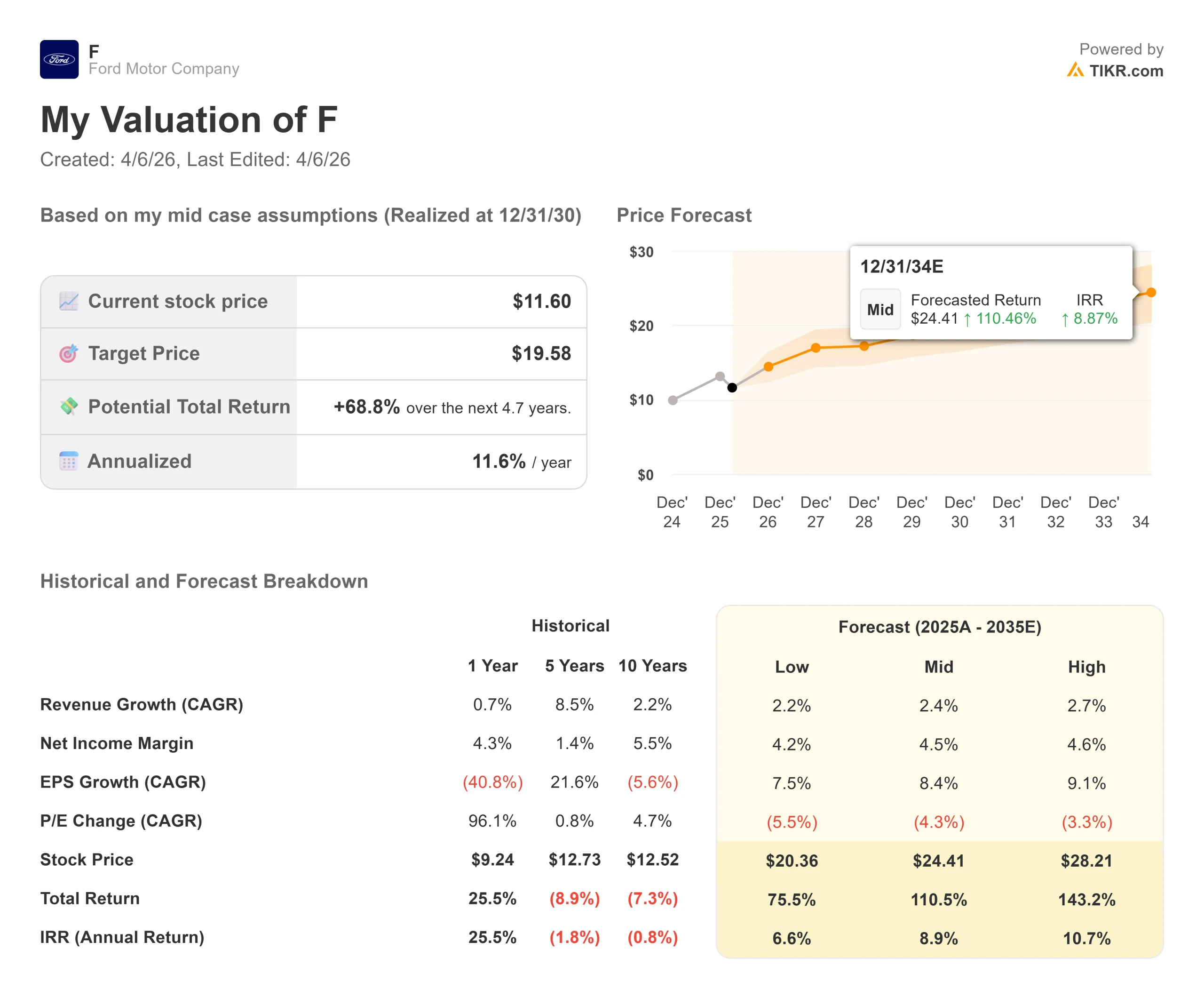

Key Stats for Ford Stock

- Current Price: $11.60

- Target Price (Mid): $19.58

- Street Target (Mean): $14.09

- Potential Total Return (Mid): +68.8%

- Annualized IRR (Mid): 8.90% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Ford (F) stock has fallen 22.31% from its one-year high, reaching that low on March 30, 2026, and sits 12% below where it opened the year.

Bears point to a $4.8 billion annual EV loss, recurring tariff headwinds, and two consecutive years of distorted earnings. Bulls see $187 billion in revenue, a 5.2% dividend yield, and a forward P/E of 7.62x near a multi-year floor.

The tension sharpened on April 2, 2026, when President Trump announced 25% tariffs on all imported automobiles and parts.

Ford CEO Jim Farley called the levies “the most significant challenge facing our industry in decades.” Ford estimated the tariffs would cost approximately $1.5 billion in adjusted EBIT this year. The Center for Automotive Research projected combined additional costs of roughly $41.7 billion across Ford, GM, and Stellantis from the new tariff package.

That announcement landed less than two months after Ford’s Q4 2025 earnings on February 10, 2026, where Farley told analysts the company generated “$6.8 billion of adjusted EBIT for the full year,” including a $2 billion Novelis headwind and a $2 billion net tariff impact.

CFO Sherry House confirmed that without a surprise late-year tariff credit reversal, full-year EBIT would have reached $7.7 billion.

The stock rose 2.06% on earnings day despite the miss. For 2026, Ford guided for $8 to $10 billion in adjusted EBIT and $5 to $6 billion in adjusted free cash flow, guidance now under review given the April tariff announcement.

See historical and forward estimates for Ford stock (It’s free!) >>>

Is Ford Undervalued Today?

At 7.62x forward P/E and 9.36x NTM market cap to free cash flow, Ford is one of the cheapest large-cap industrials in the U.S. market. LTM levered free cash flow of approximately $5.4 billion covers the 5.2% dividend yield, paying investors to wait while the thesis plays out.

The recovery case rests on three things.

First, the 2025 earnings baseline was distorted. The $6.8 billion in adjusted company EBIT absorbed $4 billion in combined headwinds from Novelis and the tariff credit reversal. Strip those out and the underlying run rate was closer to $7.7 billion. The 2026 guide reflects that recovery.

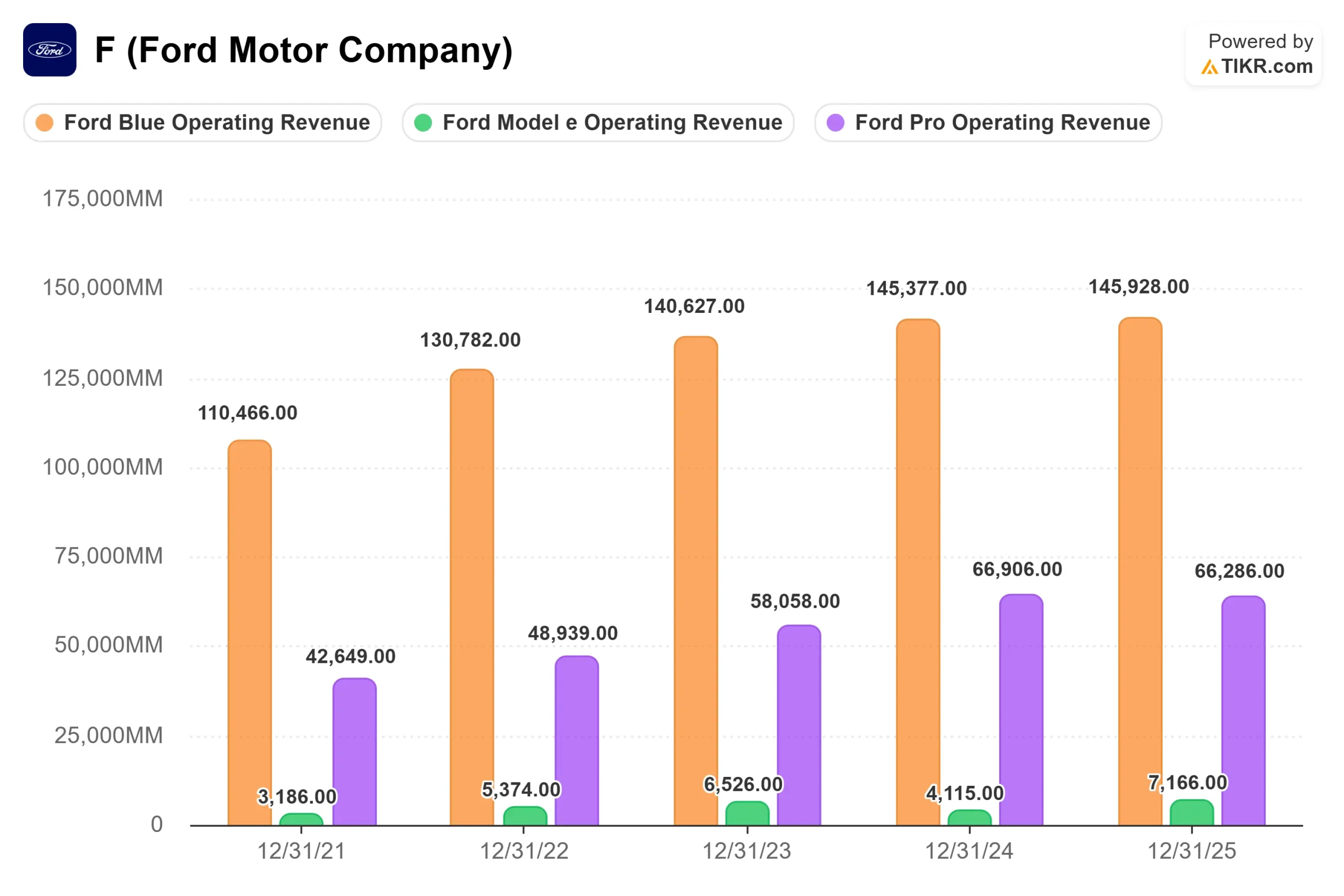

Second, Ford Pro. The commercial vehicle segment generated $6.8 billion in segment EBIT at a double-digit margin in 2025, separate from the company’s total adjusted EBIT figure. Farley described it plainly on the Q4 earnings call: “It’s a durable commercial business our competitors cannot match.” Ford Pro holds over 42% Class 1 through 7 U.S. market share. Paid software subscriptions grew 30% in 2025, and Ford Pro Intelligence subscriptions reached over 865,000 in Q1 2026 per the company’s April 2 sales report.

Third, the Novelis restart. COO Kumar Galhotra confirmed the hot mill is expected to restart between May and September 2026. When it does, House said the $1.5 to $2 billion in temporary aluminum costs are “not expected to be repeated in 2027.”

On peer multiples, Ford’s forward EV/EBITDA of 15.16x sits above GM at 7.40x, BMW at 8.04x, and Mercedes-Benz at 9.18x. That gap reflects Model e losses suppressing EBITDA without reducing enterprise value, not a premium valuation. On a forward P/E basis, Ford at 7.62x is more comparable to peers, though GM’s 5.83x reflects a more disciplined buyback record that the market continues to reward.

The risk is straightforward.

Ford Model e lost $4.8 billion in 2025. The 2026 guide calls for $4 to $4.5 billion in losses as Gen 1 restructuring savings are partially offset by Gen 2 investment ahead of the Universal EV Platform (UEV) launch in 2027.

Farley set the destination: “The goal is to set up the company over the next couple years to be that 8% margin company.” That target is set for 2029. Every dollar Ford Pro earns partially subsidizes the EV transition until then, and the April tariff shock added new uncertainty to every projection between now and that target.

See how Ford performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $11.60

- Target Price (Mid): $19.58

- Potential Total Return: +68.8%

- Annualized IRR (Mid): 8.90% / year

See analysts’ growth forecasts and price targets for Ford stock (It’s free!) >>>

The TIKR mid-case uses a 2.4% revenue CAGR through 2030. The two primary drivers are Ford Pro’s continued share gains in North American commercial markets and Ford Blue’s improving mix as low-margin nameplates are phased out in favor of trucks, off-road trims, and hybrids. Net income margin reaches 4.5% in the mid-case, up from 2.5% in 2025, as Model e losses narrow and the Novelis cost drag ends after 2026.

The high case to 12/31/30 implies a stock price of $28.21 at a 10.7% IRR, requiring 2.7% revenue growth and margins near 4.6%. That outcome depends on the UEV platform gaining traction after its 2027 launch and Ford Pro’s software mix reaching its 20% EBIT contribution target. On the downside, if the new tariffs meaningfully compress industry volumes, if Novelis costs persist, and if Model e losses widen, the stock has limited support above its 52-week low of $8.44.

Ford ended 2025 with close to $29 billion in cash and nearly $50 billion in liquidity. Farley noted that Ford produces more than five vehicles in America for every one it imports, a structural advantage versus European peers in the current tariff environment. That balance sheet and domestic production footprint are the two factors that make the mid-case recoverable even in a difficult 2026.

Conclusion: Watch adjusted EBIT at Q1 2026 earnings on April 28, 2026. Management guided for roughly flat sequential EBIT in Q1 relative to Q4’s approximately $1 billion. The print itself is not the story. What matters is whether Sherry House maintains the $8 to $10 billion full-year EBIT range given the April tariff announcement. A maintained range confirms the cost program is holding. A cut signals the recovery has been pushed out again.

Ford at $11.60 is a cash-generating business paying a 5.2% dividend while absorbing an EV transition with a defined endpoint. The TIKR mid-case implies 68.8% total return to 12/31/30 at an 8.90% annualized IRR. How much of that the tariff environment allows to materialize is the only question that matters at Q1 earnings.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Ford?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ford, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ford alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!