Key Takeaways:

- Transaction Momentum: Fifth consecutive quarter of transaction growth with 4.7% system-wide increase.

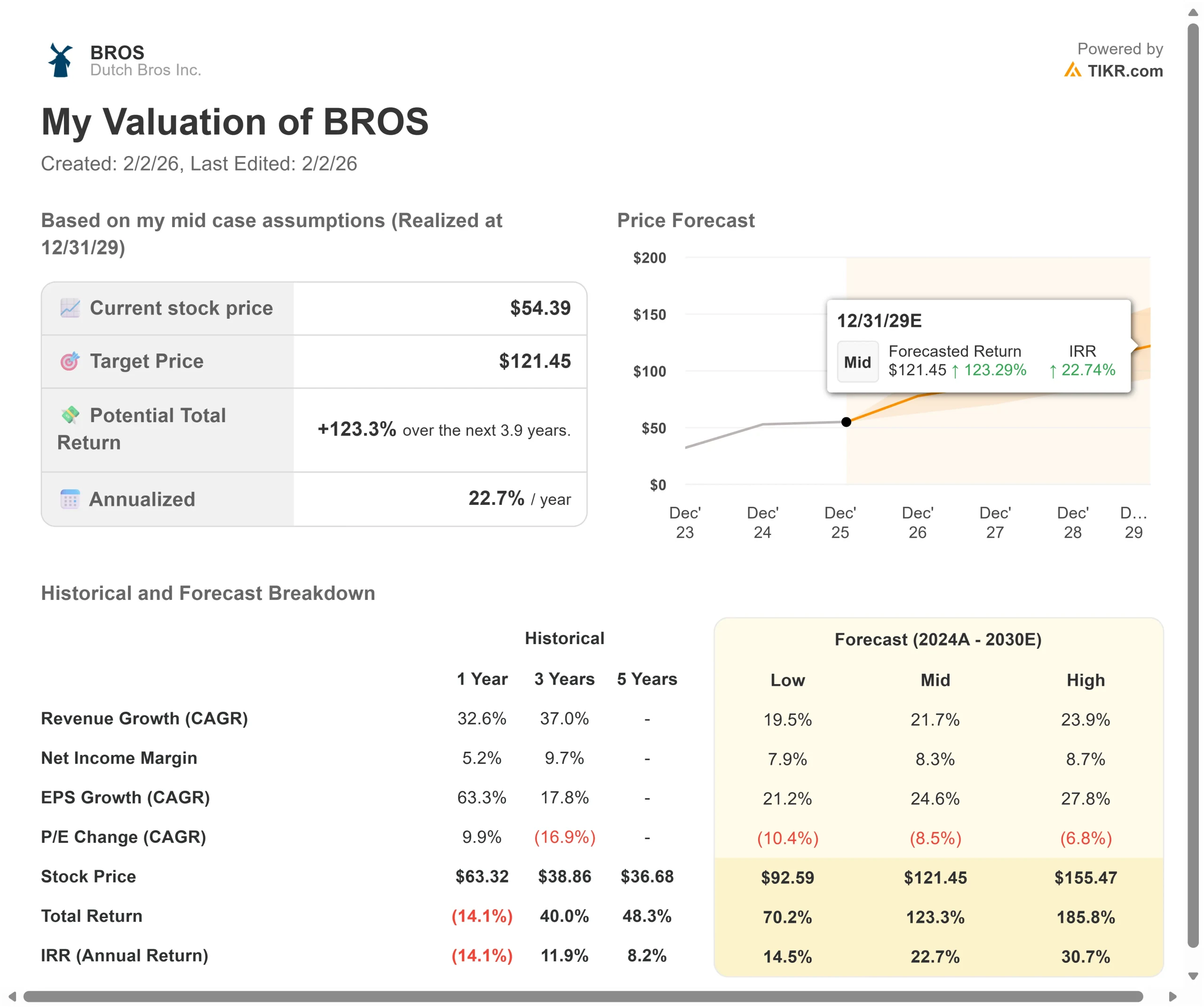

- Price Projection: Based on the current trajectory, BROS stock could reach $80 by December 2027.

- Potential Gains: This target suggests a total return of 47% from the current price of $54.

- Annual Return: Investors could see roughly 22% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Dutch Bros (BROS) just delivered another standout quarter with 25% revenue growth and same-store sales up 5.7%, while announcing plans to accelerate new shop openings to 175 locations in 2026.

The drive-thru coffee chain reached 1,081 shops and remains firmly on track toward its ambitious goal of 2,029 shops by 2029.

CEO Christine Barone is executing a multi-pronged growth strategy centered on transaction-driving initiatives.

- The company posted its fifth straight quarter of transaction growth—a rare feat in today’s restaurant environment.

- System-wide transactions grew 4.7%, while company-operated shops saw an even stronger 6.8% increase.

- New-shop productivity remains elevated, with average unit volumes at record highs.

- The company expanded into six contiguous states in 2025, bringing its total presence to 24.

- Dutch Rewards now accounts for 72% of transactions, up 5 points year-over-year, while Order Ahead reached 13% of sales, with some new markets at nearly double that rate.

Despite this exceptional momentum, Dutch Bros stock trades at $54, offering significant upside for investors who recognize the company’s differentiated position in the beverage space.

See analysts’ full growth forecasts and estimates for BROS stock (It’s free) >>>

What the Model Says for Dutch Bros Stock

We analyzed Dutch Bros as it transformed into a dominant drive-thru beverage platform with unmatched customer engagement and a clear path to national scale.

The company is expanding beyond its Western roots into the Midwest and Southeast, consistently seeing long lines and strong demand in new markets.

The brand’s differentiated culture—built around authentic broista interactions and extensive customization—creates emotional connections that drive remarkable visit frequency.

- Dutch Bros now has over 475 operators in its pipeline with an average tenure of 7.5 years.

- This depth allows the company to scale its culture effectively while maintaining the high-energy experience that sets it apart.

- The company ranked #1 in order accuracy, satisfaction, and beverage quality in the 2025 QSR drive-thru report.

Using a forecast of 24.9% annual revenue growth and 10.4% operating margins, our model projects the stock will rise to $80 within 1.9 years. This assumes a 59.1x price-to-earnings multiple.

That represents compression from Dutch Bros’ historical P/E averages of 92.4x (one year) and 123.3x (three years). The lower multiple acknowledges the company’s path toward maturity and expects some normalization as the business scales.

The real value lies in sustaining transaction momentum while executing aggressive shop expansion and rolling out the hot food program to drive breakfast occasions.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BROS stock:

1. Revenue Growth: 24.9%

Dutch Bros’ growth centers on three pillars: new shop expansion, same-store sales, and strategic initiatives.

The company expects to open approximately 175 shops in 2026, marking an acceleration from previous years.

With record-high development pipelines adding 30+ potential sites per month, management is confident it will reach 2,029 shops by 2029.

Same-store sales momentum remains robust, driven by multiple transaction-building initiatives. The hot food program, now in approximately 160 shops, is delivering a 4% comp lift, with about a quarter of the lift coming from transactions.

Management plans to complete the rollout by the end of 2026 to capture the breakfast daypart.

Digital initiatives continue gaining traction. Order Ahead is growing organically, while Dutch Rewards provides an efficient engagement channel.

The company is running almost exclusively segmented offers, demonstrating sophisticated analytics capabilities.

2. Operating margins: 10.4%

Dutch Bros is expanding margins while investing in growth.

- The company delivered 27.8% shop contribution margins in Q3 despite elevated coffee costs and higher occupancy rates from new shops.

- Management continues leveraging the capital-efficient build-to-suit lease model, with average CapEx per shop at $1.4 million.

- Adjusted EBITDA reached $78 million in Q3, up 22% year-over-year.

- The company expects approximately 110 basis points of SG&A leverage in 2025, demonstrating disciplined expense management as it scales operations.

Near-term margin pressure includes elevated coffee costs extending into 2026, higher food COGS as the hot food program rolls out, and California regulatory changes adding 50 basis points of labor pressure in Q4.

3. Exit P/E Multiple: 59.1x

The market values Dutch Bros at 66.1x earnings. We assume the P/E will compress to 59.1x over our forecast period.

Growth stocks typically see multiple compressions as they mature and scale. Dutch Bros is transitioning from a regional player to a national brand, which may command a lower premium over time.

As execution continues and the company demonstrates sustainable unit economics across diverse geographies, the concept should maintain a premium multiple.

The strong culture, transaction momentum, and clear path to 2,000+ shops support above-market valuations.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Drive-thru concepts face labor pressures and consumer spending cycles. Here’s how Dutch Bros stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 19.5% and net income margins compress to 7.9%, investors still see a 70% total return (14.5% annually).

- Mid Case: With 21.7% growth and 8.3% margins, we expect a total return of 123% (22.7% annually).

- High Case: If transaction initiatives exceed expectations and Dutch Bros maintains 8.7% margins while growing at 23.9%, total returns could reach 186% (30.7% annually).

See what analysts think about BROS stock right now (Free with TIKR) >>>

The range reflects execution on shop expansion, food program adoption, and sustained transaction growth through digital initiatives.

In the worst case, same-store sales moderate or new-shop productivity disappoints in unfamiliar markets.

In the best case, the hot food program drives stronger breakfast occasions than anticipated, Order Ahead accelerates faster, and shop expansion maintains current momentum with elevated unit volumes.

How Much Upside Does Dutch Bros Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!