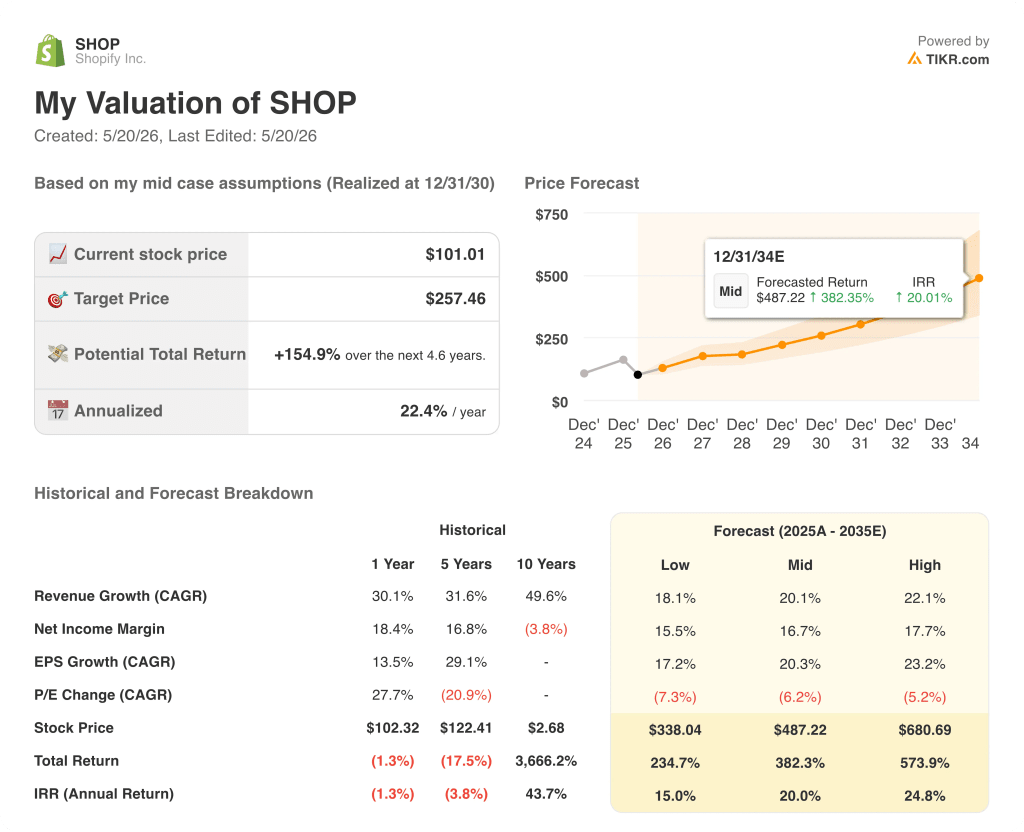

Shopify’s Valuation Model Take: A $257 Base Case Against a $101 Stock Price

TIKR’s base case values Shopify at $257 per share, reaching that target by December 2030, anchored to a mid-case revenue CAGR of around 20% from 2025 through 2035 and a net income margin assumption of around 17%, consistent with the operating leverage trajectory management has been guiding toward for several consecutive quarters.

The distance between TIKR’s $257 mid-case target and Shopify stock’s current price of $101 implies around 155% total return over 4 and a half years, equivalent to an annualized IRR of around 22%, a risk-reward profile that positions Shopify stock as undervalued given the breadth of the platform’s growth across enterprise, B2B, international, and agentic commerce channels.

The argument hinges on one question: does Shopify’s operating expense discipline catch up to its revenue trajectory fast enough to justify the multiple the bull case requires, or does the cost of building AI-native commerce infrastructure outpace the margin expansion the model assumes?

Is Shopify stock undervalued right now?

TIKR’s base case values Shopify at around $257 per share, implying around 155% upside from the current price of $101.

With 38 analysts issuing Buy or Outperform ratings and a mean Street target of $152, the consensus view supports that Shopify stock is undervalued at these levels.

The key variable is operating expense discipline: if the 37% OpEx-to-revenue ratio in Q1 continues compressing toward the mid-thirties range, the margin expansion required for the base case valuation holds.

Should You Invest in Shopify Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Shopify Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Shopify Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze X stock on TIKR for Free →