Key Takeaways:

- Regulatory Tailwind: Garmin stock benefits as January FDA guidance limits oversight on wellness wearables, supporting consumer devices representing billions in annual revenue.

- Aviation Momentum: Garmin stock gained defense credibility after its G5000H avionics secured a 24-helicopter Brazilian Air Force modernization program.

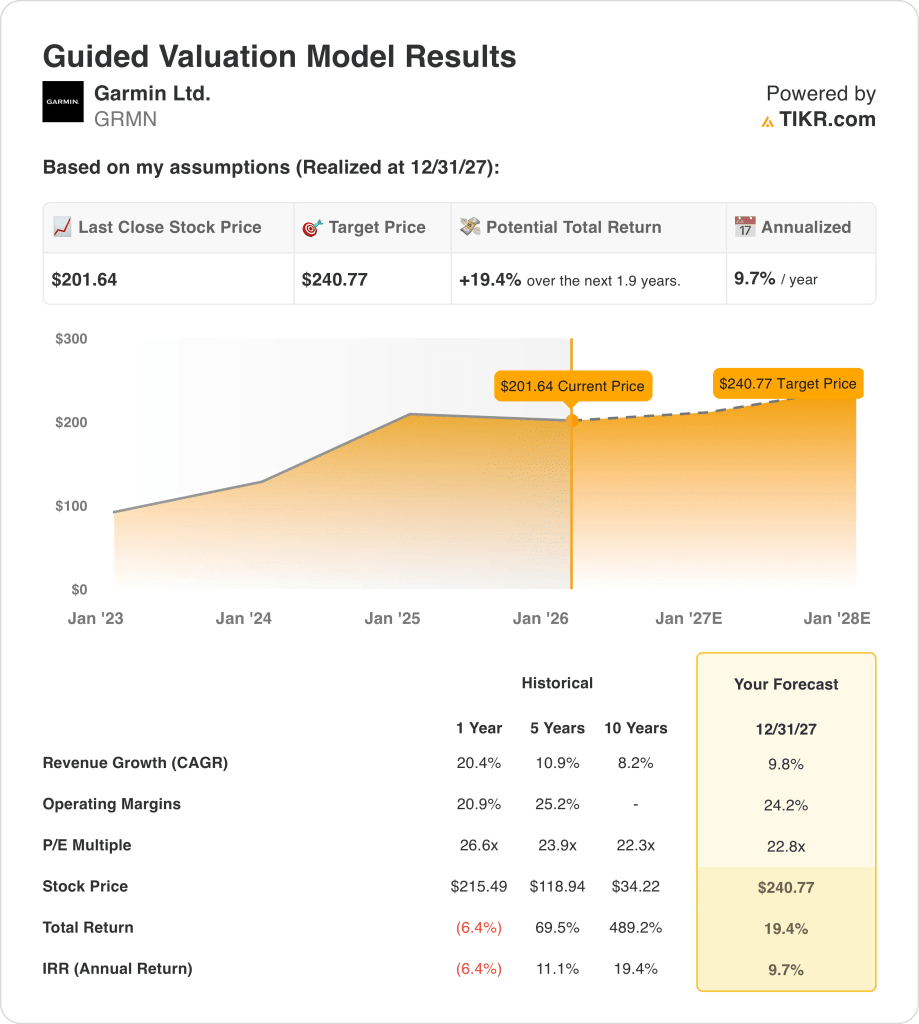

- Price Outlook: Based on 10% revenue growth, 24% operating margins, and a 23x exit multiple, Garmin stock could reach $240 by December 2027.

- Upside Math: That target implies 19% total upside from $201 today, translating into roughly 10% annualized returns for Garmin stock.

Garmin (GRMN) designs connected devices across fitness, aviation, marine, and outdoor markets, competing through hardware depth and software ecosystems across more than 100 countries.

Last January 7, FDA guidance limiting regulation on wellness wearables strengthened Garmin’s consumer positioning as shares rose nearly 3%.

Garmin generated about $7 billion in LTM revenue, showing demand durability across fitness and aviation segments after earlier consumer electronics volatility.

The company produced roughly $2 billion in operating profit, with operating margins near 26% supporting reinvestment and shareholder returns.

Garmin’s $39 billion market value prices in stability, yet a $240 valuation target raises questions about upside if execution continues without valuation expansion.

What the Model Says for GRMN Stock

Garmin combines fitness and aviation scale with strong cash generation, supporting capital returns as operating margins hold near 24.2%.

Using 9.8% revenue growth and a 22.8x exit multiple, the model points to a $240.77 target.

That implies about 19% total upside and roughly 10% annual returns over the next two years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for GRMN stock:

1. Revenue Growth: 9.8%

Garmin stock generated strong recent growth, with 20% revenue growth over the past year as fitness, aviation, and marine segments all expanded.

Current execution shows demand normalizing, but product depth across wearables and avionics supports steady growth rather than a sharp slowdown.

Looking ahead, fitness device refresh cycles and aviation backlog conversion support revenue, while consumer electronics cycles limit acceleration risk.

Using pooled analyst expectations, 9.8% revenue growth balances diversified demand strength against mature category expansion.

2. Operating Margins: 24.2%

Garmin stock historically sustained operating margins above 20%, reflecting in-house manufacturing, premium pricing, and disciplined cost control across segments.

Recent margins near 21% improved as revenue scale absorbed fixed costs and aviation mix supported profitability.

Forward margins benefit from software attachment, services, and higher-margin aviation systems, while competition in wearables caps upside.

Per compiled analyst projections, operating margins near 24% reflect a return to historical efficiency without peak-cycle assumptions.

3. Exit P/E Multiple: 22.8x

Garmin stock currently trades near a mid-20s earnings multiple, supported by consistent cash generation and balance sheet strength.

Historically, the stock held earnings multiples between roughly 22x and 26x during stable growth periods with strong returns on capital.

Investor caution reflects consumer demand cycles, while optimism rests on aviation and marine backlog durability.

Based on aggregated market forecasts, a 22.8x exit multiple reflects steady growth, stable margins, and measured capital returns.

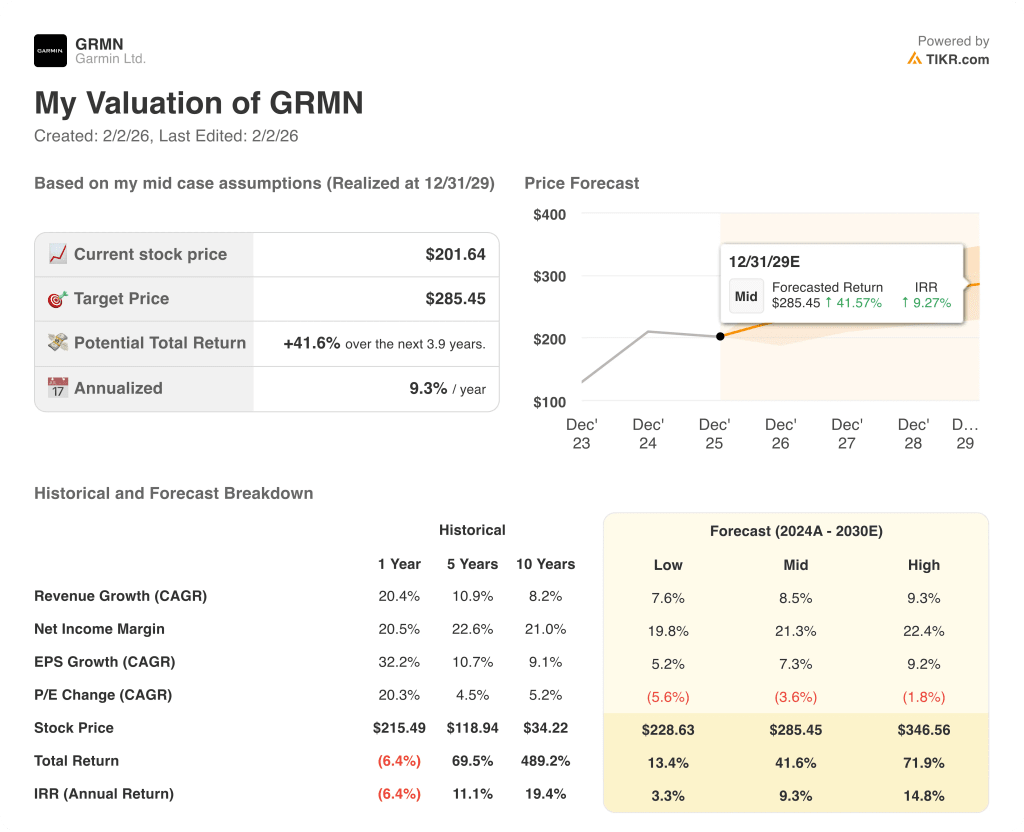

What Happens If Things Go Better or Worse?

Garmin stock’s outcomes depend on wearable demand trends, aviation order flow, and margin control across fitness, outdoor, and aviation segments through 2029.

- Low Case: If consumer wearables soften and aviation orders slow, revenue grows around 7.6% and margins stay near 19.8% → 3.3% annualized return.

- Mid Case: With fitness demand steady and aviation backlog converting, revenue growth near 8.5% and margins improving toward 21.3% → 9.3% annualized return.

- High Case: If premium wearables gain share and aviation deliveries accelerate, revenue reaches about 9.3% and margins approach 22.4% → 14.8% annualized return.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!