Key Takeaways:

- Infrastructure Scale: Public Service Enterprise Group stock reflects regulated utility scale, with 25,000 circuit miles supporting stable earnings across more than 2,000,000 customers.

- Operational Execution: Public Service Enterprise Group stock shows resilient execution, restoring power to 3,140 customers after storms while maintaining service reliability across its network.

- Price Outlook: Public Service Enterprise Group stock could reach $103 by December 2027, supported by regulated rate recovery and operating margins near 30%.

- Upside Math: Public Service Enterprise Group stock implies 25% total upside from $82, translating into a 12% annualized return over 2 years

Public Service Enterprise Group (PEG) provides regulated electric, gas, and nuclear power services, with 25,000 circuit miles supporting essential energy demand across New Jersey.

Last week in January, Public Service Enterprise Group highlighted operational resilience after restoring service to 3,140 customers following winter storm disruptions.

Public Service Enterprise Group generated $12 billion in LTM revenue, reflecting stable utility demand tied to regulated customer bases and infrastructure investment programs.

PEG stock’s operating income reached nearly $3 billion LTM with a 26% margin, supported by rate recovery, cost discipline, and scale efficiencies.

PEG stock trades near $82 while valuation implies $103, creating tension between steady fundamentals and restrained utility sector pricing.

What the Model Says for PEG Stock

We assessed Public Service Enterprise Group using regulated utility positioning, supported by steady cash flows and improving operating efficiency.

Using 7.4% revenue growth, 29.6% operating margins, and a 20.3x exit multiple, the model projects a $103 price.

That outcome represents 25% total upside and about 13% annual return, ending at $103 with 13% annual gains.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PEG stock:

1. Revenue Growth: 7.4%

Public Service Enterprise Group generated about $12 billion in LTM revenue, recovering after a prior 8% decline tied to weather and regulatory timing.

Recent quarterly revenue reached about $3 billion, supported by regulated rate base growth and steady electric and gas customer demand.

Growth relies on approved capital spending, grid investment, and efficiency programs, constrained by weather volatility and regulatory timing.

As reflected in aggregated market forecasts, 7.4% revenue growth balances regulated stability against softer non-regulated power and post-cycle normalization.

2. Operating Margins: 29.6%

PEG stock posted operating margins near 26% LTM, below the 31% peak reached during favorable power and cost conditions.

Margins improved as outage costs normalized and efficiency programs reduced operating expense pressure across transmission and distribution networks.

Profitability depends on rate recovery, cost control, and steady nuclear output, with storms and fuel costs as key risks.

Per compiled analyst expectations, operating margins near 29.6% align with historical levels without assuming unusually supportive cost or pricing conditions.

3. Exit P/E Multiple: 20.3x

PEG stock traded near 18x to 20x earnings historically during stable rate cycles and predictable cash flow periods.

The stock currently reflects cautious sentiment tied to recent revenue volatility and capital spending intensity across regulated utilities.

A higher multiple requires consistent earnings delivery, regulatory support, and continued capital return visibility through dividends and buybacks.

According to pooled market forecasts, a 20.3x exit multiple assumes steady regulated earnings, capital discipline, and normalized growth.

What Happens If Things Go Better or Worse?

Public Service Enterprise Group’s outcomes hinge on regulated rate recovery, capital spending discipline, and execution across utility and power segments through 2029.

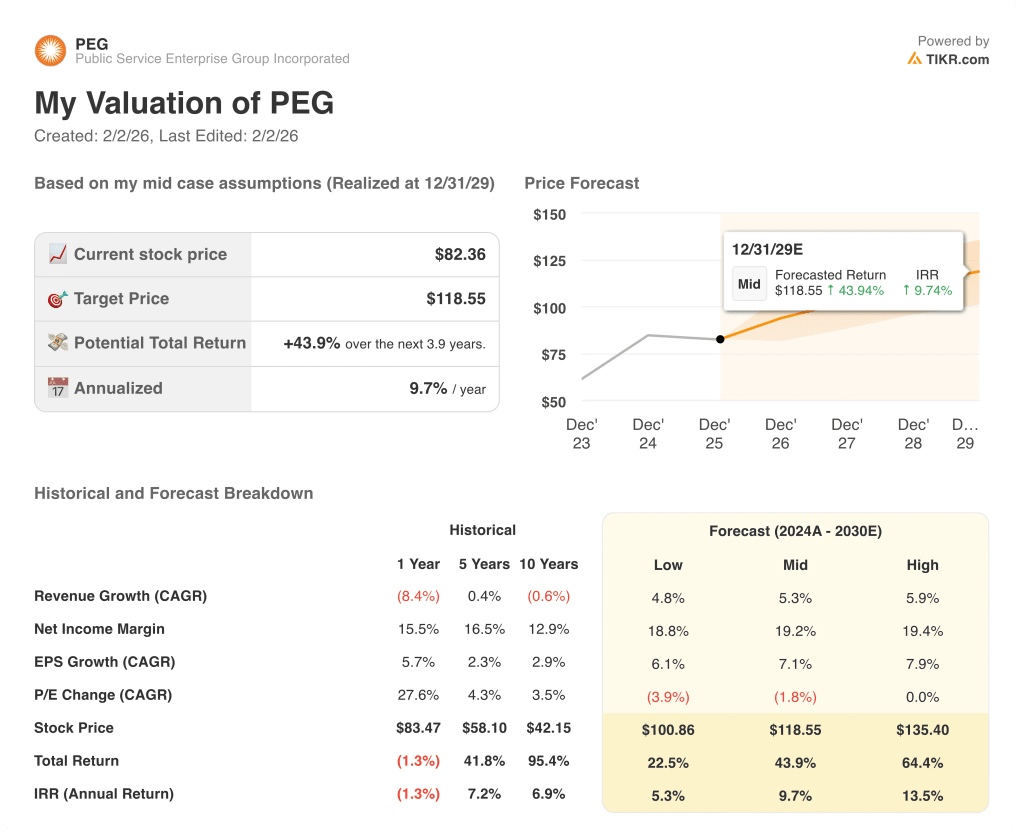

- Low Case: If rate recovery slows and non-regulated power remains soft, revenue grows around 5% → 5.3% annualized return.

- Mid Case: With regulated investments progressing as planned, revenue growth near 5.3% → 9.7% annualized return.

- High Case: If rate approvals accelerate and power segment performance stabilizes, revenue reaches 5.9% → 13.5% annualized return.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!