Key Takeaways:

- The Rate Inflection: After years of headwinds, new customer rates have turned positive, accelerating to over 3% growth year-over-year (net of discounts) in Q3.

- External Growth Machine: Management is capitalizing on market dislocation, executing a $244 million acquisition of 24 properties across Utah, Arizona, and Nevada.

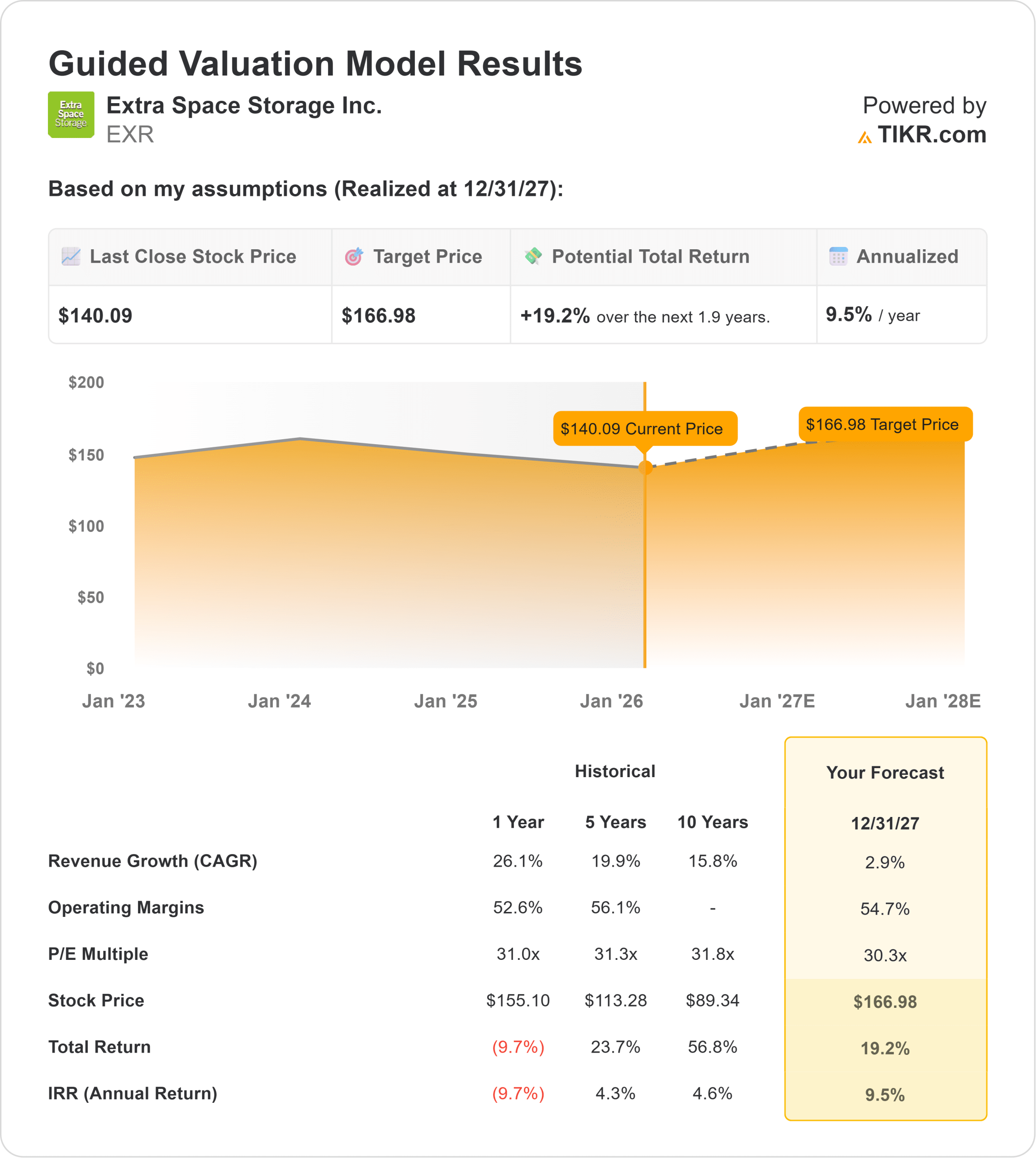

- Price Projection: The valuation model points to a target of $167 by 2027, suggesting moderate upside from today’s price.

- Solid Returns: With an implied 9.5% annualized return, the model signals a “Hold,” indicating the stock is priced for steady compounding rather than explosive growth.

Extra Space Storage (EXR) is the largest self-storage operator in the U.S., and it is finally seeing the light at the end of the tunnel.

CEO Joe Margolis highlighted a critical turning point in the latest quarter: new customer rates have increased positively for the first time in three years.

This pricing power is supported by a rock-solid operational platform.

Same-store occupancy remains high at 93.7%, and the company’s third-party management platform added another 95 stores, bringing the total managed portfolio to over 1,800 locations.

Financially, the company is a fortress.

LTM Revenue stands at $3.42 billion with impressive Operating Margins of 44.8%.

However, with the stock trading at $140, the valuation is not exactly a bargain. Is this the right entry point, or should investors wait for a better pitch?

What the Model Says for EXR Stock

This analysis evaluates EXR’s potential through 2027, balancing the improving rate environment against the current valuation premium.

The model signals a “Hold.”

Using a forecast of 2.9% Revenue Growth (CAGR) and 54.7% Operating Margins, the model points to a target price of $167 by December 2027.

This implies a 9.5% annualized return from today’s levels.

The model suggests that Extra Space is “fairly valued.” It offers high-single-digit returns driven by stability and dividends, but the current price leaves little room for multiple expansion.

Wall Street is slightly more cautious.

The average “Street Target” is $150.95, which implies only 7% upside and is lower than our model’s projection.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for EXR stock:

1. Revenue Growth: 2.9%

The growth engine is restarting.

Management noted that street rates improved sequentially every month since May, driven by their proprietary pricing systems and marketing investments.

While same-store revenue was flat in the short term due to discounting, the long-term trend is pointing up.

The model forecasts a steady 2.9% CAGR, reflecting the company’s ability to drive rents higher as housing turnover stabilizes.

2. Operating Margins: 54.7%

Scale drives superior profitability.

The model assumes Operating Margins will maintain a robust 54.7% through 2027.

This high margin profile is defended by the company’s “Bridge Loan Program,” which generates high-yield interest income ($123 million in originations this quarter) and feeds the acquisition pipeline.

3. Exit P/E Multiple: 30.3x

REITs typically trade on FFO multiples, but the TIKR model uses a P/E proxy for this projection.

The model assumes an exit multiple of 30.3x.

This is a premium multiple, reflecting Extra Space’s status as a “best-in-class” operator with significant scale advantages over smaller peers.

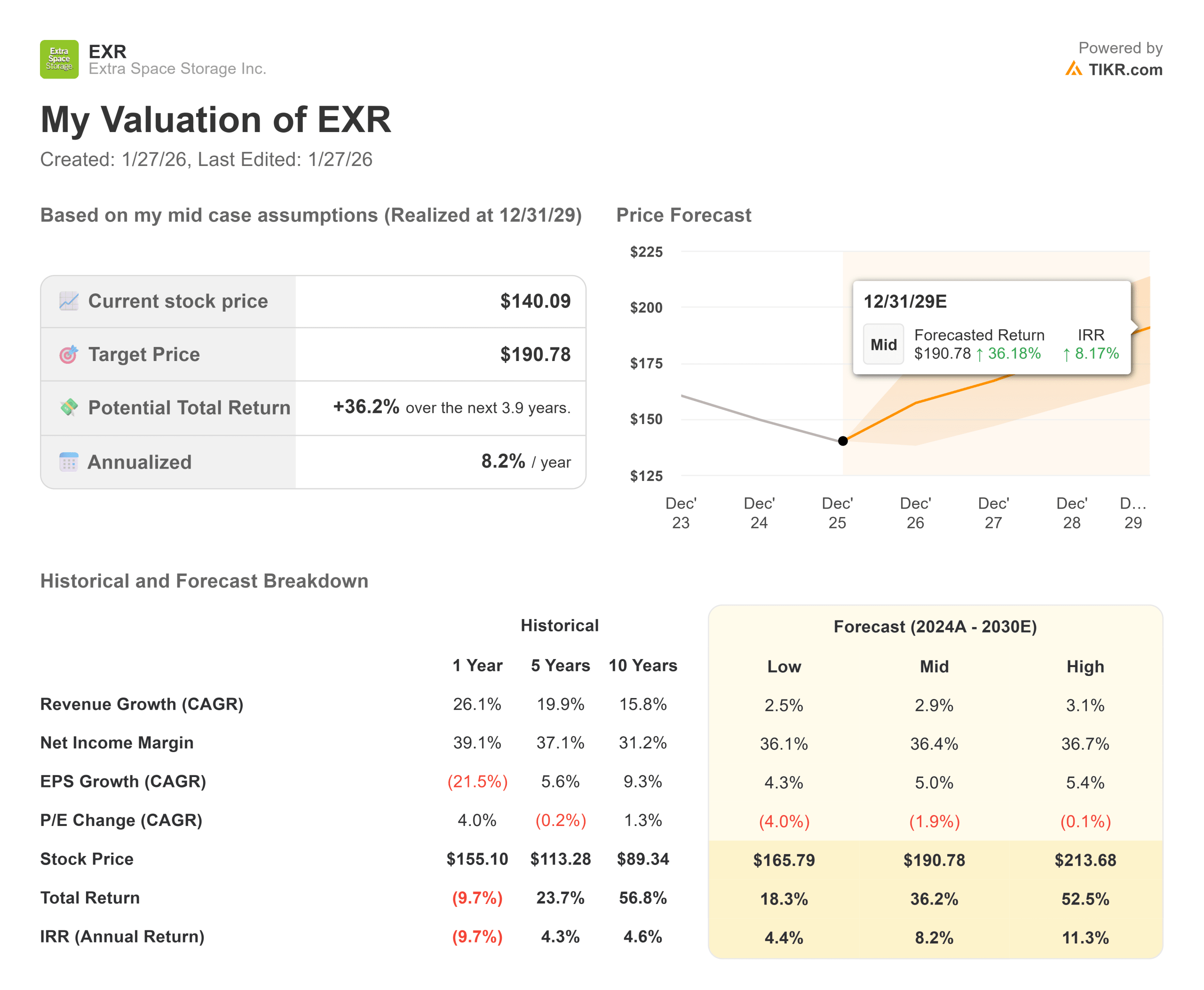

What Happens If Things Go Better or Worse?

Looking at the longer-term scenarios (through 2029), the risk/reward profile remains balanced (these are estimates, not guaranteed returns):

- Low Case: If rate growth stalls, the model projects a return of just 4.4% per year, underperforming the broader market.

- Mid Case: With steady execution, the Advanced Model points to an 8.2% annual return through 2029.

- High Case: If the housing market rebounds sharply, driving higher move-in volumes, the stock could deliver an 11.3% annual return, pushing the IRR into double-digit territory.

See what analysts forecast for the next 5 years for EXR stock (Free with TIKR) >>>

How Much Upside Does EXR Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!