Key Takeaways:

- BASE44 Momentum: New AI app-building platform reached $50 million ARR within months of acquisition.

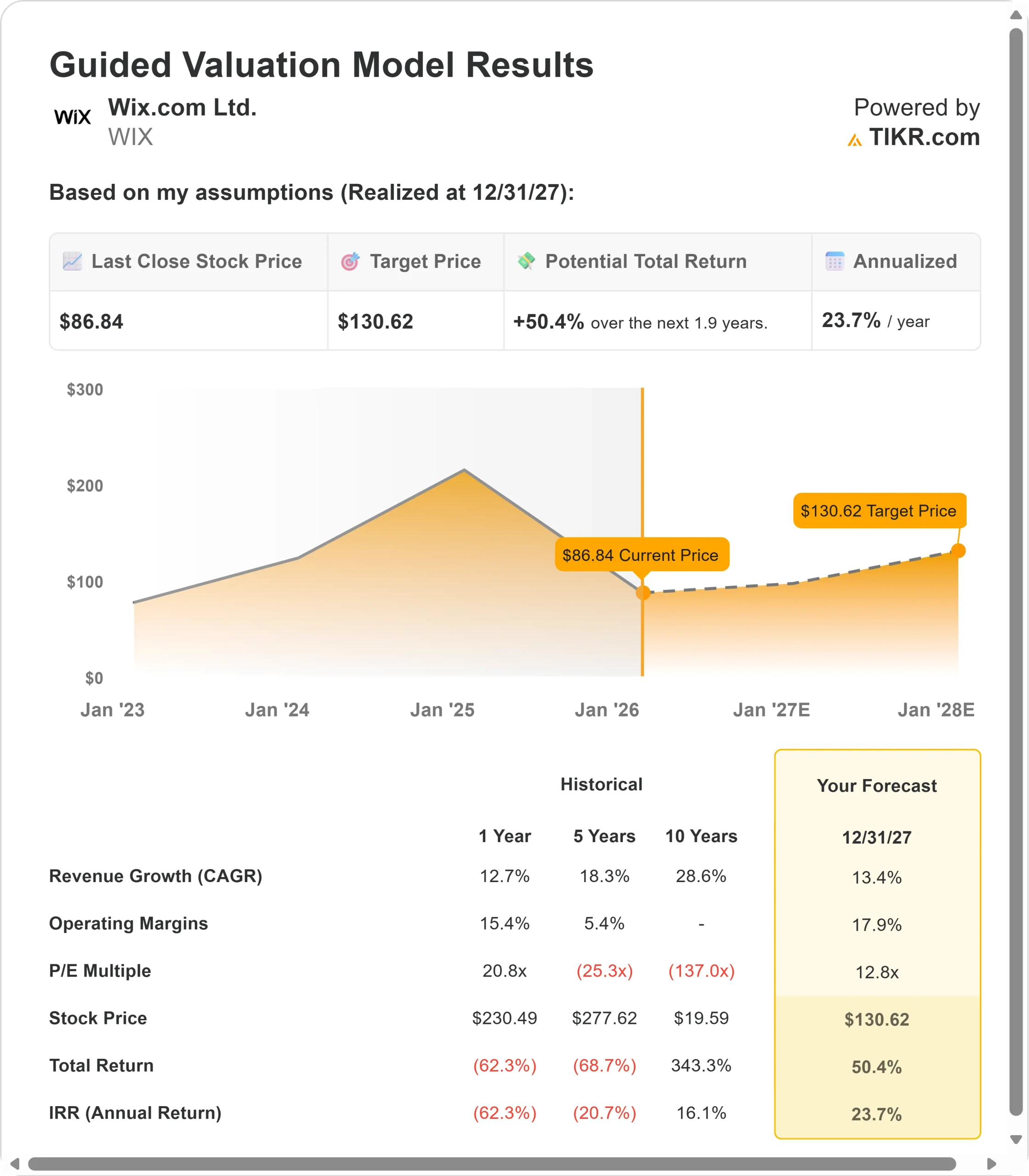

- Price Projection: Based on current execution, WIX stock could reach $131 by December 2027.

- Potential Gains: This target implies a total return of 50% from the current price of $86.84.

- Annual Return: Investors could see roughly 24% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Wix.com Ltd. (WIX) delivered strong Q3 results with revenue hitting $505 million, up 14% year-over-year, while bookings jumped to $515 million. The company is executing a bold expansion beyond website creation into AI-powered application building through its BASE44 acquisition.

CEO Avishai Abrahami is pursuing an aggressive vision centered on “vibe coding” – making software creation accessible to everyone through natural language. BASE44 now serves over 2 million users, a sevenfold increase since June, with more than 1,000 new paying subscribers joining daily.

The platform’s share of AI app-building traffic surged to over 10% by October from low single digits just months earlier.

Wix raised its 2025 bookings guidance to $2,060-$2,078 million, representing 13-14% growth, driven primarily by BASE44’s exceptional performance.

Despite this momentum, Wix stock trades at $87, down 34% from recent peaks, presenting upside for investors who recognize the company’s position in democratizing software creation.

See analysts’ full growth forecasts and estimates for WIX stock (It’s free) >>>

What the Model Says for Wix Stock

We analyzed Wix’s transformation from a website builder into a comprehensive platform that supports both web creation and AI-powered application development.

- The BASE44 acquisition opens an enormous new market.

- While businesses need just one website, they often require multiple applications – for scheduling, inventory, vendor management, and more.

- The vibe coding market grew explosively in 2025, and Wix captured a meaningful share by applying its proven playbook of comprehensive branding, aggressive marketing, and superior product development.

The company maintains solid fundamentals in its core business. New user cohorts continued performing strongly through Q3, with customers purchasing longer subscription plans and adopting more business applications.

Transaction revenue accelerated 20% as merchants increasingly chose Wix Payments, while gross payment volume grew 13% to $3.7 billion.

Using a forecast of 13.4% annual revenue growth and 17.9% operating margins, our model projects the stock will rise to $131 within 1.9 years. This assumes a 12.8x price-to-earnings multiple.

That represents compression from Wix’s historical P/E averages of 20.8x (one year) and 32.2x (three years). The lower multiple reflects near-term margin pressure from BASE44’s front-loaded costs and the platform’s monthly subscription mix, which differs from Wix’s predominantly annual billing.

The real value lies in successfully scaling BASE44 while maintaining core business strength and expanding operating leverage as the acquired business matures.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for WIX stock:

1. Revenue Growth: 13.4%

Wix’s growth centers on two engines working in tandem.

The core business showed resilience with bookings up 14% in Q3. New user cohorts maintained strong behavior patterns established in the first half, purchasing advanced subscriptions and longer-duration plans.

Partners’ revenue jumped 24% to $192 million, driven by professional designers and studio adoption.

BASE44 adds a completely new growth vector. Management now expects at least $50 million in ARR by year-end, up from initial projections.

The platform operates on monthly subscriptions, resulting in straight-line revenue recognition compared to Wix’s front-loaded annual billing.

This means BASE44’s full revenue impact will materialize over time as cohorts build and renew.

2. Operating margins: 17.9%

Wix faces near-term margin pressure as it builds BASE44’s foundation, but the path to improved profitability is clear.

Q3 operating margin came in at 18%, down from higher levels as the company invested aggressively in the new platform. Two factors drive current headwinds: AI processing costs and marketing investments.

New BASE44 users consume significantly more AI tokens during initial app creation compared to recurring users maintaining existing applications.

As the user base matures, this cost structure should improve dramatically. Management already expects AI costs to decline as competition among providers intensifies.

Marketing spending jumped 23% sequentially as Wix deployed its proven playbook to BASE44, which had zero marketing infrastructure at acquisition.

These investments delivered returns exceeding expectations, enabling confident scaling. Both branding costs and customer acquisition targets should be optimized as BASE44 gains recognition.

CFO Lior Shemesh expects BASE44 to achieve operating margins comparable to core Wix’s long-term as the business scales and the company leverages its track record of driving efficiency.

3. Exit P/E Multiple: 12.8x

The market values Wix at 13.8x earnings currently. We assume modest compression to 12.8x over our forecast period.

Near-term integration complexity and margin pressure from BASE44 investments weigh on the multiple. The company must successfully scale a new business model while maintaining momentum across legacy operations.

However, Wix’s proven ability to democratize emerging technologies and capture new markets should support valuation recovery.

As BASE44 demonstrates sustainable unit economics and margin expansion begins, the market should reward execution with multiple expansions from these depressed levels.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Software platforms face technology transitions and execution risk on new initiatives. Here’s how Wix stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 10.7% and net income margins compress to 23.0%, investors still see an 80% total return (16% annually).

- Mid Case: With 11.9% growth and 24.3% margins, we expect a total return of 128% (23% annually).

- High Case: If BASE44 adoption accelerates and Wix maintains 25.8% margins while growing at 13.1%, total returns could reach 187% (31% annually).

See what analysts think about WIX stock right now (Free with TIKR) >>>

The range reflects execution on scaling BASE44, maintaining core business momentum, and achieving margin expansion as the app-building platform matures.

In the low case, AI app adoption moderates or integration challenges emerge.

In the high case, vibe coding demand exceeds expectations, BASE44’s user mix shifts toward annual plans faster than anticipated, and AI costs decline ahead of schedule.

How Much Upside Does Wix Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!