Key Takeaways:

- AI-Led Industry Shock: Take-Two stock fell about 10% last week after Google unveiled AI-generated game worlds, reshaping development cost expectations.

- Franchise Momentum: Take-Two stock reflects strength after Wells Fargo raised its target to $288, citing GTA Online growth and mobile bookings momentum.

- Price Projection: Based on valuation assumptions through March 2028, Take-Two stock could reach $353 as revenue scales and margins normalize.

- Upside Math: That target implies 60% upside from the current $220 price, translating into roughly 24% annualized gains over about 2 years.

Take-Two Interactive (TTWO) develops premium console, PC, and mobile games, anchored by franchises like GTA and NBA 2K with global scale.

Last week in January, Take-Two stock dropped about 10% after Google’s AI world-generation model raised concerns about future game development economics.

Take-Two generated about $6 billion in LTM revenue, reflecting durable demand across core franchises and recurring digital spending.

Recent operating performance produced roughly $1 billion in profit with margins near 22%, supported by scale, digital mix, and live-service content.

With a market value near $38 billion, Take-Two trades at elevated multiples despite strong fundamentals, creating tension worth examining further.

What the Model Says for TTWO Stock

We analyzed Take-Two stock using operating scale, franchise depth, and recurring digital revenue supporting sustained earnings and shareholder returns.

Based on 9.4% revenue growth, 22.0% operating margins, and a 49.1x exit multiple, the model projects continued earnings expansion.

That scenario points to a $353 target price, implying 60.3% total upside and a 24.3% annual return over 2.2 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for TTWO stock:

1. Revenue Growth: 9.4%

Take-Two posted 14% ten year revenue growth, reflecting durable franchise releases and long development cycles tied to blockbuster titles.

Recent growth slowed to 6% as major launches lapped, but digital bookings and mobile titles supported revenue stability.

Forward growth depends on GTA, NBA 2K updates, and mobile scale, balanced against long production timelines and hit driven volatility.

According to consensus analyst estimates, 9.4% growth supports a $353 target and about 24% annual return without assuming release timing perfection.

2. Operating Margins: 22%

Take-Two delivered 23% operating margins over five years, showing strong scale economics during peak franchise launch periods.

Margins recently eased to 11% as development spending rose ahead of major releases and live services investment increased.

Profitability improves as marketing normalizes and digital mix rises, while risks include delays and higher content costs.

In line with analyst consensus projections, 22.0% margins reflect normalized release cadence and sustained digital contribution across core franchises.

3. Exit P/E Multiple: 49.1x

Take-Two trades near premium levels, with historical multiples around 57x one year, 41x five years, and 35x ten years.

Investor caution reflects hit risk and long cycles, while optimism rests on proprietary IP strength and repeat monetization.

The multiple requires steady execution, successful flagship launches, and margin follow through without relying on sector rerating.

Based on street consensus estimates, a 49.1x exit multiple balances franchise durability with elevated expectations embedded in a 24% annual return outlook.

What Happens If Things Go Better or Worse?

Take-Two stock’s trajectory hinges on release timing, live-service monetization, and cost discipline through 2030.

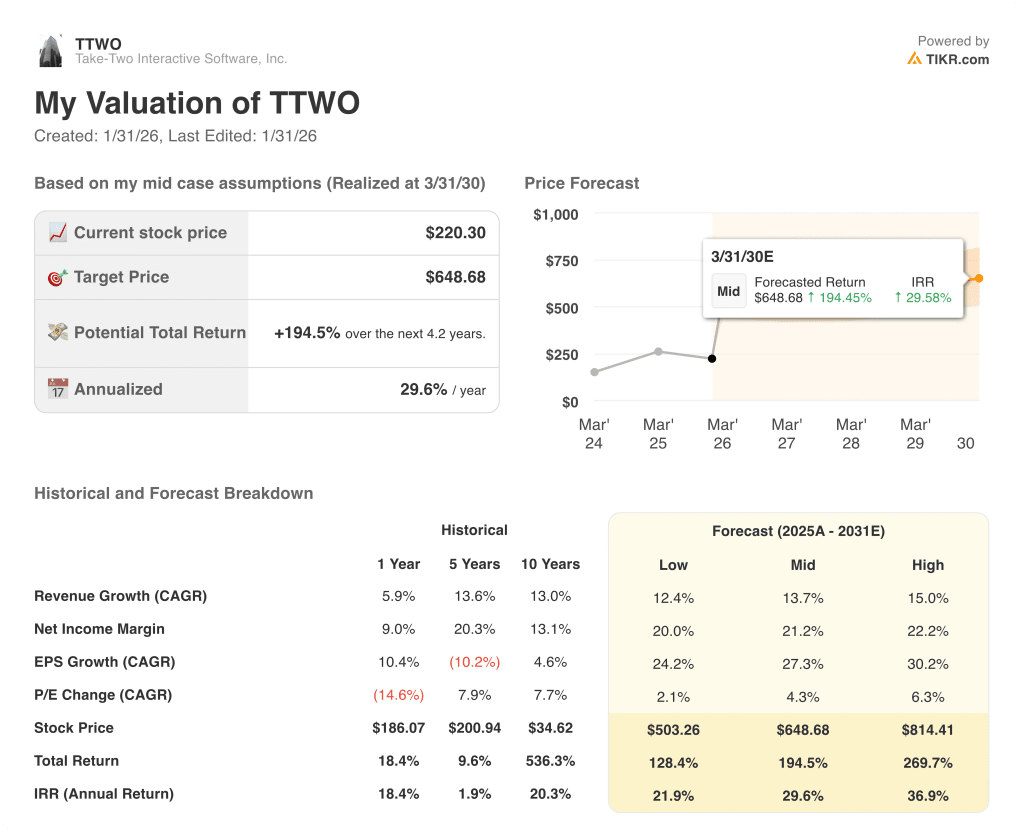

- Low Case: Delayed releases and higher costs limit revenue to 12.4% and margins to 20% → 21.9% annualized return.

- Mid Case: On-time franchise execution supports 13.7% revenue growth and 21.2% margins → 29.6% annualized return.

- High Case: Strong launches and monetization lift revenue to 15.0% and margins to 22.2% → 36.9% annualized return.

The $649 mid-case target is achievable through timely releases and margin control, without multiple expansion or narrative-driven re-rating.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!